What Is a Conventional Loan?

What You Should Know

- Conventional loans have stricter requirements compared to government-backed loans, and can require a higher credit score and lower debt-to-income ratio

- A conventional loan would be a better choice than government-backed loans if you have a large down payment and a high credit score

- While conventional loans can have low interest rates, making a down payment of less than 20% will require private mortgage insurance premiums to be paid

- You can get a conventional loan from any private lender, such as a bank or credit union

What Is a Conventional Home Loan?

A conventional loan, also known as a conventional mortgage, is a type of home loan that isn't backed or insured by a government agency. Instead, conventional loans are offered by the private sector, which can include banks and credit unions. Conventional loans might also have private mortgage insurance (PMI) rather than being insured by the federal government. There are seven main types of conventional loans.

Conventional loans are the standard, regular mortgage loans that you might be thinking of when you picture what a typical mortgage loan would be. Namely, you will need a good credit score, a stable employment history, an income that allows you to have an acceptable debt-to-income ratio, and a sizable down payment in order to qualify for a conventional loan. If you do not have a good credit history, then there are other ways to finance a house with bad credit.

Conventional mortgage loans don't have special features that unconventional mortgages might have, such as no down payment requirement or no mortgage insurance premiums, and they also don't generally offer reduced credit score requirements or higher tolerance for existing debt. Many conventional loans are considered qualified because they follow a qualified mortgage rule.

Conventional loans are the most common type of home loan offered by lenders. If you have a strong financial profile, you will have plenty of mortgage lenders to choose from. However, conventional loans are generally harder to be approved for. This page will take a look at conventional loan requirements, the difference between conventional loans and other types of mortgage loans, and current conventional loan rates today.

Conventional Loan Rates

Today's Best Mortgage Rates

See the latest Mortgage Rates at the Casaplorer® Mortgage Rates Page

Types of Conventional Loans

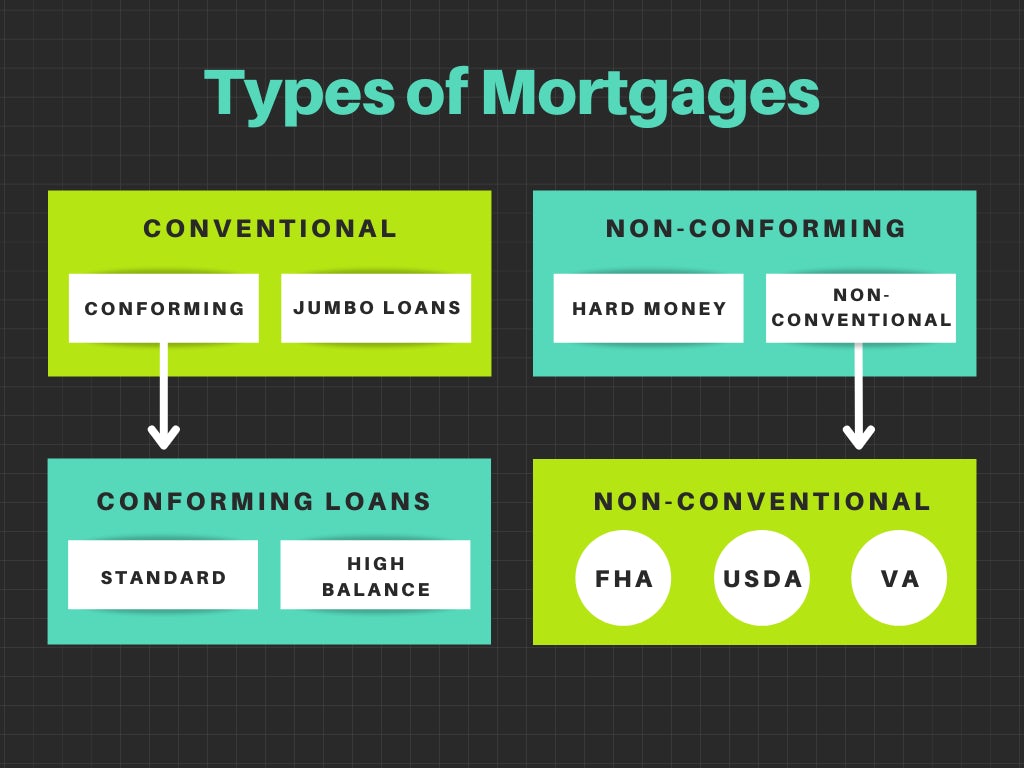

There are two main types of conventional loans: conforming conventional loans and non-conforming conventional loans. Conforming conventional loans tend to be backed by a quasi-government agency while non-conforming loans are not backed. This means that non-conforming loans tend to be perceived riskier by lenders. Regardless of what type of loan you get, you are still responsible to make mortgage payments. If a borrower misses a certain number of payments on their mortgage, the property may move into the pre-foreclosure stage where a borrower may be forced to sell the property.

Conforming Loans

What does it mean when a loan is conforming? It simply means that the loan conforms to the loan limits set out by the Federal Housing Finance Agency (FHFA) and that also conforms to Fannie Mae and Freddie Mac lending guidelines. By conforming to these limits and guidelines, mortgage lenders will be able to sell the loans that they have originated off to investors. Fannie Mae and Freddie Mac purchase home loans from lenders that meet their specific requirements and repackage them into investment products that are sold in the financial markets. Since they will only provide guarantees to mortgages that meet their size and quality requirements, that is why lenders offer good mortgage rates to conventional loans that conform to these requirements.

The major requirement that all conforming loans must meet is the loan limit requirement. The loan must be within the conforming loan limits set by the Federal Housing Finance Agency (FHFA). Loan limits are based on the county that you are located in, such that certain counties have different limits based on the cost of the homes in the area.

Conforming Loan Limits for 2023

The 2023 conforming loan limit for most counties is $726,200.

Higher-cost counties will have a higher conforming loan limit, up to a maximum of $1,089,300 for 2023.

For example, New York, San Francisco, and Los Angeles counties all have a conforming loan limit of $1,089,300 for 2023. This is an increase from the highi-cost loan limit of $970,800 in 2022.

This means that the conventional loan limit will increase by $79,000 for the base loan limit and increase by $118,500 for the high-cost loan limit for 2023.

2023 Conforming Loan Limits for Multi-Unit Properties

| Property Type | Baseline Limit (Low-Cost Counties) | Maximum Limit (High-Cost Counties) |

|---|---|---|

| 1-Unit | $726,200 | $1,089,300 |

| 2-Unit | $929,850 | $1,394,775 |

| 3-Unit | $1,123,900 | $1,685,850 |

| 4-Unit | $1,396,800 | $2,095,200 |

Super Conforming Loans

Super conforming loans, which are also known as high-balance loans and conforming jumbos, are mortgages in high-cost counties that are above the base conforming loan limit, but are permissible due to a higher conforming loan limit. For example, the 2023 conforming loan limit for Los Angeles County is $1,089,300. A mortgage loan of $1,000,000 would be above the FHFA’s 2023 conforming loan limit of $726,200, but since it is below the specific county loan limit, this mortgage loan would still be conforming. Instead of being called a conforming loan, these types of loans are called super conforming loans.

Using Piggyback Loans to Get Around the Conforming Limit

Did you know that you can use a piggyback loan to get around the conforming limit? Piggyback loans, also known as 80-10-10 loans, allows you to take out two separate loans at once to purchase a home. The second “piggyback” loan reduces the size of your main loan. This means that you can reduce your main loan size so that it is under the conforming loan limit. This lets you benefit from lower conforming loan rates without needing to come up with a large down payment. This is an important loan type that homebuyers should be aware of. Some home buyers find expensive ways to raise their money for the down payment simply because they are not aware of the options. For example, some home buyers make a 401(k) withdrawal to purchase a home before looking at all available options, which leads to large fees that a borrower has to pay.

For example, let’s say that you want to purchase a $1.3 million home in Los Angeles. The conforming loan limit in Los Angeles for 2023 is $1,089,300, which means that you will need to make a down payment of about 20% to bring the loan under this limit. That works out to be around $218,000. With a piggyback loan, you can take out a loan to cover 10%, or $109,000, which can then be used towards your down payment. You’ll now only need to come up with another $109,000 down payment for your conforming loan.

Piggyback loans can also come in different proportions, such as 60-20-20. This allows you to benefit from having at least part of your home loan as a conforming loan with lower rates, while only a small portion of your home loan will consist of a jumbo loan. For example, let’s say that you’re looking to purchase a 2-unit home for $2 million, and the conforming loan limit in your medium-cost county is $1 million. Can you still get a conforming loan for this property, even if the price is $1 million over the conforming loan limit?

With a piggyback loan, you can use a 50-30-20 proportion. This means that 50% will be financed with a conforming loan of $1 million. 30% will be financed with a piggyback loan of $600,000. The remaining 20% is the down payment of $400,000. With this method, you will be able to still benefit from having a conforming loan, rather than having to pay possibly higher rates with a $1.6 million jumbo loan. However, piggyback loans require borrowers to have a good credit score to qualify.

Types of Non-Conforming Loans

- Conventional Loans (Non-Conforming)

- Jumbo Loans

- Non-Conventional Loans (Non-Conforming)

- FHA Loans

- USDA Loans

- VA Loans

- Hard Money Loans

- Interest-Only Mortgage Loans

- Seller Carry Back Mortgage Loans

- Physician Mortgage Loans

Non-Conforming Loans

Non-conforming conventional loans are mortgages that do not meet the requirements set out by Fannie Mae and Freddie Mac. These loans are usually above the conventional loan limit of the county and are known as jumbo loans. For example, if you are buying a $1.3 million home with a $300,000 down payment in New York City where the loan limit is $970,800, you would have to get a jumbo mortgage. That’s because your mortgage loan of $1,000,000 is above the $970,800 loan limit for New York City. Jumbo loans have stricter eligibility requirements due to the higher risk to the lender. Typically, you will need to have a credit score greater than 700, a minimum down payment of at least 20%, and a debt-to-income (DTI) ratio no greater than 43% in order to qualify for a jumbo loan.

Besides jumbo loans, other types of non-conforming loans include non-conventional loans, such as FHA loans, USDA loans, and VA loans, along with hard money loans, interest-only mortgage loans, and seller carry back mortgages.

Conventional Loan Requirements

Eligibility requirements can vary from lender to lender, however, there are some basic requirements that most lenders look for. Some lenders may set stricter requirements, so the best way to see what you can qualify for is to request a mortgage pre-approval from your lenders to see how much they are willing to approve you for. It is still important to remember the basic requirements, so the basic requirements for a conventional loan are:

Conventional Loan Requirements 2023

| Minimum Down Payment | At least 3% |

| Minimum Credit Score | 620 or higher |

| Maximum Debt-to-Income Ratio | Less than 50% |

Minimum Down Payment

The conventional loan down payment requirement is 3% or an LTV ratio less than 97%. However, you must be a first-time home buyer and be purchasing a single-unit family home in order to be able to make a down payment of as low as 3%. If you are not a first-time homebuyer or are getting an adjustable-rate mortgage, you must put at least 5% down. An adjustable-rate mortgage uses a variable mortgage rate which changes with a benchmark index like the prime rate along with an additional credit spread.

For example, you can purchase a $300,000 home with a down payment of as little as $9,000 using a conventional loan with some lenders. Whether you are a first-time homebuyer or not, private mortgage insurance (PMI) will be required if the down payment is less than 20%. Making a down payment of less than 20% will require you to make PMI premium payments, which increases the cost of your conventional mortgage loan.

Minimum Credit Score

Conventional loans typically require your credit score your credit score to be greater than 620. The higher the credit score, the lower your conventional mortgage loan rate.

Maximum Debt-to-Income (DTI) Ratio

Your DTI ratio must be less than 50%, which means less than 50% of your monthly income should be going towards monthly debt and interest repayments. For example, if your monthly income is $5,000, less than $2,500 ($5,000 x 50%) should be spent on debt repayments per month. However, not all lenders allow a maximum DTI ratio as high as 50%.

Some might have a maximum DTI limit of 43% or 36%. The Qualified Mortgage (QM) rule, from the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd-Frank Act), requires residential mortgages to have a DTI ratio of 43% or less in order to be considered a Qualified Mortgage, alongside other criteria. Non-QM mortgages can avoid these rules.

Conventional Loans vs Government-Insured Loans

Conventional Loan vs FHA

Federal Housing Administration (FHA) loans are insured by the FHA, while conventional loans are not. This allows FHA-approved lenders to offer FHA loans with lower down payment requirements and lower credit score minimums. However, all FHA loans require the payment of FHA mortgage insurance premiums (MIP). MIP is paid both upfront and annually, and it cannot be canceled. On the other hand, the main difference between FHA and conventional loans is that conventional loans do not require mortgage insurance if the borrower makes a down payment of 20% or more. For conventional loans that require mortgage insurance , where a down payment of less than 20% was made, the loan’s mortgage insurance can still be canceled once the loan’s LTV is less than 20%. That’s not possible with an FHA loan.

What this means is that FHA loans allow borrowers to make low down payments at the expense of mortgage insurance premiums. Their looser requirements also make it easier for borrowers to qualify for a mortgage loan. Borrowers that can afford to make a 20% or larger down payment can benefit by getting a conventional loan without having to pay extra for mortgage insurance, as long as they meet the stricter lending requirements of conventional loans.

What Are FHA and Conventional Loan Limits?

FHA loan limits are different from conventional loan limits. FHA loan limits are set by the U.S. Department of Housing and Urban Development while conventional loans have conforming loan limits set by the Federal Housing Finance Agency (FHFA).

For 2023, the FHA loan limit “floor” is $472,030, while the FHA loan limit “ceiling” is $1,089,300. The FHA loan limits vary by county.

For 2023, the conventional loan limit “floor” for conforming loans is $726,200, while the conventional loan limit “ceiling” for conforming loans is $1,089,300. There is no conventional loan limit for non-conforming loans.

FHA vs. Conventional Loan Limits 2023

| Loan Limit “Floor” | Loan Limit “Ceiling” | |

|---|---|---|

| FHA Loans | $472,030 | $1,089,300 |

| Conforming Conventional Loans | $726,200 | $1,089,300 |

Is a conventional loan better than an FHA loan?

Whether a conventional loan is better than an FHA loan depends on your financial situation. For example, FHA loans are a better option, or sometimes the only option, for borrowers with a credit score of less than 620. Conventional loans require a credit score of at least 620, which means that having a credit score of 600 would mean that you would not be able to get a conventional loan. Generally, FHA loans are better for borrowers with a lower credit score, lower down payment, and a higher DTI ratio. The opposite is true for conventional loans. Borrowers with a higher credit score, high down payment, and low DTI ratio would be better off with a conventional loan.

FHA vs. Conventional Loan: Which One Is Better For Me?

| FHA Loan | Conventional Loan |

|---|---|

| Credit Score Below 620 | Credit Score Above 620 |

| High Levels of Debt (DTI up to 50%) | Lower Levels of Debt (36% DTI or Less) |

| Low Down Payment of as Little as 3.5% | Down Payment of 20% or More |

If you already have an FHA loan, you can switch your FHA loan to a conventional loan through a mortgage refinance. This might make sense if you’re able to get a lower conventional loan rate compared to your current FHA loan rate, which might happen if your credit score has improved and your loan’s LTV has decreased. FHA loans make it easier for borrowers to get a mortgage. Once your financial situation allows it, refinancing to a conventional home loan may result in a lower interest rate. You'll also be able to get rid of FHA mortgage insurance premiums as well. Before choosing to refinance to a conventional loan, you should compare the terms of your new loan to the terms of the current loan as well as understand the differences between PMI and MIP.

Do FHA loans have lower interest rates than conventional loans?

FHA loans have a lower interest rate compared to conventional loans for mortgages with a smaller down payment. For mortgages with a large down payment, conventional loans will generally have a lower mortgage rate.

| Small Down Payment | Large Down Payment | |

|---|---|---|

| FHA Loans | ☑ Lower Rate | Higher Rate |

| Conforming Conventional Loans | Higher Rate | ☑ Lower Rate |

Differences between FHA loans vs. conventional loans also apply to credit score requirements, down payment amounts, down payment sources, DTI, and property standards. For a full list and explanation of differences, visit our conventional loan vs FHA loan page.

VA Loan vs. Conventional Loan

VA loans are backed by the Department of Veterans Affairs and are available to eligible veterans and their spouses. VA loans do not have a minimum down payment or credit score requirement, however, all VA loans have an upfront VA funding fee. VA loans are almost always the better option than conventional loans if you are eligible.

Compared to conventional loans, VA mortgage loans have no minimum down payment requirement, no private mortgage insurance cost, and no maximum mortgage loan amount. While the Department of Veterans Affairs doesn’t set a minimum credit score requirement themselves, individual VA loan lenders will have their own credit score requirements. This minimum is usually 620 for a VA loan, however, some lenders can be more flexible and allow lower credit scores of around 580. The drawbacks of VA loans is that you are limited to purchasing primary residences, rather than second homes or investment properties. Instead of paying for conventional loan PMI, you will also need to pay a VA loan funding fee instead.

| VA Loan | Conventional Loan | |

|---|---|---|

| Differences | 0% down payment allowed | Minimum down payment of at least 3% |

| Can only be used for owner-occupied primary residences | Can be used for primary residences, as well as second homes and investment properties | |

| VA Loan Funding Fee | PMI Premiums | |

| Similarities | Minimum credit score of 620 | |

| DTI of 50% or less | ||

| Similar term length and mortgage rate options | ||

How does a VA loan compare to Conventional Loans?

In most cases, a VA loan is better than conventional loans. VA loan rates are generally lower than conventional loan rates, plus you will only need to pay a one-time VA loan funding fee rather than a monthly PMI premium. Being able to purchase a home with zero down payment can also be enticing and can make it easier for borrowers to purchase a home.

The main drawbacks with VA loans are the restrictions that come with it. You will need to be eligible for VA loans in the first place, which requires you to be a veteran, an active service member, or a spouse of a veteran or service member. You'll also need to have a Certificate of Eligibility (COE) entitlement that allows you to purchase a home with a VA loan. This typically means that you won't be able to have two VA loans at once if you have no remaining COE entitlement available. VA loans can also only be used to purchase primary residences, and the borrower must occupy the home within 60 days of the VA loan closing. This means that you can’t purchase a second home and investment property, and you also would need to be able to move in fairly quickly. Conventional loans don’t have this requirement, making them much more flexible for borrowers looking to finance a home purchase.

The benefit of being able to make no down payment can also be risky if you’re not planning on staying in the home for a longer period of time. Having little to no home equity can be a problem if your home’s value decreases and you need to move and sell your home. You could owe more than your home is worth, meaning that you’ll need to come up with cash to make up for the difference if you sell your home for less than your VA loan balance.

Just like how conventional loans can beat out FHA loans for down payments of 20% or more, conventional loans can also be a better option compared to VA loans if you are able to make a down payment of 20% or more. The ability to pay no mortgage insurance or funding fees can work out to save you a lot of money. The upfront VA loan funding fee means that if you plan on paying off your VA loans early, such as if you were to sell your home, then the funding fee over a short period of time will result in a higher mortgage APR, even if VA loans have lower interest rates. And as usual, a higher down payment generally results in a lower interest rate. If you have enough cash to make a 20% or larger down payment, you may find more favorable conventional loan rates compared to VA loan rates.

USDA vs. Conventional Loans

USDA loans are insured by the Department of Agriculture and are aimed at individuals buying a home in a rural area. USDA loans do not have minimum down payment requirements or credit score requirements, however, your income must be less than 115% of the median county income in the county that you are looking to purchase a home in. You can’t use an USDA loan to purchase a home anywhere in the country either. USDA loans are only available for rural areas, which can be found by using an USDA loan eligibility map.

USDA loan rates can be lower than conventional loan rates, however, USDA loans come with restrictions. These include:

- Can only be used to purchase homes in rural areas, as defined by the USDA

- Can only be used to purchase primary residences

- There’s a limit on the borrower’s household income when it comes to USDA loan eligibility

- USDA loan approvals can take longer than conventional loan approvals

However, USDA loans are also more flexible than conventional loans in other areas. For example, USDA loans have no prepayment penalties for early mortgage payoffs, while some conventional loan lenders may charge a prepayment penalty. USDA loans can also be used to build a home too, rather than requiring a separate construction loan to finance construction. With an USDA loan, you can also finance the closing costs and USDA guarantee fee by rolling it into your loan. This means that USDA loans are a way for borrowers to build or buy a home with no upfront cost.

Advantages & Disadvantages of Conventional Loans

Advantages of Conventional Loans

- All Types of Property - Conventional loans can be used for a variety of mortgages from standard conforming loans to jumbo non-conforming loans. Mortgages for second homes, investment properties, farm-use, or multiple unit homes can be purchased using a conventional loan. Government mortgages are mostly for first-time home buyers, low-to-moderate income households, and for single-unit homes that will be the primary residence.

- Numerous Loan Structures - Conventional loans are flexible in terms of their length and rate options. You can get a conventional mortgage for 10, 15, 20, 25 or 30 years and you can choose between fixed and adjustable-rate mortgages. In comparison, government-backed mortgages mostly offer 30-year fixed loans only.

- Removal of Mortgage Insurance - Private mortgage insurance (PMI) can be removed once you attain an LTV ratio of 78%, or when you refinance your mortgage once you have at least 20% equity in the home. On the other hand, mortgage insurance cannot be removed and is required to be paid for the full life of an FHA loan. VA loans have an upfront fee that cannot be refunded unless you meet specific VA funding fee exemptions.

- Down Payment Options -You can choose to benefit from a 3% down payment with PMI or choose to pay at least 20% down to avoid PMI. There is flexibility in deciding based on how much house you can afford. It is also important to note that there are different types of PMI, which may provide borrowers with different financial opportunities.

- No Program Specific Fee - Lender fees are still there, however, there are no upfront program fees. Most government-insured programs have some upfront fee, for example, VA loans have an upfront VA funding fee.

Disadvantages of Conventional Loans

- Minimum Credit Score of 620 - Conventional loans are great if you have a credit score greater than 620 because most lenders will require at least 620 to accept your application. However, meeting the bare minimum requirement and having a credit score of 620 will cause you to get a very high mortgage rate as lenders will not see you as creditworthy. On the other hand, government-insured loans have much lower credit score requirements, with FHA at 500 and VA and USDA not having a minimum credit score requirement.

- Higher rates with Lower Down Payment - Although you can get a mortgage with a down payment as low as 3%, the mortgage rate and PMI on the loan will be very large. Therefore, if you do not have savings for a larger down payment and can qualify for an FHA loan, a non-conventional government-backed mortgage might be a more suitable option.

- Stricter Qualifications - As conventional loans are not insured by the government, lenders have to be careful who they give a mortgage to. This makes the qualification process for a conventional loan to be harder than government-insured programs that focus on increasing homeownership.

Comparing Conventional Loans

Conventional Loan Down Payment Options

Some lenders offer Conventional 97 loans, which are 3% down conventional loans. Is a conventional 97 loan with a 3% down payment better than making a 5%, 10%, or 20% down payment? Out of these options, a conventional 97 loan will have the highest mortgage rate. However, you’ll have a lower upfront cost.

Let’s take a look at a $500,000 home. How much down payment would a conventional loan require?

Down Payment

- Conventional 97: $15,000

- Conventional 95: $25,000

- Conventional 90: $50,000

- Conventional 80: $100,000

With a conventional 97 loan, you’ll only need a down payment of $15,000 to purchase a $500,00 home. In comparison, making a down payment of 20% to avoid PMI will require you to have $100,000 saved up. Due to loan-level pricing adjustments (LLPA), conventional loans with a higher LTV will have a higher mortgage rate. While conventional loans with a low down payment will require a smaller upfront cost, a low down payment conventional loan will require higher monthly payments.

Let’s take a look at a $500,000 home that you want to finance for a 30-year term.

Monthly Mortgage Payments

- Conventional 97: $2,097 (at 3.2%)

- Conventional 95: $2,028 (at 3.1%)

- Conventional 90: $1,922 (at 3.1%)

- Conventional 80: $1,686 (at 3%)

When comparing Conventional 97 with Conventional 95, your monthly mortgage payments excluding PMI would be $69 higher every month at these example mortgage rates. The difference in down payment was only $10,000, but it will cause you to pay $69 more every month for 30 years. Spread out over 30 years, this means that you will be paying $24,840 more in the future just to save $10,000 today. If you’re able to afford it, making a larger down payment on a conventional loan can save you money in the long run.

Conventional Loan Structure Options

There are three types of interest rate options for conventional loans: fixed rate, adjustable rate (ARMs), and hybrid adjustable rate (Hybrid ARMs). Fixed rate mortgages are the most common type of conventional loan.

- Fixed Rate

With a fixed-rate conventional loan, your monthly principal and interest payments stay the same for the entire term length. This means that your mortgage payments will not change, allowing for stability and certainty. Fixed-rate conventional loans generally have a mortgage term of either 15 years or 30 years.

- Adjustable Rate (ARMs)

Adjustable rate mortgages have an interest rate that can increase, decrease, or stay the same, based on a certain index that will determine your ARM interest rate. A margin will be added to determine your ARM rate. ARMs will usually have a mortgage term of 30 years.

- Hybrid Adjustable Rate (Hybrid ARMs)

Hybrid ARMs have an interest rate that starts off as a fixed-rate for a certain number of years before becoming an adjustable rate for the remainder of the mortgage term. For example, a hybrid ARM might have a fixed-rate for 5 years before turning into an adjustable rate.

Comparing Conventional Loan vs Government Mortgage Options

What’s better: a conventional loan, FHA loan, USDA loan, or VA loan? Assuming that you are eligible and can qualify for all of these options, you might decide to base your decision based on the monthly mortgage cost. Some borrowers with limited funds might base their decision on the amount of down payment required. Others may choose based on the flexibility that the loan option provides, such as financing for certain property types or loan amounts. There’s no single answer to this question since each borrower is unique and their needs and goals will vary. Still, we can take a look at an example scenario to see which option comes out ahead in various situations.

Let’s take a look at a $500,000 home that is eligible for all of these loan options. If you had to choose, which one of the following do you prioritize: a low down payment, a low monthly mortgage amount, or flexibility?

Down Payment

- Conventional 97: $15,000 at 3%

- Conventional 80: $100,000 at 20%

- FHA: $17,500 at 3.5%

- USDA: $0 at 0%

- VA: $0 at 0%

If having a low down payment is most important to you, then USDA loans and VA loans offer a zero down payment option. Conventional loans can have a down payment as low as 3%, while FHA’s minimum down payment is 3.5%. This makes the difference between a conventional 97 loan and an FHA loan to be just a $2,500 difference in down payment amount.

Monthly Mortgage Payments

To compare mortgage payments, let’s assume that these loan options all have the same fixed mortgage rate of 3% for a 30-year term.

- Conventional 97: $2,045 + $404 PMI at 1%

- Conventional 80: $1,686

- FHA: $2,034 + $342 MIP at 0.85%

- USDA: $2,129

- VA: $2,108 + $48 VA Fee

When combining monthly insurance and funding fees:

- Conventional 80: $1,686

- USDA: $2,129

- VA: $2,156

- FHA: $2,376

- Conventional 97: $2,449

Making a down payment of 20% will reduce your mortgage payments significantly. Among the low down payment options, USDA loans and VA loans have a lower mortgage payment amount even though they had zero down payments. That’s because the USDA guarantee fee and VA funding fee is less expensive compared to the hundreds of dollars a month that FHA MIP and conventional PMI premiums can cost.

Conventional Loans and Mortgage-Backed Securities (MBS)

How do conventional loans work? Lenders commonly sell conventional loans to Fannie Mae and Freddie Mac. Mortgage lenders, such as banks and credit unions, sell mortgages to Fannie Mae and Freddie Mac since they operate primarily as mortgage originators. Banks and credit unions lend you money for your mortgage loan, but they might not necessarily be the one that services your loan or even owns your mortgage.

When mortgage lenders sell your loan to Fannie Mae and Freddie Mac, they’ll be able to get back their money that they lent to you, allowing them to lend to other borrowers. They make money by originating loans. The role that Fannie Mae and Freddie Mac plays is that they purchase loans from lenders, bundle them up into packages, and then sell them to investors as a mortgage-backed security (MBS). This is known as “securitization”. Lenders may also sell their mortgages on the secondary mortgage market.

According to the Federal Housing Finance Agency, most U.S. residential mortgages are securitized. In 2020, Fannie Mae and Freddie Mac purchased a combined $2.5 trillion of single-family mortgages. Most mortgages that Fannie Mae and Freddie Mac purchase are fixed-rate mortgages. In fact, 99.64% of mortgages that they acquired in 2020 were fixed-rate mortgages.

Fannie Mae and Freddie Mac Mortgages by Type

| Type | % of Mortgages Acquired in 2020 |

|---|---|

| Fixed-Rate | 99.64% |

| Hybrid Adjustable Rate (Hybrid ARMs) | 0.33% |

| Other Mortgages | 0.03% |

| Adjustable Rate (ARMs) | 0% |

Fannie Mae and Freddie Mac have guidelines on which mortgages they will buy. Mortgages that meet these guidelines are called “conforming loans”. The term “conventional loan” and “conforming loan” are often used interchangeably, but they are not always the same. Government-backed loans can still be conforming loans, but Fannie Mae and Freddie Mac do not create MBS pools from government loans. Instead, FHA loans, VA loans, and USDA loans are pooled into Ginnie Mae MBS pools.

Ginnie Mae, which stands for the Government National Mortgage Association, is part of the federal government. On the other hand, Fannie Mae (Federal National Mortgage Association) and Freddie Mac (Federal Home Loan Mortgage Corporation) are government-sponsored enterprises (GSE) that are publicly traded companies.

Fannie Mae and Freddie Mac MBS vs. Ginnie Mae MBS

| Fannie Mae and Freddie Mac | Conventional Loans |

| Ginnie Mae | FHA Loans, VA Loans, and USDA Loans |

Loan–Level Pricing Adjustments (LLPA)

Conventional loans are subject to loan–level pricing adjustments (LLPA), which causes higher risk borrowers to pay a higher mortgage rate. That’s because Fannie Mae and Freddie Mac charge LLPA fees on mortgages with certain risk characteristics. While the lender will be the one directly paying for LLPAs when they deliver the mortgage to Fannie Mae and Freddie Mac, the lender will pass on these LLPA charges to the borrower in the form of a higher mortgage interest rate.

LLPAs can increase your conventional mortgage rate significantly. For example, a borrower with a credit score of 620 that borrows a conventional loan with a LTV of 97% will have a 3.50% LLPA. If the mortgage loan is for a principal of $100,000, then $3,500 will be deducted from the proceeds of the sale to Fannie Mae and Freddie Mac. Lenders will recoup the LLPA through higher mortgage rates.

The Loan-Level Price Adjustment (LLPA) Matrix lists the LLPAs that Fannie Mae assesses. The LLPA depends on your credit score, LTV, and mortgage or property type. LLPAs are cumulative, which means having more than one risk characteristic will result in more than one LLPA being charged.

Example of Loan-Level Price Adjustment (LLPA) Matrix

| Credit Score | Loan-to-Value (LTV) | ||||

|---|---|---|---|---|---|

| 60% or less | 80.01% - 85% | 85.01% - 90% | 90.01% - 95% | 95.01% - 97% | |

| 740 or more | 0% | 0.25% | 0.25% | 0.25% | 0.75% |

| 720 - 739 | 0% | 0.50% | 0.50% | 0.50% | 1.00% |

| 700 - 719 | 0% | 1.00% | 1.00% | 1.00% | 1.50% |

| 680 - 699 | 0% | 1.50% | 1.25% | 1.25% | 1.50% |

| 660 - 679 | 0% | 2.75% | 2.25% | 2.25% | 2.25% |

| 640 - 659 | 0.50% | 3.25% | 2.75% | 2.75% | 2.75% |

| 620 - 639 | 0.50% | 3.25% | 3.25% | 3.25% | 3.50% |

| Less than 620 | 0.50% | 3.25% | 3.25% | 3.25% | 3.75% |

Source: Fannie Mae

Example of Loan-Level Price Adjustment (LLPA) by Mortgage Type

| Mortgage Type | Loan-to-Value (LTV) | ||||

|---|---|---|---|---|---|

| 60% or less | 80.01% - 85% | 85.01% - 90% | 90.01% - 95% | 95.01% - 97% | |

| Adjustable Rate Mortgage | 0% | 0.25% | 0.25% | 0.25% | 0.75% |

| Manufactured Home | 0% | 0.50% | 0.50% | 0.50% | 1.00% |

| Second Home | 0% | 1.00% | 1.00% | 1.00% | 1.50% |

| Investment Property | 0% | 1.50% | 1.25% | 1.25% | 1.50% |

Source: Fannie Mae

Adverse Market Refinance Fee

The adverse market refinance fee was a fee charged to conventional refinances in the wake of the COVID-19 pandemic. 0.5% was charged for conventional loans that were backed by Fannie Mae and Freddie Mac that were refinanced, if the loan was for more than $125,000. The adverse market refinance fee didn't apply to FHA loans, VA loans, and USDA loans. The adverse market refinance fee was eliminated on August 1, 2021.

Super Conforming Loans and MBS

High-balance conventional mortgage loans will need to be specially identified when a lender delivers the mortgage to Fannie Mae or Freddie Mac. For example, Fannie Mae's special feature codes (SFC) require high-balance super conforming loans to be identified with code 808. When securitized and issued into mortgage-backed securities (MBS), super conforming mortgages can be packaged into Uniform Mortgage Backed Securities (UMBS) Pools and Supers Pools (Supers). Super conforming loans cannot make up more than 10% of the unpaid mortgage principal of a UMBS or Supers Pool. Seperate super conforming MBS Pools can be made up entirely of super conforming loans.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.