Current FHA Loan Rates

What You Should Know

FHA rates are determined based on the rates of securities composed of FHA mortgages. Supply and demand determine the rates of mortgage-backed securities in the free market. Because investors can choose to buy securities backed by any type of mortgage, different mortgage programs (e.g., conventional, FHA, VA) have similar rates.

Each lender decides what interest margin to add to the securities market rates. Also, each lender determines your default risk with its own proprietary formula; thus, not just you might get slightly different rates with each lender, but one lender might even qualify you while another had disqualified you.

FHA Insured Loans are part of a program by the Federal Housing Administration to facilitate homeownership for low-income and low-credit-score Americans. Applicants can either have a down payment as low as 3.5% and a credit score as low as 580 or a down payment as low as 10% and a credit score as low as 500. Both fixed-rate mortgages and adjustable-rate mortgages (ARM) are available under the FHA program.

Learn more about FHA loans and application requirementsCurrent FHA Loan Rates

As of August 8th, 2026

FHA Fixed Mortgage Rates

| TERM | RATE | APR | LENDER |

|---|---|---|---|

| 30-Year Fixed Rate | 7.125% | 8.055% | |

| 30-Year Fixed Rate | 6.250% | 7.141% | |

| 30-Year Fixed Rate | 6.000% | 6.896% | |

| 30-Year Fixed Rate | 7.250% | 8.173% | |

| 30-Year Fixed Rate | 7.124% | 8.087% | |

| 30-Year Fixed Rate | 5.990% | 6.938% | |

| 25-Year Fixed Rate | 7.250% | 8.277% | |

| 20-Year Fixed Rate | 7.250% | 8.431% | |

| 20-Year Fixed Rate | 7.124% | 8.206% | |

| 20-Year Fixed Rate | 5.990% | 7.065% | |

| 15-Year Fixed Rate | 6.750% | 7.859% |

Last updated August 08, 2026. Rates are for informational purposes only.

Current FHA Refinance Mortgage Rates

| TERM | RATE | APR | LENDER |

|---|---|---|---|

| 30-Year Fixed Rate (Refinance) | 6.250% | 7.155% | |

| 30-Year Fixed Rate (Refinance) | 7.625% | 8.540% | |

| 30-Year Fixed Rate (Refinance) | 6.999% | 7.648% | |

| 30-Year Fixed Rate (Refinance) | 5.750% | 6.384% |

Last updated August 08, 2026. Rates are for informational purposes only.

FHA Mortgage in the U.S.

| Prevalence of residential mortgage programs with a first lien on the property | ||||

|---|---|---|---|---|

| Loan program | Conventional mortgages (including conforming loans and jumbo loans) | FHA loans | VA loans | USDA loans |

| Portion of mortgages issued | 75% | 15% | 8% | 1.6% |

| Value of mortgages issued | 80% | 11% | 8% | 0.8% |

FHA loans are the second most common mortgage in the US. The federal government, through the Federal Housing Administration (FHA) which is a division of the Department of Housing and Urban Development (HUD), insures some mortgages and thus provides an alternative to conventional mortgages.

Source of Money

Most mortgages in the US are pooled together and sold by the loan originator (lender). The buyer might be a government agency (Ginnie Mae) or it might be a government-sponsored enterprise (GSE), like Fannie Mae and Freddie Mac, or it might even be a private entity. These buyers combine pools of mortgages and use them as collateral on bonds that they issue. In effect, they turn pools of mortgages into mortgage-backed securities (MBS). These MBSs are different from traditional bonds in that they pay interest and a portion of the principal at the end of each month, while traditional bonds like those issued by government or municipalities pay interest every six months and make a balloon payment for the principal and the last half-year of interest at the maturity of the bond. MBS payments are not fixed nor predictable. Through the MBS medium, your mortgage obligation and the lien on your house are traded regularly on the secondary market.

Yield

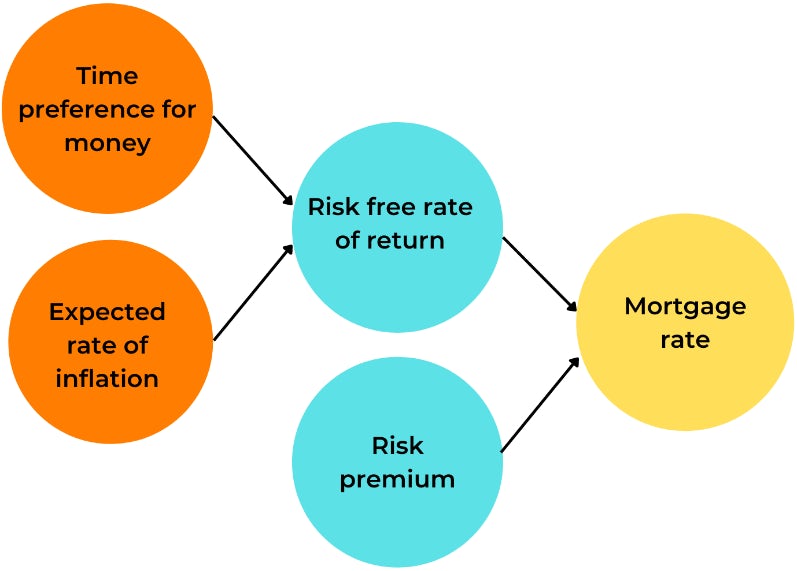

Thus the price you have to pay for your mortgage (your mortgage rate) is determined by MBS prices. Like any bond, MBS's price determines its interest rate. This interest rate is composed of two components. The first component is a risk-free rate of return and the second is the risk premium demanded by investors to hold mortgage obligations. It is generally assumed that federal government bonds are free from risk and thus their rate of interest is the risk-free rate of return. The risk-free rate is dependent on the maturity date of the bond. If you plot the rate of return vs. time left to maturity, the resulting graph is called the yield curve. The short end of the yield curve is generally controlled by the central bank through open market operations. While the yield, in general, is determined by supply and demand, that is theoretically the amount of savings in the economy vs. the amount of demand for borrowing capital. Practically it is determined by the extent of government deficit (bond issuance) vs demand for government bonds (mostly from the Federal Reserve, foreign governments and large institutional investors).

US Government Debt Yield Curve (2022/04/09)

Note that the longer one is expected to wait the less certain the future is. Thus generally the farther out you go on the yield curve the higher the rate of return. Thus a normal yield curve, sometimes referred to as a positive yield curve, occurs when long-term debt instruments yield larger returns compared with short-term debt instruments of the same quality. At times, longer-term instruments might exhibit a lower yield compared with shorter-term instruments. Such a situation is referred to as an inverted yield curve. Some consider an inverted yield curve as a predictor of recession. Generally, in earlier stages of economic development, the demand for capital is far greater than the supply of savings, thus larger yields; as an economy grows, savings accumulate and lower the yield.

Risk-free rate of return itself is composed of two components. The first is expected inflation and the second is time preference for money. An investor does not want to lose their savings to inflation and so they factor their inflation expectations into their expected rate of return. Also a saver needs to be rewarded for postponing consumption of the fruit of their labor. How much a saver is rewarded for postponing consumption depends on the savings relative to demand for capital. Over the last couple of decades another important factor has entered the market which is the central bank. Though central banks have been deciding for the short end of the curve through their policy overnight rate, over the last couple of decades they have been influencing various parts of the yield curve through quantitative easing (QE) and quantitative tightening (QT) programs.

Quantitative easing is when the central bank buys bonds in the open market. This is the modern equivalent of printing money and would lower interest rates. Interference by the Federal Reserve through lowering interest rates is referred to as loose monetary policy and supporters of such policy are referred to as doves. Quantitative tightening is when the Federal Reserve sells bonds on the open market. This is equivalent to annihilating money and increases interest rates. Interference by the Federal Reserve through increasing interest rates is referred to as tight monetary policy and supporters of such policy are referred to as hawks.

By this point we have seen that the most important component of your FHA mortgage rate is the risk-free rate of interest which is mostly determined by inflation expectations on the one hand and Federal Reserve policy on the other hand. Note that the link between mortgage rates and risk-free rate of return is provided by mortgage backed securities. The yield on mortgage backed securities include a risk premium which we should consider in order to understand mortgage yields.

The main source of risk for MBS is if one or more of the underlying mortgages do not perform, meaning that the borrower fails to make their payments. In such situations the servicer of the non-performing mortgage needs to foreclose on the mortgaged property. So one factor in determining MBS risk would be the likelihood of loss after a potential default. One factor contributing to potential loss would be the cost of foreclosure if default occurs. To judge the default risk factor the lender can use credit history (conveyed by your credit score) and employment history. The other risk factor would depend on how costly it is to foreclose in your locality. Thus the higher the default risk in your area and the more difficult it is to foreclose in your area, the higher the mortgage rate would be. Note that the procedure for foreclosure is generally set out in state law. Some states require judicial foreclosure. In these states, defaults are generally costlier for lenders. The location can also affect your mortgage rate in respect to the profit margin for loan initiators. The more lenders active in your area, the more competition among them. The more competition among lenders the lower their profit margin and thus your mortgage rate.

FHA specific considerations

What we have mentioned up to this point are about mortgages in the U.S. in general. Now let us consider FHA mortgages in particular. The Federal Housing Administration (FHA) was created by the National Housing Act of 1934. In 2021, the FHA insured 1.4 million new mortgages whose combined principal value was $343 billion. Any one who takes an FHA mortgage must pay mortgage insurance premium (MIP). MIP’s are contributions to the Mutual Mortgage Insurance Fund. If an FHA loan does not perform and the lender forecloses on the house, potential losses will be paid out of the Mutual Mortgage Insurance Fund.

One of the often overlooked advantages of FHA loans is related to situations where default has occurred or is very likely to occur soon. For such cases, FHA mandates the loan servicer to use a process called a waterfall. In the waterfall process, the loan servicer is required to consider a number of loss mitigation options in order and use the first one appropriate for the situation. These loss mitigation alternatives are:

- Forbearance

- Repayment plan

- Loan modification

- Partial claim

- Loan modification plus partial claim

- Pre-foreclosure sale (short sale)

- Deed in lieu of foreclosure

For conventional loans you can certainly ask for loss mitigation measures but your lender is not required to agree.

With an FHA loan your mortgage is insured, by paying mortgage insurance premium (MIP), for at least 11 years or for the life of the loan. In comparison for conventional loans, private mortgage insurance (PMI) can be ended when your equity reaches 20% by your proactive action, or it will end automatically when your equity in your home reaches 22%. Thus by carrying the insurance for longer, FHA loans are less risky compared with conventional loans. As a result, FHA loans tend to have a slightly lower rate. But except for very risky borrowers, the total cost of PMI is likely less than the total cost MIP. As a result, the average percentage rate (APR) which is the effective rate you are paying would most likely be higher with an FHA. In any case it would be a good practice to calculate your monthly payment using the FHA loan calculator and compare the result with what you get using a conventional loan calculator.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.

- The names and logos of third-party products and companies displayed on this website are the property of their respective owners and may also be trademarks.