Private Mortgage Insurance (PMI) Calculator

Property Information

Mortgage Information

Total Cost Breakdown

What You Should Know

- Private mortgage insurance (PMI) is required when a borrower contributes less than 20% as a down payment for a conventional mortgage.

- A borrower pays private mortgage insurance, and it protects the lender in case the borrower defaults on their mortgage.

- Annual PMI premiums usually range from 0.5% to 2% of the outstanding principal, and it depends on how risky the borrower is.

- Private mortgage insurance is not required once the loan-to-value (LTV) ratio of the mortgage lowers to 80%, but it is canceled automatically only when LTV reaches 78%.

What Is Private Mortgage Insurance (PMI)?

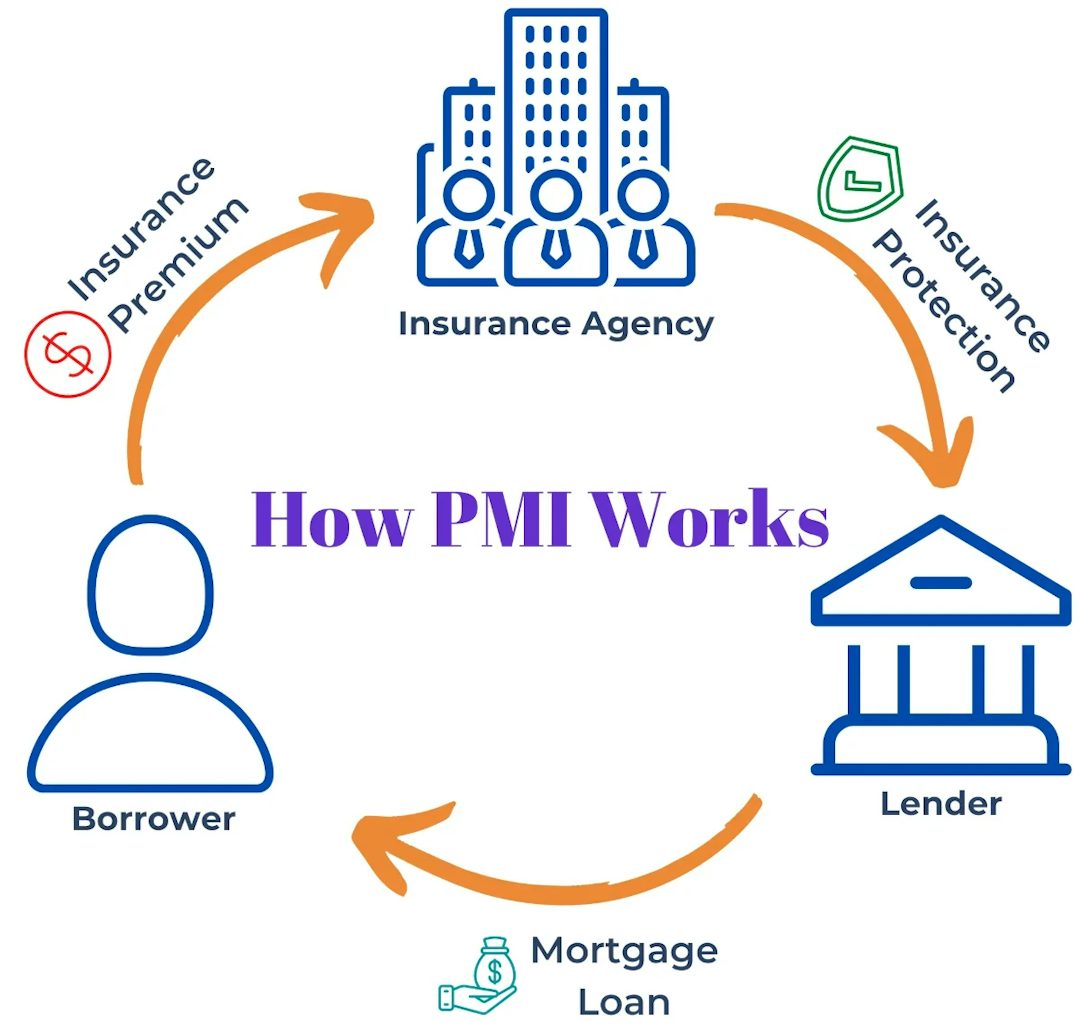

Private mortgage insurance, also known as PMI, is a form of mortgage insurance for conventional loans. The borrower purchases private mortgage insurance, and it protects the lender in case the borrower defaults on their mortgage. Even though PMI does not benefit borrowers, some borrowers may be required to take them if they are considered too risky. Usually, PMI is required for conventional loans that have a loan-to-value (LTV) ratio higher than 80%. Mortgage insurance protects the lenders in case the borrower defaults on their loan, which allows the lenders to issue conventional mortgages with down payments as low as 3%.

Private mortgage insurance is an expense that in many cases should be avoided regardless of the cost. This kind of insurance is paid by the borrower and it protects a lender, which means that the borrower should try to avoid getting this insurance. On the other hand, some borrowers may need to get PMI because it is the only way for them to receive a mortgage in the first place. In these cases, the borrower should be aware of how exactly the cost of PMI is being composed to ensure that they are paying the lowest rate possible.

How to Calculate PMI

To use the PMI calculator provided above, there are some property-specific values required to be inputted to complete the calculations. First and foremost, if your down payment is 20% of the home purchase price or more, you will not need to pay for private mortgage insurance at all. If your down payment is less than 20%, then you can estimate the cost of private mortgage insurance. The following values are needed to calculate your monthly mortgage insurance premium:

- Home Purchase Price - When all other variables stay fixed, the higher the home purchase price, the higher your private mortgage insurance will be. This is because the mortgage insurance rate is multiplied by the loan amount to find your annual mortgage insurance. For the same down payment, a higher home purchase price means that the loan amount will be bigger, and this exposes the lender to more risk, therefore the private mortgage insurance premiums will be higher as well.

- Down Payment Amount – The down payment you make is deducted from the home purchase price to find out how much financing you will need from the lender. Your private mortgage insurance premiums will be determined based on the amount you borrow.

- Mortgage Insurance Rate – As mentioned above, the mortgage insurance rate is multiplied by the loan amount to find out the premium. A higher mortgage insurance rate means that you will pay a bigger amount on private mortgage insurance.

Example – Calculating PMI

You want to purchase a home that costs $350,000. Since you can only afford to put a 15% down payment, you are required to pay for private mortgage insurance. Your lender notifies you that your mortgage insurance rate will be 0.55%. How much will your monthly PMI premium cost?

- Down Payment = 15% * $350,000 = $52,500

- Loan amount = Home Purchase Price – Down Payment = $350,000 - $52,500 = $297,500

- Annual PMI = Loan Amount * Mortgage Insurance Rate = $297,500 * 0.55% = $1636.25

- Monthly PMI = $1636.25 / 12 = $136.35

You will have to pay approximately $137 each month for PMI.

To find out the total PMI premium, the loan interest rate and loan term will be needed. These inputs are used to find out when you will reach an LTV of 80% so that your PMI can be removed. The total PMI premium is determined depending on the mortgage term and interest rate. It is important to note that this PMI calculator works only for borrower-paid mortgage insurance. It may not be accurate for all other types of private mortgage insurance.

The Cost of Private Mortgage Insurance

As of 2022, Freddie Mac estimates that PMI costs $30 to $70 per month for every $100,000 borrowed. In other words, annual PMI premiums usually range from 0.5% to 2% of the outstanding principal. There are specific factors that may affect how much a borrower will have to pay for Private Mortgage Insurance. These factors are usually related to the risk profile of the borrower. This means that the insurer will require a higher premium if the borrower is more likely to default on their loan. A borrower should consider the following factors before getting private mortgage insurance:

- Credit Score - The credit history and credit score play an important role in all lending practices. A person with a low credit score or poor credit history is considered to be more likely to default on their loan than a borrower with a high credit score. This is an easy risk factor for the insurance agency to receive and analyze, so it is used widely to set the private mortgage insurance premium. A borrower should get their credit score and see whether it requires improvement before getting PMI.

- Loan-to-Value (LTV) - This ratio is another important factor that affects the premium. The insurance companies recognize that the LTV ratio can directly affect the willingness of a borrower to pay off their mortgage. If the loan-to-value ratio is too high, then the insurance companies may require a higher premium. As a rule of thumb, a borrower does not need private mortgage insurance when their LTV is less than 80%. On the other hand, their premiums will increase as their LTV increases from 80% to 97%. It is unlikely that a lender would issue a mortgage with LTV over 97%.

- Loan Type - Private mortgage insurance is used for conventional loans, but they may behave differently depending on the type of interest rate the loan has. There are usually fixed and adjustable rate mortgages. Fixed-rate mortgages tend to be less risky because the borrower knows exactly how much they need to pay monthly. On the other hand, adjustable rate mortgage payments may spike unexpectedly and lead to default. Since adjustable rate mortgages tend to be more volatile, they are considered riskier. This means that the insurance company would set a higher premium for adjustable rate mortgages.

- Loan Size - The dollar amount of the principal, is also an important factor for deciding what premium to charge a borrower. The larger the loan size, the larger the loss an insurance company may incur if a borrower defaults. In that case, the insurance companies may add an extra premium even though it is always proportional to the loan size anyways. Generally, this risk factor applies to jumbo loans with an outstanding principal that surpasses conforming loan limits.

- Insurance Term - Choosing the insurance term does not directly relate to the risk profile of the borrower, but it is important to note that it takes time and effort to issue insurance. Insurance companies are more willing to issue longer-term insurance policies rather than shorter-term ones. Because of that, a borrower has a good chance of getting a reasonable discount on their premiums if they choose a longer insurance term.

Types of Private Mortgage Insurance

There are various types of PMI based on how the payment is structured:

- Borrower Paid Monthly Mortgage Insurance (BPMI) - This is the most common type of PMI where your mortgage insurance is included in your monthly payments thereby increasing your monthly expense. This type of PMI works best if you are unsure of how long you are planning on keeping the mortgage because there is no upfront cost to you.

- Single Premium Mortgage Insurance (SPMI) - In this form of PMI, instead of doing monthly payments, you decide to pay the total PMI amount upfront thereby not increasing your monthly payments. This form of PMI would be suggested if you have funds available at the closing of the home, and that way your monthly expense will remain lower. An advantage of this form of PMI is that it might help you qualify for a larger home loan because you paid the PMI upfront.

- Lender Paid Mortgage Insurance (LPMI) - Although this sounds great that the lender is footing the bill for the mortgage, it is a bit more complicated than that. The lender indeed does pay the PMI, but they also increase the interest rate on your loan in order to cover the PMI. Essentially you pay for the PMI by getting a higher interest rate on your home loan. The disadvantage of this type of PMI is that the interest rate does not reduce once you reach a loan-to-value of 78% because you’re locked into that interest rate.

- Split-Premium Mortgage Insurance - This is the least common type of PMI as it is a combination of monthly paid insurance (BPMI) and single premium insurance (SPMI). The way this type of PMI works is that you pay a portion of the PMI upfront and pay the rest of the PMI in monthly payments as part of the mortgage payments. This might be used by individuals who cannot pay the entire PMI upfront but can cover a portion in order to reduce their monthly costs. For example, on a $500,000 home, with a PMI rate of 1.5%, the total PMI amount is $7,500, but if you decide to pay $3,000 upfront, only the remaining amount of $4,500 is added to your monthly mortgage payments for the first year.

How to Remove PMI

There are multiple ways to remove PMI, but they all require some contributions from the borrower. PMI for home loans can be removed in one of the following ways:

- LTV Ratio Reaches 78%– If you make enough payments such that your LTV is 78%, then PMI should automatically be removed by the insurer. You can also get PMI manually removed when you have 20% ownership of the house, but you will have to reach out to your insurer to get it removed. In most cases, it takes homeowners 11 years to own enough equity in the home to get PMI removed. For example, on a $300,000 home price, if you have $234,000 outstanding in your mortgage, then you have achieved 78% LTV ($234,000/$300,000) and PMI would be removed.

Example: LTV Ratio

The LTV or loan to value ratio is the portion of the value of the house that you are borrowing through a mortgage. In other words, the percentage of your home’s value that is financed by the mortgage. Imagine that you want to purchase a house that costs $100,000 and you can only afford to make a 10% down payment. What is your LTV ratio?

Down Payment = 10% x Home Price = 10% x $100,000 = $10,000

Mortgage Amount = Home Price - Down Payment = $100,000 - $10,000 = $90,000

LTV Ratio =

Mortgage Amount

Home Value

=

$90,000

$100,000

= 90%

- Halfway Point of a Mortgage Term Is Passed - On a 30-year mortgage, for example, PMI must be removed 15 years into the loan. This is true even if the LTV on the mortgage still exceeds 80%.

- Mortgage Is Refinanced - The last way to get rid of PMI is to refinance your mortgage such that the new loan balance is less than 80% of the home’s current value. This will allow you to avoid paying PMI after the refinancing of the mortgage.

Private Mortgage Insurance Companies

MGIC – Mortgage Guaranty Insurance Corporation

MGIC is a subsidiary of MGIC Investment Group and it provides private mortgage insurance to lenders of home mortgages across the U.S. The company offers primary coverage and pool insurance. Primary coverage gives the opportunity to people to become homeowners with less than 20% down payment and protects the lender against default. Pool insurance covers losses that are bigger than claim payments in the case of default. Mortgage Guaranty Insurance Corporation currently operates in all the states of the U.S., Puerto Rico, and Guam. MGIC is one of the largest private mortgage insurance companies which has more than 20% share in the market of PMI providers.

Radian Guaranty Inc.

Radian Guaranty Inc is the primary subsidiary of Radian Group. The subsidiary is in the business of providing private mortgage insurance to lenders and offers various mortgage, real estate, and title services. Radian Guaranty Inc. provides PMI on first-lien mortgage accounts and pool insurance. Currently, Radian works with more than 3,500 residential lenders to make homeownership possible for Americans. Its revenues account for half of the total revenues of its parent company.

Essent Guaranty Inc.

Founded in 2008, Essent Guaranty is headquartered in Pennsylvania and is a subsidiary of Essent Group. To protect home mortgage lenders and mortgage investors, the company offers mortgage insurance and loss management services. The company is approved by Fannie Mae and Freddie Mac and is currently licensed in every state in the U.S. and the District of Columbia.

National Mortgage Insurance Corporation

National MI is another U.S.-based top company that specializes in mortgage insurance and risk protection services for mortgage lenders and investors. The parent company of National MI is NMI Holdings. NMI Holdings ranked 24th in Fortune's list of 100 Fastest-Growing Companies for 2020. Moreover, National MI has been recognized by Fortune in the list of Best Workplaces in Financial Services and Insurance in March 2021.

PMI on FHA Loans

FHA loans are a type of non-conventional loans backed by the Federal Housing Administration in the U.S. FHA loans offer various advantages to conventional loans. For starters, FHA loans have looser financial requirements for borrowers and allow for smaller down payments. Since these are government-backed loans, it means that in the case that the borrower defaults on their payments, the government agency will partially or fully pay the lender for the losses incurred. This is why lenders can assume a bigger risk and offer more favorable requirements. For example, if you have a credit score of at least 580, you can qualify for an FHA loan with only 3.5% down payment. When your credit score is between 500 and 580, you would have to put at least 10% down.

Conventional loan PMI and FHA MIP are different. While conventional lenders use PMI, FHA lenders protect themselves by charging an FHA mortgage insurance premium against borrowers who present a high risk of default. You can use our FHA MIP Calculator to estimate your mortgage insurance premium on an FHA loan. MIP is typically made of an upfront payment of around 1.75% of the loan amount and an annual premium that ranges from 0.45% to 1.05% of the loan amount. That is why MIP often proves to be more expensive than PMI. Key differences between MIP and PMI include the following:

- Upfront Premium - As mentioned above, MIP requires the borrower to pay an upfront premium of 1.75%. This premium can either be paid upfront or can be rolled over into the loan balance. If you choose to go with the second option, the higher loan balance will lead to a higher interest expense. PMI, on the other hand, only requires an upfront payment if you are getting Single-premium mortgage insurance or Split-premium mortgage insurance.

- Canceling Mortgage Insurance - The biggest difference between MIP and PMI is that you cannot cancel your mortgage insurance with MIP once you reach 20% equity in your home. If you have initially put at least 10% down, you are required to pay MIP for 11 years of the loan. On the other hand, if you have put a down payment of less than 10%, you are required to pay MIP for the whole life of the loan. The only way that you can stop paying for MIP is if you refinance your FHA loan into a non-FHA loan product.

- Contribution by Seller - With FHA loans, the seller is permitted to contribute to closing costs up to 6% of the home’s purchase price. This is known as seller credit, and it means that the seller can also pay for some or all of the upfront mortgage premium. In conventional loans, sellers are allowed to contribute up to only 3%.

| PMI | FHA MIP | |

|---|---|---|

| Payment Structure | Annual Fee (Except for SPMI and Split-Premium Mortgage Insurance). | Upfront Payment + Annual Fee. |

| Mortgage Insurance Rate | 0.55% - 2.25% | Upfront: 1.75% Annually: 0.45% - 1.05% |

| Down Payment | < 20% | Not Applicable. |

| Credit score | Has an impact on the rate. | Does not have an impact on the rate. |

| Cancelation | Once an LTV ratio of 78% is reached. | After 11 years – for down payments of at least 10%. For the entire loan term – for down payments of less than 10%. |

| Lender | Private Institutions. | FHA-Approved Institutions. |

Frequently Asked Questions

Do I need to get PMI?

The lender will require you to get PMI or insurance for your loan if you decide to put less than a 20% down payment of the total loan amount. For example, if the total mortgage amount is $300,000 and you only have $45,000 for the down payment, which is 15% and is less than the required 20%, then you will need to buy PMI for the home loan. It may be useful to estimate your jumbo loan eligibility before applying for it.

How Is PMI Calculated?

The coverage a private mortgage insurance company offers determines what portion of the amount lost the lender will be able to recover in the case that the borrower defaults on their mortgage. For example, if the PMI provider provides 30% coverage, this means that the lender will be paid back by the insurer for 30% of the losses related to the borrower’s default. These losses can include the unpaid principal balance, interest that the lender would otherwise get, and 30% coverage for the lenders’ costs associated with the borrower’s default and home foreclosure.

Higher coverage means that the borrower will pay higher insurance premiums. When the lender is lending a lot of money to the borrower and there is a high risk of default, the lender can agree to lend if they are protected by greater insurance coverage. The PMI company will provide this coverage at a higher cost that the borrower will have to bear.

Is PMI Tax Deductible?

PMI can be tax deductible, but it may not always be a good idea to deduct it. Just like other forms of mortgage insurance, PMI can be deducted when you file your income tax return as an itemized deduction, but it cannot be deducted as a standard deduction. With the Further Consolidated Appropriations Act of 2020, US Congress allowed for deductions until December 31st, 2020. It is also available for 2019 and 2018.

Why Do I Need to Pay For PMI When It Benefits the Lender?

The reason for this is that the lender is taking on additional risk by lending to you while you’re putting up less money upfront (<20% down payment) and can default on future payments. However, it is important to understand that it is beneficial for you too because if PMI or insurance was not an option, lenders may not have offered a mortgage for anything less than a 20% down payment, preventing a lot of individuals from becoming homeowners.

PMI also has an additional benefit because lenders can give you a better mortgage rate if you take PMI. The reason for this is that PMI allows lenders to recover a greater portion of their investment as compared to individuals who do not take PMI, allowing them to give you a better rate on your mortgage.

How Do I Pay For PMI?

Depending on the type of private mortgage insurance, you may have different options to pay for PMI. For example, if it is a single-premium or split-premium mortgage insurance, then the premiums may be paid directly to the insurance companies at the time of insurance origination. On the other hand, if the mortgage insurance is borrower-paid or lender-paid, then there are a few ways a borrower may pay for PMI.

- Premium can be added to the mortgage payments. The exact amount paid in premium is disclosed in the closing disclosure at the time of loan origination. The borrower should refer to the closing disclosure to find all information regarding the PMI premiums and terms.

- Premium can be partially paid upfront and periodically. In this case, the borrower will have to pay a certain fee upfront while the other fees would be rolled into the mortgage. To find the fees paid with the mortgage, the borrower should refer to the closing disclosure to find all relevant information on PMI premiums.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.