Construction Loans

CASAPLORER®Trusted & TransparentWhat You Should Know

- Most construction loans have high interest rates and a short maturity term of about a year.

- Getting a construction loan requires a lot of planning because lenders want to see a clear construction plan before issuing this type of loan.

- If a borrower already has equity in a property, they can get a home equity loan that is cheaper and much easier to get than a construction loan.

- A construction loan origination process is very similar to a mortgage loan process except for the fact that a borrower has to present a clear construction plan before receiving a loan.

What Is a Construction Loan?

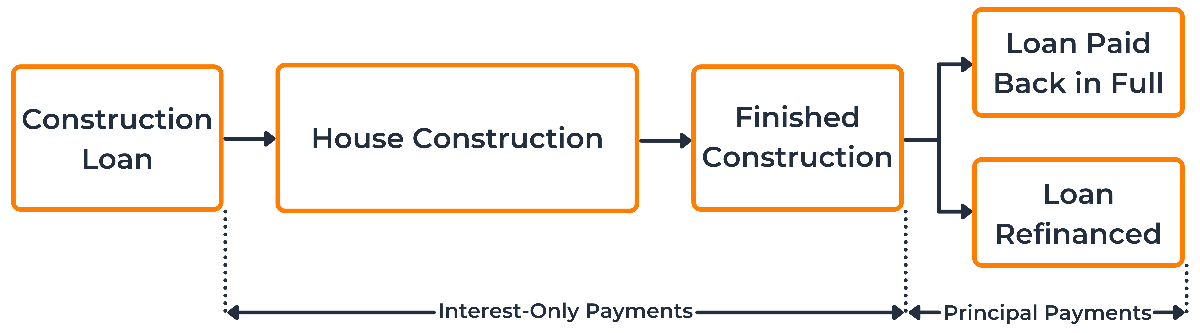

A construction loan is a short-term loan that usually has a high interest rate and is used to fund construction projects. Usually, a construction loan is issued for up to 12 months. Since it has a high interest rate, the borrowers of these loans tend to either pay off or refinance the loan as soon as the construction is completed. This type of loan can be useful for people who cannot find a suitable property on the market, so they choose to build the property themselves.

Construction loans usually have a higher interest rate than mortgages because when a construction loan is originated, there is no physical collateral hypothecated for the loan. Since a property is only about to be built, construction loans tend to be considered much riskier than mortgages with a pledged collateral. Additionally, construction loans have an adjustable interest rate, which means that the interest rate charged on the principal changes as the prime rate changes. When the construction is finished, the borrower has an option to refinance the loan into a mortgage or pay off the principal at once.

How Do Construction Loans Work?

Getting a construction loan involves a lot of planning. When lenders issue a loan, they want to ensure that they will be able to get their money back. In case of mortgages, the lenders take a property as a collateral. This collateral protects the lender in case a borrower defaults on their loan. When it comes to a construction loan, the lender cannot get a property as a collateral because the property is yet to be built. Because of that, the lenders want to see a clear and detailed plan that shows a step-by-step construction process to determine whether a borrower is eligible for a construction loan.

If a borrower is able to provide a clear construction plan, then they might be able to receive a loan. The loan itself has different features than a conventional loan. First, it usually has an adjustable interest rate, which means that the interest rate will vary depending on the prime rate. The interest rate on a construction loan itself is much higher than for a mortgage because a construction loan is much riskier for a lender than a mortgage. Lastly, construction loans usually have an interest-only component in them. Borrowers usually pay only interest on construction loans up until construction is completed. When construction is completed, a borrower has an option to pay off the principal at once or refinance it into a mortgage. It is important to note that construction loans are typically issued for 12 months only. If a construction project requires extensions, then the borrower risks paying monthly extension fees. Depending on the lender and the size of the project, the extension fees can vary from a few hundred dollars per month to a few thousand dollars per month. Regardless of how much exactly a borrower has to pay, the loan may become very costly because of the extension fees.

Unlike a traditional loan where a borrower receives a lump-sum payment at the origination of the loan, the lender pays the contractor directly in phases, known as “draws”. This helps mitigate the risk for the lender and allows them to track the construction process. The contractor receives funds for every draw which is linked to an important phase of the home construction process, such as building the foundation, home framework, roofing, and finishing. Each time funds are to be disbursed, an inspection is required by an agent to track the process and determine the amount of funds needed.

Since the lender does not issue a full loan amount at the time of loan origination, the borrower pays the interest only on the outstanding amount. For example, suppose there are 4 draws in the construction process, each draw is $100,000, and the monthly interest rate charged is 1.5%. In this case, the borrower’s payment schedule while the construction is in process will look as follows.

| Loan Draws | Principal Outstanding | Monthly Interest-Only Payments |

|---|---|---|

| Draw 1 | $100,000 | $1,500 |

| Draw 2 | $200,000 | $3,000 |

| Draw 3 | $300,000 | $4,500 |

| Draw 4 | $400,000 | $6,000 |

Types of Construction Loans

There are 3 types of construction loans available. They are very similar in their structure and purpose, but they have certain differences that make some of them be more favorable over the others. The main differences appear in the interest rates offered, closing costs and repayment phase. The following table summarizes these features for all 3 construction loan types.

| Loan Type | Repayment | Closing Costs | Interest Rate |

|---|---|---|---|

| Construction Only | Paid Back in Full | Paid Twice | Variable |

| Construction-to-Permanent | Converts to a Mortgage | Paid Once | Fixed |

| Owner-Builder Loan | Paid Back in Full | Paid Twice | Variable |

| Renovation Construction | Paid in Installments | Paid Once | Depends |

Construction Only Loan

Construction only loan is the most flexible type of loan because it allows a borrower to choose between refinancing or paying off the loan at the maturity date. When a borrower gets a construction only loan, they only borrow money to finance the cost of building a property. Once the home is completed the loan is paid back in full to the original lender. This means that if the borrower has the ability to pay off the loan, they can pay it off without getting a mortgage. On the other hand, if the borrower cannot pay it off, they have an option to get a mortgage and pledge their newly built property as a collateral. In this case, the mortgage lender will pay off the construction only loan in full and receive mortgage payments from the borrower.

The lender of a construction only loan transfers the funds directly to the contractor in “draws” and the borrower is required to make interest-only payments on the principal amount outstanding. This means that the interest-only payments will increase as the construction progresses because the outstanding principal will be increasing. Additionally, the construction only loan usually charges a variable interest rate, which means that the interest rate will vary depending on the prime rate.

The biggest advantage of this type of loan is that it provides flexibility and an option to find the best mortgage lender if needed. With this loan, a borrower has the flexibility to find the best mortgage lender that can satisfy their financial needs. Additionally, the borrower has a lot of time to negotiate and thoroughly discuss the terms of the mortgage, which may lead to more favorable interest rates and a payment schedule. On the other hand, the downside of this type of loan is the extra cost associated with getting another loan. Any time a loan is originated, a borrower has to pay closing costs that may account for 3% - 6% of the loan value. As there are two different loan processes, a borrower has to pay closing costs for two loans: construction only loan and mortgage loan. The closing costs associated with the two loans may increase the overall costs of construction and the mortgage by a large margin. Apart from costs, a borrower will have to spend extra time on paperwork for both loans.

With these characteristics, this type of loan is fit for people who would like the flexibility that comes with the loan. If a person knows that they are able to pay off the loan in full at the time of expiration, they may prefer this loan to other loans. Additionally, if a borrower expects to receive a lower interest rate for a mortgage later on, then they may also choose this type of loan over others. As long as a borrower believes that the value of extra closing costs is lower than the value of savings that come with mortgage refinancing, the borrower should choose a construction only loan.

Construction-to-Permanent Loan

Construction-to-Permanent loans provide funds to cover the construction costs, which are then rolled into a mortgage once the construction is completed. Usually, a borrower has an option to either pay back the loan or refinance it into a mortgage once the construction is over. A construction-to-permanent loan allows a borrower to refinance the loan into a mortgage without paying additional closing costs for mortgage origination. A borrower receives the funds to build a property and once the home is completed, the loan is converted into a mortgage without any extra costs. The structure of this loan is very similar to an interest-only mortgage where a borrower pays only interest for some time before starting to amortize the principal. There are various construction-to-permanent loans available. Even some government agencies offer their own construction loans. For example, The US Department of Agriculture offers a USDA Construction Loan that works as a construction-to-permanent loan.

The biggest advantage of this loan is that a borrower has to pay closing costs only once at the origination of construction loan. As the loan converts into a mortgage, a borrower does not need to be worried about the costs associated with getting a mortgage and going through the application process again. One of the disadvantages of this type of loan is that a borrower is locked into a mortgage rate with certain terms almost a year before their mortgage starts. This means that if the interest rates fall during that year, the borrower will not be able to benefit from the lower interest rates when it is time to pay for the mortgage.

This option is great for borrowers who have a clear construction and repayment plan with a fixed interest rate. If a borrower understands how exactly the property will be constructed, how much time it will take, then they will be able to complete the project in the allocated time frame. A clear understanding of how the mortgage will be paid off will help the borrower make an educated decision about their ability to pay off the mortgage at an interest rate provided at the time of loan origination.

Owner-Builder Loan

Owner-builder loans are very similar to a construction only loan. The only difference between the two is the absence of a contractor who works on a project in an owner-builder loan. A construction only loan pays a contractor to work on the construction project in “draws”. An owner-builder loan implies that the owner of the property works on the project, so there is no contractor. In this case, the lender pays the owner the same way they would pay a contractor. The owner has to work on the project and provide updates to the lender. The lender, in turn, provides funds in draws to the owner to work on the project. Owner-builder loans tend to have a lower value simply because the owner does not have to pay salary to a contractor, which lowers the cost of a construction project.

Renovation Construction Loan

There are multiple renovation construction loans available, and they all can be categorized as home improvement loans. Even though these types of loans can be used for a construction, they are quite different from the other two loans described above. These loans are suitable for homes that are already built but require costly renovations and upgrades. There are various renovation loans available depending on the loan amount, loan term, flexibility and requirements.

If a homeowner has a small project that requires less than $20,000, then a personal loan may be a great option. No collateral is required, and the application process is relatively quick. A borrower can receive the funds within days of the application and repayment period can stretch for 2 – 5 years. Since there is no collateral backing the loan, the interest rate on this type of loan tends to be higher than for alternatives.

If a homeowner has lived in their property for some time and has built up home equity, then they may consider getting a HELOC or a home equity loan. These loans allow a homeowner to get a loan with an interest rate close to a mortgage rate. Usually, a lender is willing to lend out enough cash for a loan-to-value (LTV) ratio to be equal to 80% on the property used as a collateral. Home equity loans can extend for up to 20 years giving a borrower enough time to plan and repay the loans. These loans are perfect for large well-planned projects such as finishing a basement or building a pool. A hard money loan may also be a good option for well-planned projects as long as the borrower has a clear understanding how they will repay the loan. One large disadvantage of hard money loans is that they are much more expensive than other construction loans.

The last viable option available for construction and home renovation projects is a cash-out refinance. In a cash-out refinance a homeowner borrows more funds than needed to pay off their outstanding mortgage. Using this technique, a borrower can pay off their existing mortgage and have some cash left for a construction project. The main advantage of this strategy is that a borrower is left with a single loan that encompasses both the mortgage and the construction loan. The amount a borrower can get using a cash-out refinance depends on many variables, so it might be wise to estimate how much a borrower can get using a cash-out refinance calculator.

How to Get a Construction Loan?

Depending on what type of construction loan a borrower chooses to get, they may need to provide different documentation. The easiest way to get a loan for a construction is through renovation construction loans such as HELOCs and personal loans. On the other hand, if a borrower does not have a property to put as a collateral, then they may need to get either a construction-to-permanent loan or construction only loan. These loans are more difficult to get because they require a detailed construction plan that has a clear time frame for each step of the project.

Before getting a construction loan, a borrower should ensure that they can qualify for this type of loan. Construction loans usually have higher qualification requirements than mortgage loans mostly because construction loans are not secured with a collateral. To qualify for a construction loan, a borrower must have a credit score of at least 620 points and a minimum down payment of 20%. Even though the minimum down payment required is 20%, a vast majority of lenders require a down payment of 25% for construction loans. Many lenders also look at the debt-to-income (DTI) ratio, which should be less than 45% to qualify for a construction loan. Lastly, a borrower should prepare a clear and realistic construction and loan repayment plan to increase their chances of getting a construction loan. A construction plan should have a clear outline of the project with dates and funds required at each step. A repayment plan is referred to the way how a lender will receive the principal amount after the construction is complete. Usually a repayment plan includes taking a mortgage loan on the newly built property, but it may also include the borrower’s way to pay off the loan in cash.

When a borrower ensures that they meet the minimum requirements, they can start working towards getting a construction loan. The process of getting a home construction loan is very similar to the process of getting a mortgage. The process usually includes the following steps.

- Find a Lender

A borrower should do research on the different lenders that offer construction loans to find the best match given their financial situation. A borrower should choose a lender that best satisfies their financial needs that may include a low interest rate or specific repayment terms. Sometimes lenders require a construction plan or a budget for the project. It might be useful to estimate the budget before asking for a loan. It might take time, but it is possible to estimate how much each item will cost. For example, a concrete calculator can help you estimate the amount of concrete needed for a project.

- Get a Pre-Approval Letter

Once a borrower finds the best lender given their financial needs, the borrower can get a pre-approval letter that will state how much a lender is willing to lend out, at what interest rate and for what term. During the pre-approval process, a lender will analyze the financial information of a borrower to determine their risk level. This step is crucial for a borrower to ensure that they can get enough money to fund their construction project in full. A pre-approval for a construction loan will likely be contingent on a clear construction plan, which means that the borrower will be able to get a loan only if they can provide a clear construction plan that satisfies the lender.

- Find a Location

When a borrower knows how much they can allocate for their project, they should find an appropriate location. If a borrower already has a piece of land in mind for the project, they can move on to the next step. If a borrower is yet to find a location, they must keep in mind that land costs money, and they must budget the purchase of land into the project. Estimating your land loan payments can help with budgeting your costs.

- Find a Licensed Contractor

A lender will be providing money for the project directly to a lender. It is important to find a licensed contractor to participate in this deal because otherwise a lender may not be willing to approve a loan. Finding a licensed contractor can be done through referrals or through special directories such as NAHB’s directory of local home builders’ associations. It is also wise to look at multiple contractors to get the best deal.

- Plan the Construction Project

This is a crucial step for getting a construction loan. Even if a borrower is pre-approved for a construction loan, it is likely contingent on the presence of a clear construction plan. This means that a lender will require a clear construction plan before issuing a loan. If the borrower does not have a clear plan, then it is likely that the lender will decline a loan request.

- Get the Loan

When a borrower has a clear construction plan ready, they can apply for a loan. At this point, the lender will look into the financial situation of a borrower one more time to ensure that they can pay off the loan. If the lender is satisfied with the construction plan and financial situation of the borrower, the borrower will get a loan.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.