Mortgage Preapproval

What You Should Know

- A mortgage pre-approval allows a borrower to estimate how large and at what interest rate a certain lender is willing to provide a loan to them.

- Mortgage pre-approvals require a borrower to submit financial information such as tax returns, pay stubs, a social security number, and credit history.

- Having a mortgage pre-approval letter can make a homebuyer’s offer more competitive, and it can also provide an insight into the homebuyer’s budget.

- Mortgage pre-approvals typically expire 30 to 90 days after they are issued, so the borrower has to reapply for a mortgage pre-approval once the previous document expires.

What Is Mortgage Pre-Approval?

A mortgage pre-approval is a process when a mortgage lender looks at a borrower’s financial information, qualifies the borrower for a specific mortgage loan, and provides some mortgage-related details such as the maximum principal a borrower is pre-approved for, set interest rate, and the expiration date of the pre-approval. The borrower can see all the information related to the mortgage they are pre-approved for, in a pre-approval letter issued by the lender. A pre-approval letter provides terms and conditions that must be met for a lender to issue the borrower a mortgage. If the borrower does not meet any of the conditions, the borrower may not get a mortgage even though they got pre-approved.

Every lender evaluates a borrower’s financial situation and ability to pay off a mortgage before issuing one. Lenders analyze the borrower’s financial situation during the pre-approval process too, and based on this information, they pre-approve a borrower for a certain mortgage amount with a certain interest rate. A pre-approval letter that is issued once a borrower is pre-approved, shows that a mortgage lender is willing to let the buyer borrow money for a home loan, and it provides an amount for which the buyer is pre-approved. If the property is too expensive for the buyer, the seller can see it in the pre-approval letter, which can save time for both the buyer and the seller.

The pre-approval amount is based on the borrower’s income, debt, assets, and credit history. Lenders can provide a letter informing a borrower of the type of mortgage they are eligible for, the monthly mortgage payment that they can pay for, and what mortgage rate they can receive. Mortgage borrowers should be aware that every lender has its own criteria to determine the amount they are willing to lend and the interest rate they are willing to set. Because of that, even if a lender pre-approves a borrower for the amount the borrower needs, the borrower should still shop around and see what lender can offer the best mortgage rate as well as general mortgage terms. It is also important to note that even though a lender pre-approves a borrower for a certain amount, it does not mean that the borrower can afford to get such a large mortgage. It is best to be moderate and make sure that you can afford monthly payments, maintain your current lifestyle and stay on track with your financial goals.

Mortgage pre-approval is used as a good estimate to guide a borrower through their home buying process. Online mortgage pre-approval calculators can even estimate how much a borrower can be pre-approved for. Once a person is pre-approved for a mortgage, the borrower should make sure to follow the conditions of the pre-approval. A pre-approval letter is a binding document that obligates the lender to issue the mortgage loan on the conditions outlined in the pre-approval letter if all other conditions are satisfied. Depending on the lender, the conditions may change, but they usually relate to property value, the borrower’s financial situation, or economic conditions. If some conditions of the pre-approval letter are broken, the lender has the right to decline the mortgage loan or offer another loan product.

Benefits of Mortgage Pre-Approval

When a seller tries to sell their property, the seller usually wants to see that a buyer can purchase the property. To ensure that a buyer can purchase the property, a seller usually requires them to provide a pre-approval letter and a proof of funds (POF) letter . This means that even if the buyer knows that they can get a mortgage, they may have a hard time starting a deal with a seller without any proof. From the point of view of the seller, they would strongly prefer to make a deal with a buyer who has proof that they can purchase the property.

There are many other reasons why a buyer may want to get pre-approved even if they are not planning to purchase a property any time soon. Getting pre-approved may provide insights into financial issues a borrower may have. If a borrower identifies these issues early enough, they can work on them, which will allow them to get a higher loan limit and a lower interest rate in the future. Generally, there are 3 main reasons why getting pre-approved is beneficial before purchasing a property:

- Home Affordability: Once you are aware of the amount you can afford, it will give you confidence in your search and you won’t have to spend beyond your planned amount. It will also ensure you are realistic and do not go for houses that you cannot afford.

- Closing Advantage: The lender will already have most of the financial information that they need from you, helping to make the closing process faster when it comes time to apply for mortgage approval.

- Credibility: Sellers will be confident in your ability to finance the payment. This will help give you an edge over a buyer who does not have a pre-approved mortgage letter.

How Does Mortgage Pre-Approval Work?

Pre-approval process and timeframes may vary depending on the lender a borrower is trying to get pre-approved with. This process may take time, but it is ultimately done to save time and have more certainty at the time of buying a house. Understanding how mortgage pre-approval works may help a buyer get the most use of this process by reducing the mortgage application waiting period and building certainty about what mortgage they can receive.

Mortgage preapproval is not mortgage underwriting even though both of processes share similar steps. The mortgage pre-approval process starts with a mortgage pre-approval application. Most lenders will require common information for borrowers such as their Social Security number, bank statement, pay stubs, and others. Even though different lenders make a decision based on different factors, most lenders will require the following information before completing the application process:

- Personal Information: First and last name, phone number, email address, current mailing address, and Social Security number.

- Loan Information: If a borrower has not signed a purchase contract yet, for example when they are still searching for a home or are just starting their home search, then the borrower will be asked how much down payment they are planning on making. This can be either a down payment amount or a down payment percent. Otherwise, if a borrower already has a purchase contract, then they will be asked for the home sale price along with the down payment amount.

- Employment History: This section usually requires names and addresses of the borrower’s current and previous employers, job title, years on the job, and gross income.

- Financial Information: List your bank accounts and the balance of each account, the total value of your investments, and the value of any real estate properties owned, such as your primary residence, second homes, and investment properties. You'll also state your debt and other obligations, such as current monthly mortgage or rent payment, real estate or property taxes, and home insurance premiums.

- Other Information: If you are purchasing a home with a co-borrower, you'll need to provide your co-signer's personal information as well. You may also be asked for your real estate agent's name and phone number.

Once the application is submitted, the lender will analyze the information submitted and either issue a pre-approval letter or decline the request. The loan offered depends on a lender’s objectives and risk tolerance, but there are a few common factors most lenders require borrowers to meet.

Once a pre-approval letter is issued, a borrower can find a lot of useful information that is directly related to the conditions offered for their loan. Depending on the lender, the conditions may differ, but all lenders usually include the maximum principal amount, interest rate, and down payment.

The letter is usually valid for 60 to 90 days although some lenders may issue them for as short as 30 days. This means that the borrower who received a pre-approval letter may be able to get a mortgage according to the terms outlined in the letter until it expires. If the letter expires, the borrower will have to reapply and wait for some time for a lender to analyze their finances and approve them for a mortgage again. This is important when a borrower is planning to purchase a house that needs to be sold fast. For example, if a seller tries to short sell their property, a borrower with an expired pre-approval letter may not be able to close the deal fast enough and lose it as a result.

Even though a pre-approval letter has an expiration, a borrower may benefit from getting a pre-approval letter early because it can provide some insights into the financial issues the borrower may have. Getting a pre-approval letter early allows a borrower to work on their financial situation to increase their chances of approval later on. Additionally, if a borrower is able to improve their financial situation drastically, they may be able to lower their interest rate and save a lot of money down the road.

Factors That Affect Mortgage Pre-Approval

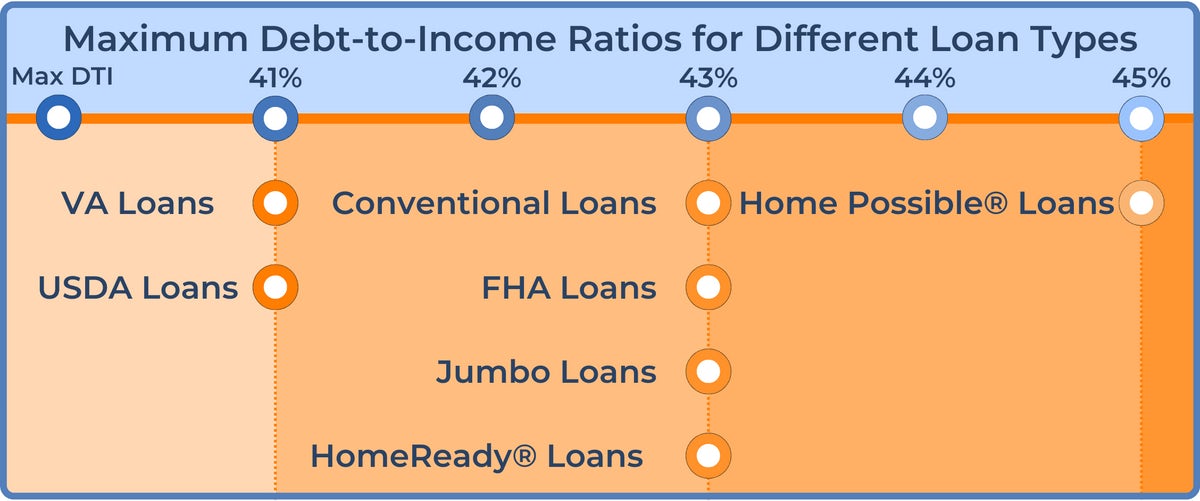

There are many criteria that may affect the outcome of a lender's analysis of a borrower. The type of loan a borrower is applying for also matters because different loans may be backed by different agencies and may have different requirements. This means that a borrower should see what type of mortgage they can be pre-approved for and see what mortgage is the best for their situation.

| Mortgage Type | Min Down Payment | Credit Score | Max DTI Ratio |

|---|---|---|---|

| Conventional | 3% | 620 | 43% |

| FHA | 3.50% | 580 | 43% |

| VA | None | None | 41% |

| USDA | None | None | 41% |

| Jumbo | 5% | 720 | 43% |

| Fannie Mae HomeReady | 3% | 620 | 43% |

| Freddie Mac Home Possible | 3% | 660 | 45% |

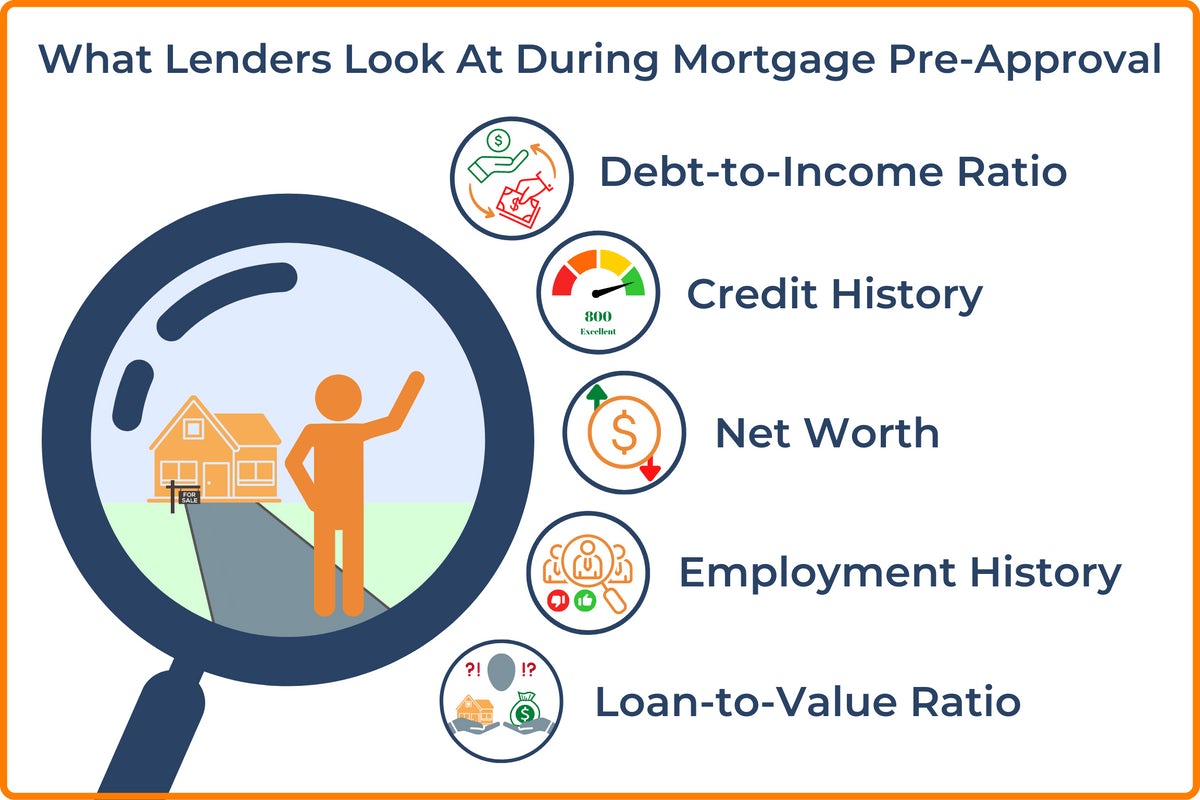

Even though the lenders may provide different rates to the same borrower, they usually take into consideration similar metrics to conduct the analysis. Using these metrics, a lender assesses the risk level of a borrower and issues the pre-approval letter with the details based on the lender’s analysis. It is important to understand what each metric means for a borrower to prepare for a pre-approval process and utilize their financial situation to their advantage.

- Debt-to-Income (DTI) Ratio: The DTI ratio looks at a borrower’s monthly debt expenses as a percentage of their gross monthly income. A DTI ratio of less than 43% is required for a majority of mortgage programs, which means less than 43% of a borrower’s monthly income should be going towards debt repayments. A lower DTI ratio will result in a higher pre-approved amount.

- Loan-to-Value (LTV) Ratio: The LTV ratio is calculated by dividing the mortgage amount by the home value. The higher the down payment, the lower the LTV ratio. An LTV ratio of less than 80% can help a borrower avoid private mortgage insurance (PMI).

- Credit History: Even though lenders look at a credit score, they are more interested in the credit history of a person because it can provide more detailed information regarding the borrower's credit worthiness. A minimum credit score of 620 is required by most lenders, however, certain loans, such as an FHA loan, only require a credit score of 500. A borrower might also be eligible for USDA loans or VA loans with a lower credit score. Once the borrower passes the credit score threshold, the lender will analyze their credit history and use their metrics to adjust the interest rate and mortgage amount offered.

- Income and Employment History: Being employed with a steady income can greatly improve a borrower's chances of getting pre-approved. Lenders will look at a borrower’s employment history along with their current income.

- Assets and Liabilities: The lender also has to ensure that the borrower has enough money to use as a down payment. If the borrower does not have any assets or they have an excessive amount of liabilities, the lender may not be willing to pre-approve them even if the borrower meets every other criterion.

| Monthly Mortgage Payments Based on Credit Score | ||||||

|---|---|---|---|---|---|---|

| Credit Score | 760-850 | 700-759 | 680-699 | 660-679 | 640-659 | 620-639 |

| Approximate APR | 4.93% | 5.15% | 5.33% | 5.54% | 5.97% | 6.52% |

| Principal Amount | Monthly Mortgage Payment | |||||

| $250,000 | $1,331.07 | $1,365.07 | $1,392.46 | $1,425.91 | $1,494.22 | $1,582.97 |

| $350,000 | $1,863.50 | $1,911.09 | $1,949.44 | $1,996.27 | $2,091.91 | $2,216.15 |

| $500,000 | $2,662.15 | $2,730.13 | $2,784.91 | $2,851.82 | $2,988.44 | $3,165.93 |

| $600,000 | $3,194.58 | $3,276.16 | $3,341.90 | $3,422.18 | $3,586.12 | $3,799.12 |

*The values are approximate and may differ from the actual monthly mortgage payments offered by a lender.

When the lender collects all the documents needed to conduct the analysis, they have 3 business days to provide a loan estimate. This loan estimate is usually a 3-page document that outlines whether the borrower has been pre-approved or not. If they have been pre-approved, it also provides an estimated loan amount and an interest rate on loan.

Pre-Approval vs. Pre-Qualification

Mortgage pre-qualification and pre-approval both aim to give you an idea about how much you can afford and the terms of the mortgage. However, the slight difference between the two is the depth and the amount of information the lender requires from you.

Pre-Qualification: In a mortgage pre-qualification, the lender will only need very basic information to give you an estimate of how much you can afford. You won’t need to provide any documents, and you’ll only give basic numbers, such as your credit score, the price range of homes you are looking to buy, the amount of down payment you have saved, your monthly debt, and the type of loan you are looking to take (fixed, variable).

Pre-Approval: In a mortgage pre-approval, you will need to provide all the required financial documents and information. You will need to also present supporting bank statements, tax returns, and pay stubs, along with all the information required in a pre-qualification. The lender will also run a credit check, and upon pre-approval, provide you with an offer in writing with a mortgage rate.

| Pre-Approval vs. Pre-Qualification | ||

|---|---|---|

| Pre-Approval | Pre-Qualification | |

| Documents Needed? | ✅ | ❌ |

| Information Verified? | ✅ | ❌ |

| Hard Credit Check? | ✅ | ❌ |

| Specific Loan Limit? | ✅ | ❌ |

| Specific Interest Rate? | ✅ | ❌ |

Getting Approved for a Mortgage

Once a borrower firms the deal with a seller, they can start applying for a mortgage. Even though a lender may have pre-approved a borrower for a mortgage, it does not mean that the borrower is automatically approved for the mortgage. The borrower will have to contact the lender again and apply for a mortgage referencing the pre-approval letter. The lender needs to ensure that all the conditions of the pre-approval are met before originating the loan. This requires the lender to inspect the home's condition, appraised value, and title of the property, along with other factors considered during a mortgage pre-approval, such as the borrower’s income, credit history, and current debt obligations.

- Home Appraisal: The lender will want to get an appraisal done to ensure that the appraised value is equal to or more than the listing price. This will show you that you are not paying more for the home as compared to its appraised value. Having a purchase price more than the appraised value may cause issues as lenders will not want to lend out more than the home is worth. That’s why contingencies can be used when making an offer on a home, such as an appraisal contingency, to allow you to renegotiate or back out of the deal.

- Title: The lender will also have to check with the title company to make sure that it is a clear title and that there is no dispute regarding ownership. Lenders can require you to purchase title insurance to protect against issues with the title.

- Home Condition: Certain mortgage loans require that the home meet property standards. For example, the Department of Housing and Urban Development (HUD) has Minimum Property Requirements (MPR) and Minimum Property Standards (MPS) that are required for all FHA loans. According to HUD, these requirements and standards on the home’s condition ensure that the home is "safe, sound, and secure".

Mortgage Pre-Approval for Largest US Lenders

You can apply for a mortgage pre-approval online in minutes, or you can apply for a mortgage pre-approval over the phone or in person. Different lenders have different pre-approval processes. Here’s how to get a mortgage pre-approval at some of the largest mortgage lenders in the United States.

Bank of America Mortgage Pre-Approval

Bank of America allows you to prequalify for a mortgage through their Digital Mortgage Experience. You'll need to provide information about your income and bank accounts, and also provide your Social Security number for a credit check.

You won’t be able to get a mortgage pre-approval with Bank of America online. That's because you will be required to submit documents such as your pay stubs, W-2 forms, and tax returns. You'll get the results of a prequalification in as little as one hour, while a pre-approval with Bank of America can take 10 business days or more.

Wells Fargo Mortgage Pre-Approval

You can’t get a pre-approval online with Wells Fargo, but you can get prequalified instantly. To get prequalified with Wells Fargo, you won't need to submit any personal information. No credit check is required either. Instead, you'll enter the price of the home, the down payment you are planning to make, the property location, your income, your monthly debt, and your estimated credit score range.

If you're pre-qualified, you'll be able to know how much you can qualify for, based on your down payment and home sales price, along with your estimated monthly mortgage payment and cash required at closing.

Navy Federal Mortgage Pre-Approval

Navy Federal lets you apply for a mortgage pre-approval online. You may get instantly pre-approved with Navy Federal, or it may take longer based on your application. Navy Federal pre-approvals are valid for up to 90 days. Your information will still need to be verified even after you have been pre-approved, which will require you to submit documents such as your tax returns, pay stubs, W-2 forms, and bank account information.

Chase Mortgage Pre-Approval

Chase lets you get prequalified for a mortgage online. You'll be able to receive a quoted interest rate based on your credit score and LTV. Other factors that Chase considers is your employment history, income, assets, and the property being financed. Chase requires you to submit your Social Security number in order to get prequalified for a mortgage.

Frequently Asked Questions

How Long Does Mortgage Pre-Approval Take?

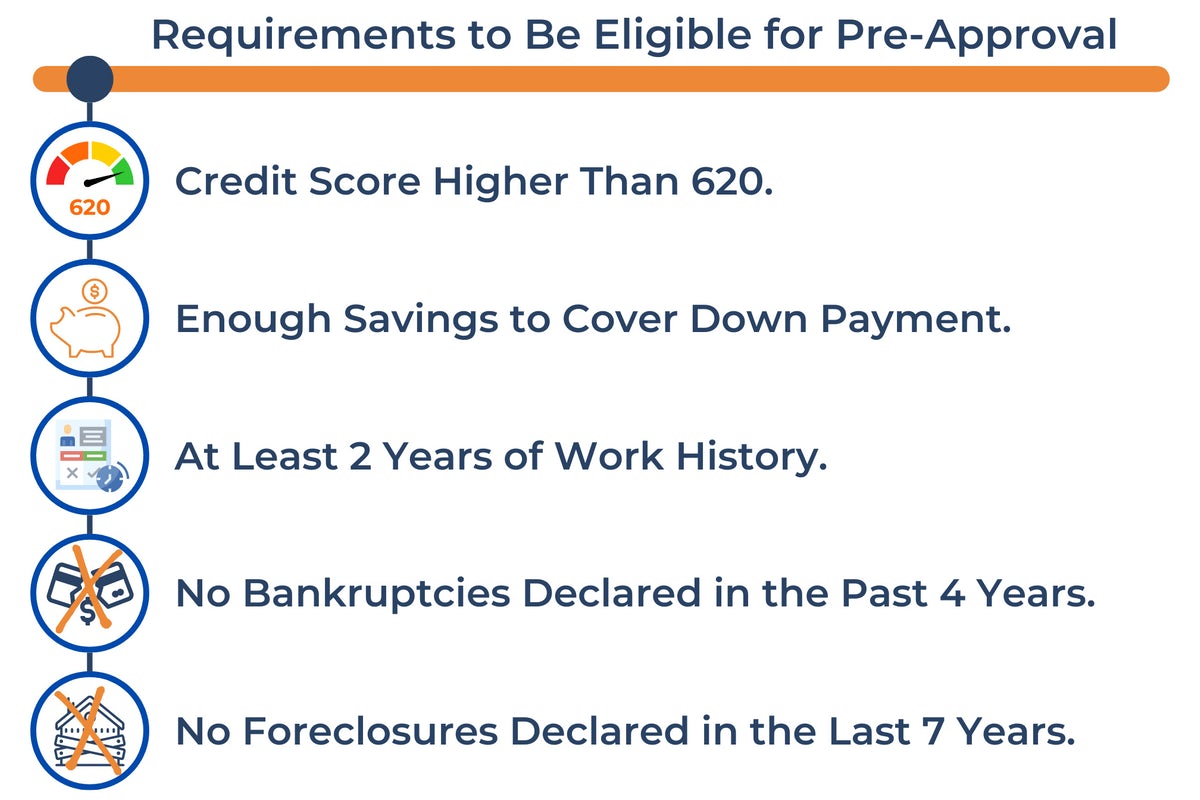

The mortgage pre-approval application itself will only take a few minutes. You will usually get a mortgage pre-approval decision within three business days, with some lenders offering same-day mortgage pre-approvals. However, if you have a lot of debt, have been bankrupt in the past, have had your home foreclosed, or have a bad credit score, then it can slow down the pre-approval process. If your finances are complex, then it might take over a month to get a pre-approval decision. You might also be asked to complete a declaration with the following questions:

- Are there any outstanding judgments against you?

- Have you been declared bankrupt within the past 4 years?

- Have you had property foreclosed upon or given title or deed in lieu thereof in the last 7 years?

- Are you a party to a lawsuit? Have you directly or indirectly been obligated on any loan which resulted in foreclosure, transfer of title in lieu of foreclosure, or judgment?

- Are you presently delinquent or in default on any Federal debt or any other loan, mortgage, financial obligation, bond, or loan guarantee?

- Are you obligated to pay alimony, child support, or separate maintenance?

- Is any part of the down payment borrowed?

- Are you a co-maker or endorser on a note?

Answering yes to any of the questions stated above may delay your mortgage pre-approval as further processing might be needed.

What Documents Are Required For Pre-Approval?

The pre-approval process is similar to a mortgage application where the lender does a deep dive into your finances and ability to repay a mortgage loan. When applying for a mortgage pre-approval, you will need to submit various documents to confirm your identity and prove your income and assets.

It is important to ensure that your stated earnings are truthful and are large enough for your DTI to stay within the limit for a chosen loan. The following documents are required from you when applying for a mortgage pre-approval:

Identification

- Drivers License or Passport

- Social Security Number (SSN)

Income

- Last Two Pay Stubs

- W-2 Forms

- Income Tax Returns

Assets

- Bank Statements

- Investment Account, 401(K), And/Or IRA Statements

Do I Have To Provide My Social Security Number For A Mortgage Pre-Approval?

Yes, you will need to provide your Social Security number (SSN) even when you are applying for just a mortgage pre-approval. That’s because your mortgage lender will need to check your credit report and credit history.

What Is a Pre-Approval Letter?

When the lender has gone through all your information and reaches an estimate, they send you a pre-approval letter showing that they have verified your financials. This is important because:

- Real estate agents want to see the pre-approval confirmation before they start showing you homes in order to narrow their search.

- Home sellers will have more confidence in your ability to purchase the home when an offer is made.

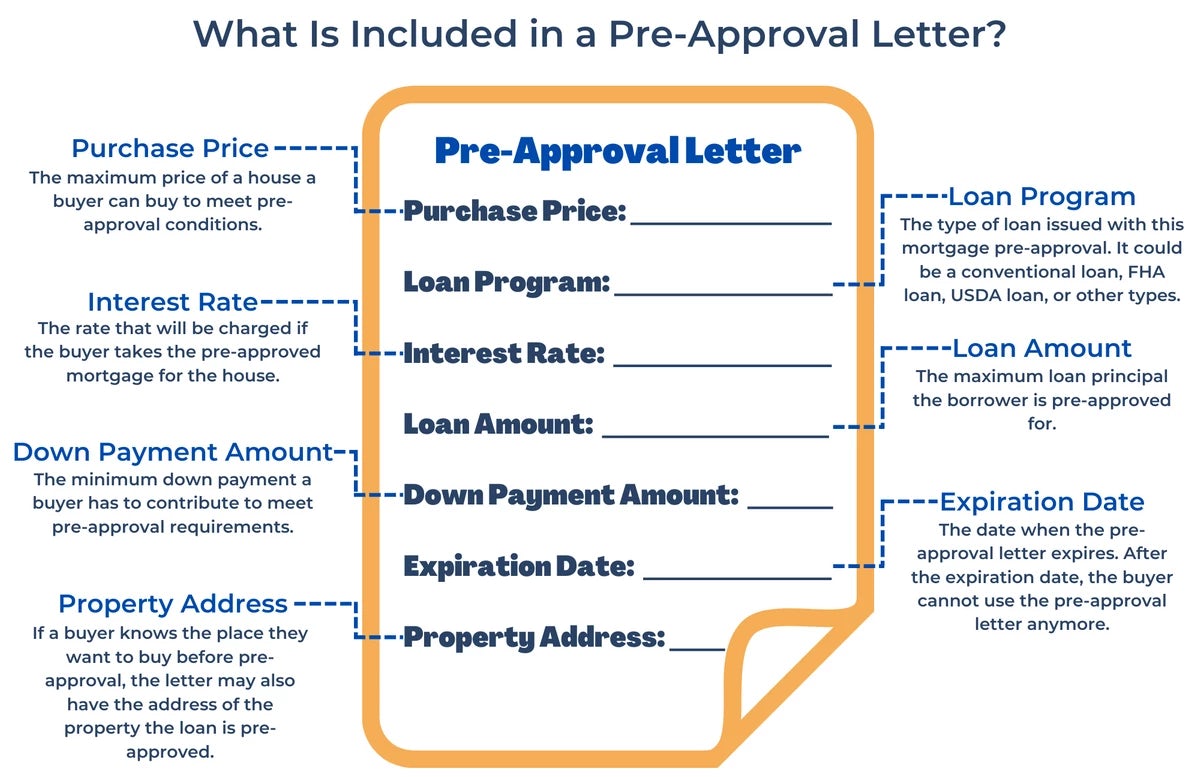

A mortgage pre-approval letter will include:

- Your pre-approved loan amount

- Your mortgage interest rate

- Your mortgage loan term

- Your loan type

- Your loan LTV

- Pre-approval expiration date

- Conditions to credit approval

How Long Does a Mortgage Pre-Approval Last?

Mortgage pre-approvals typically last for 60 to 90 days. The exact length that a mortgage pre-approval is valid for will depend on your lender. With some lenders, a pre-approval might only be valid for 30 days, while some lenders may offer pre-approvals valid for 90 days at a time. Your mortgage pre-approval letter will have an expiration date that tells you how long your pre-approval is valid.

Mortgage pre-approvals have an expiry date since the pre-approval was based on your financial situation at a particular point in time. Your employment situation might have changed and your credit score might have dropped since your pre-approval. The more time that has passed since your lender checked your application, the higher the chance that a negative change has occurred. To prevent outdated information, mortgage pre-approvals expire and will need to be renewed if it is still needed. For example, if you weren’t able to find a home in the time that your mortgage pre-approval was valid, then you can have your pre-approval renewed. Your lender may check your credit again and ask you for updated documents, such as more recent payslips.

Do Mortgage Pre-Approvals Hurt Credit Scores?

When you apply for a mortgage pre-approval, the lender will check your credit report. This credit check is a hard inquiry, also known as a hard pull, and has a negative effect on your credit score. There’s no fixed amount that a hard inquiry will lower your credit score by, but it is usually less than a 10-point drop for a single hard inquiry.

Having multiple hard inquiries can cause your credit score to drop significantly. The good news with mortgages and credit checks is that if the credit checks are all completed within a certain period, usually 45 days, then they all count as only one hard inquiry, rather than multiple hard inquiries. This 45-day period starts on the date of your first credit check and ends after 45 days. All credit checks within this period will count as one inquiry. However, only credit checks by mortgage lenders and mortgage brokers count toward this single inquiry rule. If you apply for other credit products during this time, such as multiple credit cards, then those credit checks will still show up as multiple inquiries.

When Should You Get Pre-Approved?

You should get pre-approved as soon as you have decided that you want to purchase a home and are going to begin your home search. While you aren’t required to get a mortgage pre-approval to start looking for homes, it’s a good idea to have a mortgage pre-approval letter ready. If a home seller requires pre-approval, you will be able to show that you have been pre-approved rather than having to wait possibly days for a new mortgage pre-approval. Having a mortgage pre-approval also makes your purchase offer more attractive.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.