Conforming Loan Limits 2023

What You Should Know

- A conforming loan “conforms” to the requirements and guidelines set by Fannie Mae and Freddie Mac.

- Conforming loans generally have lower mortgage rates compared to non-conforming loan rates since they can be insured by Fannie Mae and Freddie Mac.

- 2023 conforming loan limits range from $726,200 in low-cost areas to $1,089,300 in high-cost areas for a one-unit property.

- The conforming loan limit (CLL) is set each year and will increase or decrease based on changes in the average US. home value over the past year.

- Government-backed loans, such as FHA loans, VA loans, and USDA loans, are not considered to be conforming loans.

What is a Conforming Loan?

A conforming loan starts as a conventional home loan, which is a loan that is under the limit set by the Federal Housing Finance Agency (FHFA). It is a type of conventional loan. A conforming loan means that your mortgage is purchased by one of two FHFA-regulated agencies, Fannie Mae or Freddie Mac. If your home loan amount is over FHFA’s conforming loan limits, your mortgage is considered a jumbo loan and cannot be purchased by these agencies. Conforming loans offer lower mortgage rates compared to jumbo loans. Additionally, conforming loans are considered qualified mortgages. When lending out qualified mortgages, the lender is obligated to make sure that the borrower has the ability to repay the loan. This is called the Ability-to-Repay/Qualified Mortgage Rule by the Consumer Financial Protection Bureau.

When you get a home loan from a mortgage lender, such as a bank or credit union, the lender is originating a home loan. If they service your loan, you make your monthly mortgage payments to them, but they could sell your underlying mortgage to another financial institution at the same time. If your mortgage is sold to a third party, the lien on your property is held by that third party. You will still make mortgage payments to the same lender because they are responsible for servicing the loan, but the party that owns the mortgage will change.

A lender might sell home loans to liquidate your mortgage into money that can be used to finance other home purchases. This allows the lender to originate and service home loans without needing the financial capital to support all home purchases simultaneously. Conforming loans are usually offered on a federal level and can be easily obtained through local lenders. There are other programs available, such as first time home buyer programs, that can provide additional financing to eligible people.

Conforming Loan Limits 2023 by County

How Do Conforming Loans Work?

APPLY FOR A MORTGAGE WITH A CONVENTIONAL LENDER THAT MEETS FHFA GUIDELINES

➔

LENDER SELLS YOUR MORTGAGE TO FANNIE MAE OR FREDDIE MAC

➔

GOVERNMENT-SPONSORED AGENCY INSURES YOUR MORTGAGE WITH LOWER MORTGAGE RATES

➔

MAKE MONTHLY MORTGAGE PAYMENTS TO YOUR ORIGINAL LENDER

Fannie Mae and Freddie Mac are government-sponsored enterprises (GSEs) that purchase home loans behind-the-scenes. This means that you won’t need to specifically apply for a conforming loan. If your mortgage application meets the requirements to be considered a conforming loan, your lender has the option to sell the mortgage to Fannie Mae or Freddie Mac. In turn, your lender may offer you a lower mortgage rate. Not all conforming loans that meet the requirements are sold to or backed by Fannie Mae or Freddie Mac. Even if your conforming loan is sold to a GSE, nothing changes on your part. You will still make monthly mortgage payments to your original lender or to your mortgage loan servicer. What changes behind-the-scenes is that Fannie Mae or Freddie Mac will now own the mortgage.

The FHFA regulates Fannie Mae and Freddie Mac by only allowing them to purchase mortgages that meet certain requirements. For example, the maximum loan limit also known as the conforming loan limit (CLL), puts a limit on how much lenders can loan out per home buyer. By purchasing mortgages and taking on the full risk associated with the loan lent out, Fannie Mae and Freddie Mac require mortgage lenders to follow certain guidelines to help ensure that they are not originating risky loans.

2023 Conforming Loan Limits

FHFA’s conforming loan limits are set annually in November, with the new limits taking effect on January 1st of each year. The limits are based on the geographical location (county) of your property, with annual changes based on changes in the national average home price measured using the FHFA House Price Index. There is also a baseline loan limit that acts as a baseline loan limit.

95% of counties have a maximum home loan limit that is at the baseline loan limit. A few counties have high-cost area loan limits, which allows the conforming loan limit in those counties to be 115% of the highest median home price in the area or up to 150% of the baseline loan limit. This accounts for higher housing prices in those counties. Alaska, Hawaii, Guam, and the U.S. Virgin Islands are also all considered to be high-cost areas.

2023 Conforming Loan Limits Chart

| Property Size | Low-Cost Area “Floor” | High-Cost Area “Ceiling” | Alaska, Hawaii, Guam, and U.S. Virgin Islands |

|---|---|---|---|

| One-Unit | $472,030 | $1,089,300 | $1,633,950 |

| Two-Units | $604,400 | $1,394,775 | $2,092,150 |

| Three-Units | $730,525 | $1,685,850 | $2,528,775 |

| Four-Units | $907,900 | $2,095,200 | $3,142,800 |

The most common conforming loan limit of $726,200 for 2023 is a 12% increase from 2022, and it reflects the increase in American home prices. This is reflected in the FHFA House Price Index (HPI) increasing by 17.4% from October 2020 to October 2021. In comparison, the housing inflation rate over the same period was only 4.52% based on the Consumer Price Index (CPI) for housing. 95% of counties have the baseline loan limit and 3% of counties are considered high-cost areas. 2% of counties have county loan limits that range between the baseline loan limit and the maximum high-cost loan limit, based on the individual county’s median home price.

Historical Conforming Loan Limits

| Year | Baseline One-Unit Loan Limit | High-Cost Area Loan Limit | Annual Change (%) |

|---|---|---|---|

| 2023 | $726,200 | $1,089,300 | +12.2% |

| 2022 | $647,200 | $970,800 | +18.0% |

| 2021 | $548,250 | $822,375 | +7.4% |

| 2020 | $510,400 | $765,600 | +5.4% |

| 2019 | $484,350 | $726,525 | +6.9% |

| 2018 | $453,100 | $679,650 | +6.8% |

| 2017 | $424,100 | $636,150 | +1.7% |

| 2016 | $417,000 | $625,500 | - |

| 2015 | $417,000 | $625,500 | - |

| 2014 | $417,000 | $625,500 | - |

| 2013 | $417,000 | $625,500 | - |

| 2012 | $417,000 | $625,500 | - |

| 2011 | $417,000 | $625,500 | - |

2023 Conforming Loan Limits Search

| County | State | One-Unit Limit | Two-Unit Limit | Three-Unit Limit | Four-Unit Limit |

|---|---|---|---|---|---|

| AUTAUGA COUNTY | AL | $726,200 | $929,850 | $1,123,900 | $1,396,800 |

| BALDWIN COUNTY | AL | $726,200 | $929,850 | $1,123,900 | $1,396,800 |

| BARBOUR COUNTY | AL | $726,200 | $929,850 | $1,123,900 | $1,396,800 |

| BIBB COUNTY | AL | $726,200 | $929,850 | $1,123,900 | $1,396,800 |

| BLOUNT COUNTY | AL | $726,200 | $929,850 | $1,123,900 | $1,396,800 |

| BULLOCK COUNTY | AL | $726,200 | $929,850 | $1,123,900 | $1,396,800 |

| BUTLER COUNTY | AL | $726,200 | $929,850 | $1,123,900 | $1,396,800 |

| CALHOUN COUNTY | AL | $726,200 | $929,850 | $1,123,900 | $1,396,800 |

| CHAMBERS COUNTY | AL | $726,200 | $929,850 | $1,123,900 | $1,396,800 |

| CHEROKEE COUNTY | AL | $726,200 | $929,850 | $1,123,900 | $1,396,800 |

High-Cost Areas Conforming Loan Limits

Counties with a conforming loan limit of $1,089,300 in 2023:

- Alaska (All Counties)

- ALEUTIANS EAST BOROUGH

- ALEUTIANS WEST CENSUS AREA

- ANCHORAGE MUNICIPALITY

- BETHEL CENSUS AREA

- BRISTOL BAY BOROUGH

- DENALI BOROUGH

- DILLINGHAM CENSUS AREA

- FAIRBANKS NORTH STAR BOROUGH

- HAINES BOROUGH

- HOONAH-ANGOON CENSUS AREA

- JUNEAU CITY AND BOROUGH

- KENAI PENINSULA BOROUGH

- KETCHIKAN GATEWAY BOROUGH

- KODIAK ISLAND BOROUGH

- KUSILVAK CENSUS AREA

- LAKE AND PENINSULA BOROUGH

- MATANUSKA-SUSITNA BOROUGH

- NOME CENSUS AREA

- NORTH SLOPE BOROUGH

- NORTHWEST ARCTIC BOROUGH

- PETERSBURG CENSUS AREA

- PRINCE OF WALES-HYDER CENSUS AREA

- SITKA CITY AND BOROUGH

- SKAGWAY MUNICIPALITY

- SOUTHEAST FAIRBANKS CENSUS AREA

- VALDEZ-CORDOVA CENSUS AREA

- WRANGELL CITY AND BOROUGH

- YAKUTAT CITY AND BOROUGH

- YUKON-KOYUKUK CENSUS AREA California:

- ALAMEDA COUNTY

- CONTRA COSTA COUNTY

- LOS ANGELES COUNTY

- MARIN COUNTY

- ORANGE COUNTY

- SAN BENITO COUNTY

- SAN FRANCISCO COUNTY

- SAN MATEO COUNTY

- SANTA CLARA COUNTY

- SANTA CRUZ COUNTY District of Columbia:

- DISTRICT OF COLUMBIA Hawaii (All Counties)

- HAWAII COUNTY

- HONOLULU COUNTY

- KALAWAO COUNTY

- KAUAI COUNTY

- MAUI COUNTY Idaho:

- TETON COUNTY Maryland:

- CALVERT COUNTY

- CHARLES COUNTY

- FREDERICK COUNTY

- MONTGOMERY COUNTY

- PRINCE GEORGE'S COUNTY Massachusetts:

- DUKES COUNTY

- NANTUCKET COUNTY New Jersey:

- BERGEN COUNTY

- ESSEX COUNTY

- HUDSON COUNTY

- HUNTERDON COUNTY

- MIDDLESEX COUNTY

- MONMOUTH COUNTY

- MORRIS COUNTY

- OCEAN COUNTY

- PASSAIC COUNTY

- SOMERSET COUNTY

- SUSSEX COUNTY

- UNION COUNTY New York:

- BRONX COUNTY

- KINGS COUNTY

- NASSAU COUNTY

- NEW YORK COUNTY

- PUTNAM COUNTY

- QUEENS COUNTY

- RICHMOND COUNTY

- ROCKLAND COUNTY

- SUFFOLK COUNTY

- WESTCHESTER COUNTY Pennsylvania:

- PIKE COUNTY Utah:

- SUMMIT COUNTY

- WASATCH COUNTY Virginia:

- ARLINGTON COUNTY

- CLARKE COUNTY

- CULPEPER COUNTY

- FAIRFAX COUNTY

- FAUQUIER COUNTY

- LOUDOUN COUNTY

- MADISON COUNTY

- PRINCE WILLIAM COUNTY

- RAPPAHANNOCK COUNTY

- SPOTSYLVANIA COUNTY

- STAFFORD COUNTY

- WARREN COUNTY

- ALEXANDRIA CITY

- FAIRFAX CITY

- FALLS CHURCH CITY

- FREDERICKSBURG CITY

- MANASSAS CITY

- MANASSAS PARK CITY West Virginia:

- JEFFERSON COUNTY Wyoming:

- TETON COUNTY Guam

- ST. CROIX ISLAND

- ST. JOHN ISLAND

- ST. THOMAS ISLAND

U.S. Virgin Islands:

For high-cost areas, the conforming loan limit will range from the baseline of $726,200 to the maximum of $1,089,300. Not all high-cost areas will be at the maximum end of this range. The limit for your county will only be $1,089,300 if median home prices in your area are high enough to reach this limit.

Of the 3,000 counties in the United States, the FHFA classifies around 130 to 200 counties as high-cost areas. High-cost areas are not determined by looking at home prices only within the county. Instead, the FHFA groups counties into core-based statistical areas (CBSAs) and then looks at the median home values for these groups of counties. The highest median home value in each CBSA is considered, with the conforming loan limit only being higher than the baseline CLL if the highest median home value for the CBSA is greater than 115% of the baseline.

For example, the Nashville Metropolitan Area is within the Nashville-Davidson-Murfreesboro-Franklin core-based statistical area, which includes 13 counties. Since at least one county has a median home price that is greater than the 2023 baseline loan limit of $726,200, all counties within the Nashville CBSA will have a higher conforming loan limit. For 2023, the conforming loan limit for those 13 counties is $890,100.

The 2023 conforming loan for high-cost areas cannot exceed the limit of $1,089,300. For example, the median home price in Los Angeles is approaching $1 million but the maximum amount that a conforming loan can be in Los Angeles is still $1,089,300. One way to get around the conforming loan limit is to get a second mortgage loan, such as with a piggyback loan, or make a larger down payment. For example, for a $1.5 million home in Los Angeles County, California, you can get a conforming loan for $1,089,300 and get a second loan for the remaining amount. Or, you can make a down payment for the entire remaining amount. This allows you to qualify for low conforming loan rates for homes that are over the conforming loan limits. Otherwise, you will need to get a jumbo loan instead, which has stricter requirements and a higher interest rate.

Conforming Loan Other Requirements

The most well-known conforming loan requirement is the maximum mortgage limit set by the FHFA each year. While this is the most restrictive requirement to getting a conforming loan, Fannie Mae and Freddie Mac also outline other requirements on loans. A good way to see if you can qualify for a conforming loan is to get a mortgage pre-approval letter from your lender for a conforming loan. Typically, your lender will check these requirements for a conventional loan as well, but it is a good idea to make sure you qualify beforehand.

- Loan-to-Value (LTV) Ratio: Your mortgage can finance up to a maximum of 97% of your total home sale price. This means that you must contribute at least a 3% down payment toward the purchase of your property.

- Maximum Income: Fannie Mae’s HomeReady Mortgage and Freddie Mac’s HomePossible Mortgage programs target low-income home buyers. Consequently, to qualify for these mortgage programs, there is an income limit equal to 80% of your county’s median income.

- Debt-to-Income (DTI) Ratio: To ensure your income can support monthly mortgage payments, you can use a maximum of 45% of your income to finance debt including the new mortgage. This means you have to add your monthly mortgage payments from the potential mortgage and monthly payments for any outstanding debt together, which is then compared to your gross monthly income. In some cases, the maximum allowed DTI ratio can be as high as 50%. For other cases, such as those with a lower credit score or a lower down payment, the maximum allowed DTI ratio might be as low as 36%.

- Minimum Credit Score: Generally, home buyers are required to have a credit score of at least 620. If your credit score is above 680, you should be eligible for discounted mortgage rates. If your credit is below 620, you may not qualify for a conforming loan, but there are still ways to buy a house with a bad credit score.

- Homebuyer Education: You must take either Fannie Mae or Freddie Mac’s homeownership education course or homebuyer education course respectively if all borrowers attached to the mortgage are first-time home buyers.

While Fannie Mae and Freddie Mac set these guidelines, individual lenders can set different requirements for conforming loans and could charge different interest rates. The requirements listed are the bare minimum requirements for a loan to be purchased by Fannie Mae or Freddie Mac but lenders have their requirements that more closely match their risk tolerance.

Additional Debt-to-Income Ratio Requirements

The maximum DTI ratio allowed by Fannie Mae depends on your down payment/LTV ratio and your credit score. For example, if your credit score is 680 and you make a down payment that is less than 25%, the maximum allowed DTI ratio is 36%. However, if your credit score is at least 720 and you make a down payment that is less than 25%, the maximum allowed DTI ratio is 45%. A DTI ratio of up to 50% is only allowed if your application is processed through Fannie Mae’s automated underwriting system, called the Desktop Underwriter. The table below shows a sample of an eligibility matrix from Fannie Mae's Selling Guide.

Conforming Loans DTI Ratio Requirements

| Minimum Credit Score | Down Payment | |

|---|---|---|

| Maximum 36% DTI Ratio | 680 | Less than 25% |

| 640 | 25% or more | |

| Maximum 45% DTI Ratio | 720 | Less than 25% |

| 680 | 25% or more |

Pros and Cons of Getting a Conforming Loan

Pros

- Easier to Qualify: Conforming loans are generally easier to qualify for than other types of loans. Since lenders bear less risk with conforming loans because they can sell them, they only need to adhere to standards set by the FHFA. If a lender has to use their own money to lend you money like with a jumbo loan, their requirements will be stricter.

- Low Minimum Down Payment: With a minimum down payment of as low as 3%, these loans are very accessible to home buyers with low savings. However, if you choose to make a larger down payment, you can reduce your monthly mortgage payments, mortgage rates, and mortgage insurance. Generally, you should put as much down on a mortgage as you can comfortably afford.

- Low Mortgage Rates: Lenders prefer conforming loans because they can sell them on the secondary market, so they will usually charge lower mortgage rates to borrowers. However, some government mortgages have lower mortgage rates like VA loans or FHA loans, which have some of the lowest mortgage rates out there.

- Easily Accessible: Nearly all mortgage lenders offer conforming loans.

Cons

- Other Government Loans: Some types of government-backed loans are easier to qualify for and could offer some better benefits or rates. You should treat conforming loans as one of many options for getting a mortgage.

- Conforming Loan Limit: Within each county, there is a maximum loan amount lenders can give you before your mortgage turns into a Jumbo Loan.

- Insurance: If your down payment is for less than 20% of the total home price, you will have to pay for Private Mortgage Insurance (PMI). Depending on the type of PMI you can get, once you own 22% equity in your home, which means you’ve paid back 22% of your principal mortgage amount, your lender should stop charging you mortgage insurance. Some mortgages like VA loans require no mortgage insurance regardless of the down payment.

Conforming Loan Interest Rates

While we try our best to get your the best rates, we cannot guarantee that they are always accurate. Casaplorer® assumes no liability for the accuracy of the information presented, and will not be held responsible for any damages resulting from its use. Rates shown are for informational purposes only. Estimated payments do not include taxes and insurance. Some state and county maximum loan amount restrictions may apply. Casaplorer® is not endorsed or sponsored by any mortgage lender or government agency. Please refer to https://www.fanniemae.com/ or http://www.freddiemac.com/.

Fannie Mae vs. Freddie Mac 30-Year Fixed Mortgage Rates

The secondary market for conforming loans is large, which means when you get a mortgage with a lender, they can easily sell it to Fannie Mae or Freddie Mac. This reduces their risk if you fall behind on your payments or default on your mortgage, which means your lender offers lower mortgage rates to encourage home buyers to stay within FHFA limits. Lowest mortgage rates set by Fannie Mae and Freddie Mac are reported on their website, but it is likely that the interest rate you receive will be higher than the one reported. It is because of loan-level pricing adjustments, which is a risk-based fee that is charged by Freddie Mac and Fannie Mae. As a rule of thumb, the riskier the borrower, the higher the loan-level pricing adjustment. It is important to note that a borrower can still default on their loan even if it is backed by an agency. If a borrower misses a certain number of payments on their mortgage, the property may move into the pre-foreclosure stage where a borrower may be forced to sell the property.

Mortgage rates shown from Fannie Mae and Freddie Mac are as reported by the respective agencies and not representative of mortgage rates you would receive on a Fannie Mae or Freddie Mac loan. The mortgage rate you receive is determined by your lender.

Can conforming loan limits decrease?

According to the FHFA, conforming loan limits cannot decrease - limits can only increase or stay the same. CLLs will only change if the underlying FHFA house price index increases over the conforming loan limit’s high-water mark. For example, some areas have had their CLL stay the same between 2007 and 2016 even though housing prices decreased in 2007 due to the housing crisis. After the price index increased above 2007 levels in 2017, the conforming loan limit increased once again in 2017.

If a county were to fall from a high-cost area designation to a baseline value area, their conforming loan limit will also not decrease to the baseline value.

Non-Conforming Loan Limits

If the amount of your home loan is over the conforming loan limits, your loan is considered a jumbo loan. Jumbo loans cannot be purchased by Fannie Mae or Freddie Mac, so they will be held by a private mortgage lender . To compensate for the added risk, your mortgage lender may require a higher down payment or a higher mortgage rate.

The conforming loan limits apply only to the loan amount, not the price of the home that you are getting a loan for. If the conforming loan limit for your area is $822,375 but you are looking to purchase a $1 million home, you may still be able to get a conforming loan. You will need to make a down payment that reduces your home loan amount to less than $822,375. In this case, your down payment must be at least $177,625 (about 18%), otherwise, it is classified as a jumbo loan.

VA Home Loan Limits

VA loans use the same limits as the FHFA’s conforming loan limits. The VA loan limit does not apply to you if you are eligible for a VA loan with full entitlement. This applies to you if you fulfill both of the following conditions:

- You are a veteran or active servicemember

- You have never held a VA loan before or you sold the property attached to your previous VA loan

Those with full entitlement can get any loan amount with no limit, so long as your credit history, income, and assets allow your lender to approve your VA loan. You can purchase a home at any home price anywhere in the country with no down payment required.

If you have partial entitlement or no entitlement, your VA home loan limit is your county’s FHFA conforming loan limit. You will have partial entitlement if:

- You currently have a VA loan

- You have defaulted on a VA loan in the past

- You refinanced your VA loan into a non-VA loan

FHA Loan Limits

Conforming limits are related to conventional mortgages, to compare conventional and FHA loans in this regard, we should note that FHA loans do not follow FHFA’s conforming loan limits. Although, FHA loan limits do use the same median home price values. FHA loan limits use the median home price for the area, ranging from 65% for low-cost to 150% for high-cost areas. Since FHA’s high-cost areas are 150% of the baseline, this makes the maximum FHA loan limit the same as FHFA’s maximum limit for conforming loans. FHA’s high-cost area 2022 loan limit was $970,800. This was increased to $1,089,300 in 2023.

USDA Loan Limits

USDA loans do not have explicit home loan limits. Instead, USDA loans are restricted to home buyers with household incomes of less than 115% of your county’s median household income. This restricts the maximum mortgage loan that you can support with monthly payments. Since USDA loans are targeted toward low to moderate-income earners, maximum loan limits are unnecessary. You can verify your USDA eligibility with our USDA Eligibility Calculator.

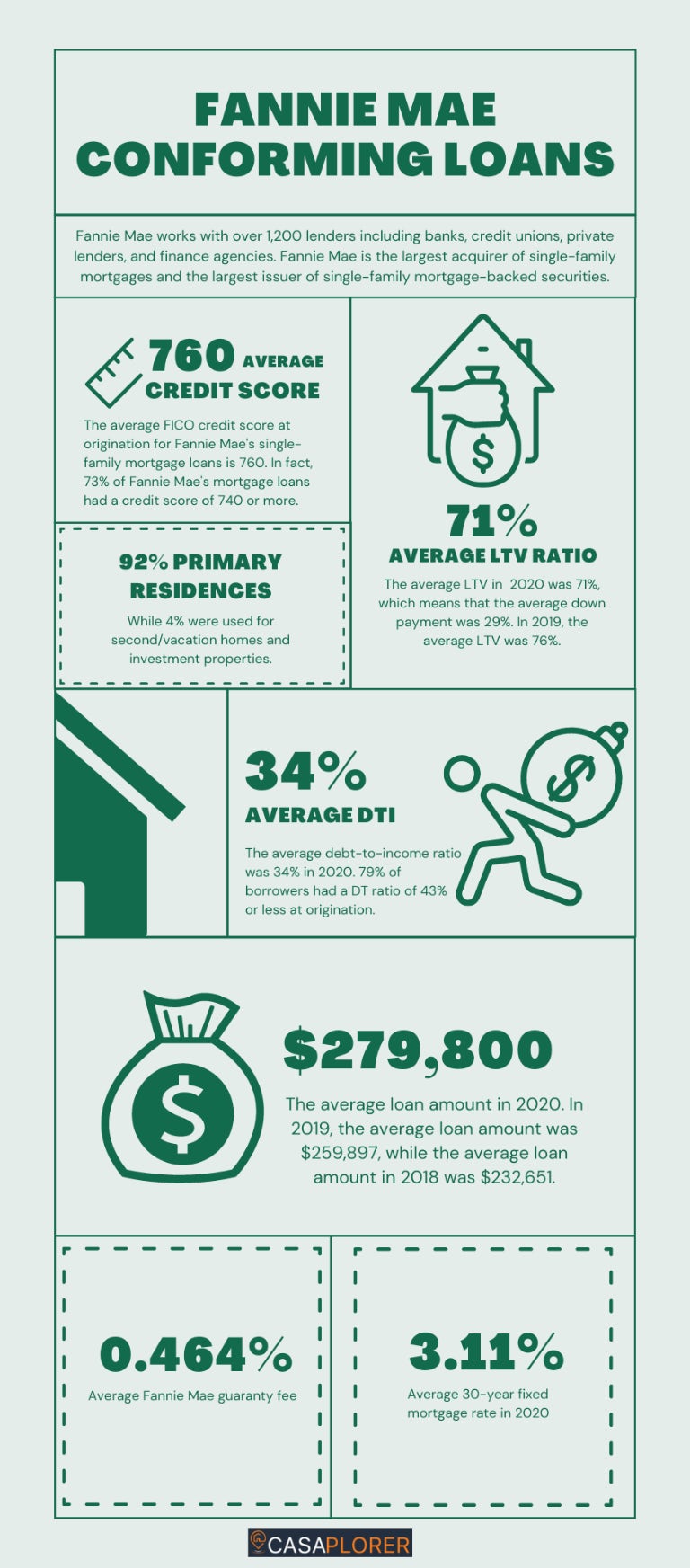

Conforming Loan Statistics

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.

- The names and logos of third-party products and companies displayed on this website are the property of their respective owners and may also be trademarks.