VA Loan Calculator 2026

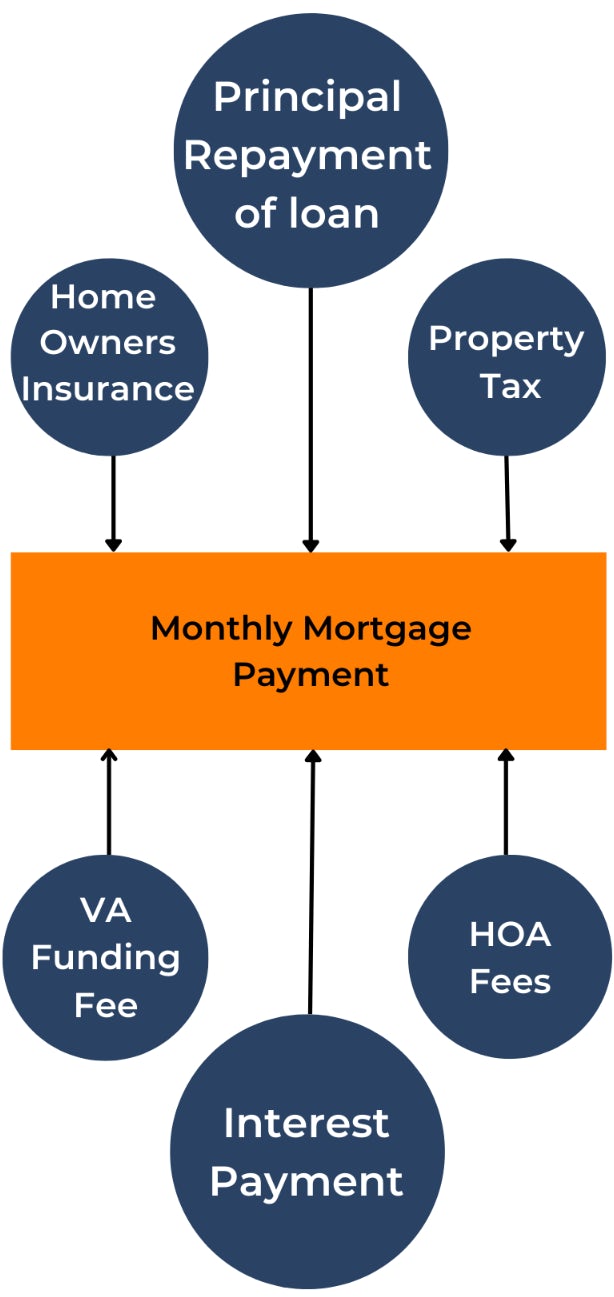

The VA loan calculator provides the monthly mortgage payment for a VA loan. The monthly mortgage payment includes the principal repayment, interest, taxes, insurance, and the VA funding fee. The VA funding fee is an important expense of the VA loan and is a one-time expense that can be paid up front or financed into your monthly mortgage payment.

How does the VA Loan Calculator work?

The VA loan calculator calculates the monthly mortgage payment for the VA loan. The mortgage rates, requirements, and eligibility criteria can be found on the VA loan page. The calculator works by calculating the principal and interest and additional costs such as the VA funding fee, which can be a significant expense. The following inputs are required by the calculator:

- Home Price – the purchase price of the home you are buying. The VA loan limits were removed in 2020; hence, no matter the size of the loan, it can be eligible to be insured by the Department of Veterans Affairs.

- Down Payment – There is no minimum down payment for the VA loan if your purchase price is less than or equal to the appraised value of your home. Otherwise, your minimum down payment is the difference between the price and the appraised value. The VA loan is one of the few mortgage programs apart from the USDA loan, where a 0% down payment is possible. Though it is possible to buy your residence with zero down payment, it is beneficial to make as large of a down payment as affordable.

- VA Loan Type – There are four different types of loans guaranteed by the Department of Veteran Affairs, VA Purchase loan, Cash-out Refinance loan, VA Interest Rate Reduction Refinance Loan (IRRRL), and Construction loans. The first one is for home buyers, and the next two are for homeowners looking to refinance.

- VA Status – There are three options, regular military, reserves/national guard, and if you are the surviving spouse of a veteran. If you are a surviving spouse of a veteran who lost their life in connection with their service, the VA funding fee is waived.

- VA Options – Veterans who have a service-related disability do not have to pay the VA funding fee, whereas if the VA loan program has been used before then the VA funding fee will be higher.

- Interest Rate – VA mortgage rates are competitive. They change based on credit score and down payment.

- State – This helps determine the average property tax in the area.

- Additional Options – Fees such as property taxes, insurance, and HOA fees are also included to provide the total monthly mortgage payment.

The monthly payment is calculated using the amortization formula along with the additional fees. The VA funding fee is unique to the VA loans and the amount depends on the type of VA loan, down payment, and VA options such as first-time use or VA disabled.

Can I lower my VA Loan monthly mortgage payment?

To reduce your monthly mortgage payment:

- Longer Loan Term: Initially, if you had selected a 15-year mortgage, consider taking a 30-year mortgage. A longer term will extend the life of the loan and will result in lower mortgage payments because amortization occurs over a more extended period. However, in a 30-year mortgage, the total interest paid for the mortgage rises.

- Larger Down Payment: VA loans do not have a minimum down payment requirement, which is a great benefit for veterans, as other mortgage programs have minimum down payment, e.g., the FHA loan has a 3.5% down payment requirement. With a larger down payment, the mortgage amount is smaller, and hence the monthly payment and total interest are also smaller.

- Lower Home Price: If the home price can be negotiated to be lower or a home with a lower price tag is bought, then the monthly payment will be lower as a smaller amount is borrowed.

- Lower Interest Rates: Although VA mortgage rates are very competitive, different lenders can alter the rate based on other factors such as credit score, debt-to-income (DTI) ratio, and the loan-to-value (LTV) ratio. Hence, it is wise to shop around for a lower mortgage rate, which will reduce interest and the monthly mortgage payment.

What is the VA Funding Fee?

The VA funding fee is a one-time fee that has to be paid by the home buyer. VA loans do not have private mortgage insurance (PMI) or a minimum down payment and have competitive mortgage rates. The VA funding fee must cover the costs of the VA loan program.

How much is the VA Funding Fee?

The average VA funding fee for a home purchase loan is 2.3% of the mortgage amount. However, the VA funding fee can be 0 – 3.6% based on several factors. The size of the VA funding fee depends on three main elements, the type of VA loan, the amount of down payment, and whether this is the first or subsequent use of the VA program. The department of veteran affairs waives the VA funding fee if the veteran has a service-related disability or if the VA loan is for a surviving spouse.

VA Funding Fee for Purchase and Construction Loans

The VA Funding Fee table below shows the VA funding fee as a percentage of the mortgage amount for purchase and construction loans.

VA Funding Fee Table (for purchase or construction)

| Down Payment | First Time Use | Subsequent Use |

|---|---|---|

| Less than 5% | 2.3% | 3.6% |

| 5% to 10% | 1.65% | 1.65% |

| Greater than 10% | 1.4% | 1.4% |

If you have a down payment of less than 5%, then the VA funding fee is 2.3% of the mortgage amount for borrowers who are using the VA program for the first time. The VA funding fee is 3.6% for a VA loan with a down payment of less than 5% if this borrower has already used the program in the past. As the down payment increases over 5%, the funding fee reduces to 1.65% up to a 10% down payment, and then to 1.4% for any down payment greater than 10%. Also, note that if you have used a VA loan to buy only a manufactured home in the past, you still get the first-time user funding fee. The VA funding fee for purchasing a manufactured home is 1% of the loan amount.

VA Funding Fee for VA Cash-out Refinance Loans

The VA cash-out refinance provides veterans the opportunity to refinance their mortgage at a lower rate and take cash out from the equity in their home. The funding fee for the VA cash-out refinance loan is similar to the purchase loan with less than a 5% down payment. In other words, the funding fee for the first use of a VA guarantee is 2.3% of the loan value, while it is 3.6% of the loan value for subsequent uses. Thus in cash-out refinance loans, the funding fee is independent of the down payment amount.

VA Funding Fee Table (for cash-out refinance)

| First Time Use | Subsequent Use |

|---|---|

| 2.3% | 3.6% |

VA Funding Fee for VA Interest Rate Reduction Refinance Loans (IRRRL)

The VA IRRRL, which is also known as VA streamline refinance, allows veterans to refinance their mortgages at a lower rate or even convert their adjustable-rate mortgages (ARM) into a fixed-rate mortgage. The funding fee for the VA IRRRL is 0.5% of the mortgage amount and is not dependent on a down payment or the number of times the VA loan program has been used.

VA Funding Fee Table (for IRRRL)

| First Time Use | Subsequent Use |

|---|---|

| 0.5% | 0.5% |

How do I pay the VA Funding Fee?

The VA funding fee has to be paid to the lender, who then sends it to the Department of Veterans Affairs. There are two different methods of paying the funding fee:

- Financing the fee into the mortgage amount, the monthly mortgage payment increases to include the fee.

- Paying the fee at closing

Exemptions for the VA Funding Fee

You will not have to pay the VA funding fee if you are:

- A Purple Heart Recipient (Service members killed or wounded by enemy action receive a purple heart medal.)

- A surviving spouse of a veteran.

- The receiver of VA compensation for a service-linked disability.

- Eligible to receive VA disability compensation but are receiving active pay or retirement pay instead.

Closing costs

The Department of Veteran Affairs strictly limits what costs can be borne by the veteran. Thus, for example, the seller should pay real estate commissions, brokerage fees, and termite report costs. Other expenses such as the VA funding fee, loan origination fee, loan discount points or buydowns, credit report or payment of credit balances and judgments, VA appraisal fee, hazard insurance , real estate taxes, title insurance, and recording fee can be paid either by the seller or by the buyer if the seller agrees to pay some of these costs it is considered a seller concession. Note that according to VA rules, seller concessions like those just mentioned cannot exceed 4% of the loan value. VA limits the loan origination fee to 1% of the loan amount for purchase loans. Lenders can charge up to 3 percent of the loan value for construction loans if they oversee the construction. Otherwise, the maximum they can charge is 2% of the loan value.

VA has a list of charges called itemized fees and charges. The lender can charge any of the itemized fees and charges to the veteran. Other than these, the lender should cover any cost of the lending process as the lender is charging a flat fee for originating the loan. VA appraiser and VA compliance inspector fees, second appraisal if requested by the veteran, credit report fee, hazard insurance premium, flood zone determination fee, the survey fee, title examination, and insurance cost, and recording fees & taxes are among itemized fees and can be paid by the veteran. A second appraisal, requested by any party other than the veteran, is not among itemized fees and cannot be paid by the veteran.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.