USDA Loan Eligibility Map 2026

CASAPLORER®Trusted & TransparentThe United States Department of Agriculture has eligibility requirements for their housing loan programs, which includes debt and credit score criteria along with maximum household income limits that vary by county. This USDA eligibility calculator checks to see if you are eligible for a USDA loan based on current USDA eligibility requirements, and whether or not you qualify for automatic approval or if manual review is needed.

USDA Loan Eligibility Calculator

Where will your home be located? Please select state and county.

What is your yearly household income and total monthly debt payment?

What is your credit score?

Please answer the following questions:

You are Eligible for the USDA Loan

What are the USDA Loan Eligibility Requirements?

USDA loans have several criteria in order to determine loan eligibility. The USDA eligibility calculator above can determine eligibility with some basic information. Here are the following requirements for a USDA Home Loan:

| Criteria | USDA Requirement |

|---|---|

| Status | US Citizen or Lawful Permanent Resident |

| Location | Within an Eligible Rural Area |

| Type of Residence | Primary Residence |

| Household Income | Household Income < 115% Median Income |

| Debt Requirement | Debt-to-Income (DTI) Ratio < 41% |

| Minimum Credit Score | No Credit Score Requirement |

- Residency Status - The individual taking out the USDA loan must be a US citizen or lawful permanent resident.

- Location - The home must be located in an eligible rural area. The USDA considers an area to be rural if its population is 10,000 or less, or if its population is 20,000 or less and it is not located inside a metropolitan statistical area (MSA). If your county is not available in the above USDA eligibility calculator, your area is not eligible for a USDA loan.

- Primary Residence - The home must be the primary residence of the home buyer. USDA loans cannot be used for real estate investment purposes, vacation homes, and the purchase of farms.

- Household Income

- There must be a dependable source of income for payments, which can be proven by showing tax returns for the past 24 months. USDA loans also have clauses that allow for unforeseen circumstances such as loss of a job, medical emergency, or other events beyond the applicant’s control. /in these cases, the lender can make exceptions regarding the borrower’s finances.

- Your annual household income cannot exceed 115% of the median income for your county. For example, if the median household income in the area is $100,000, to be eligible, your income must be below $115,000 ($100,000 x 115%).

- The income of anyone in your household over the age of 18 and not a student will be counted towards your household income.

- Debt Requirement - Your debt-to-income (DTI) ratio must be less than 41%. The DTI ratio is defined by Fannie Mae as the total monthly debt payments for loans such as auto & student loans and the sum of minimum monthly payments for credit cards divided by monthly household income. This means that monthly debt repayments such as auto loan payments, student loan payments, and your minimum credit card payments cannot exceed 41% of your monthly income. For example, if monthly income is $5,000 then the monthly debt payments cannot be greater than $2,050 ($5000 x 41%).

- Minimum Credit Score - There are no minimum credit score requirements for a USDA loan, but you do need an acceptable credit history. If an acceptable credit history is not available, USDA lenders can also accept non-traditional credit reports that credit agencies manually produce based on proof of payment. The credit agency can look at the recurring payment for utility, insurance, tuition, rent payments, and even childcare expenses. Credit score is not an eligibility requirement, but it does help determine if you are a candidate for a streamlined application process or a manual process.

- If credit score is above 640 – USDA Loan with Streamline Process

- If credit score is below 640 – USDA Loan with Manual Process

- The streamlined process is a lot faster as all the requirements are standardized allowing you to be accepted for a USDA loan quickly. For new USDA loans, your application can be processed through an automated underwriting system if your credit score is 640 or greater. Other government loans also have streamlined options for mortgage refinancing, such as FHA streamline refinance and VA IRRRL (streamline refinance). The manual approval process occurs if your credit score is below 640 as this poses additional risk for the lender. The lender and USDA might require more details and information to process your USDA loan application.

What Is a Rural Area?

USDA loans can only be used to build, buy, or repair a home in designated rural areas. Rural areas are defined by the USDA as either:

- Having a population of 10,000 or less

- Having a population of 20,000 or less, only if it is not part of a metropolitan statistical area (MSA)

- Having a population of 35,000 or less if it was once considered to be a rural area

Metropolitan statistical areas, also known as metropolitan areas or metro areas, are highly populated and have at least one urban core. For example, the most populated MSA in the United States is New York-Newark-Jersey City, while the second-most populated is Los Angeles-Long Beach-Anaheim. Even though you won’t be able to get a USDA home loan in these urban areas, you may still be eligible for suburban properties.

You can use the USDA’s eligibility map found on their website to see if your property is eligible for a USDA loan by being in a rural area.

Historical USDA Income Limits

USDA income limits are updated once every year. The line chart below shows how the income limits for most counties have changed over the years.

| Year | USDA Guaranteed Income Limit* | Change |

|---|---|---|

| 2015 | $75,650 | - |

| 2016 | $75,650 | 0% |

| 2017 | $78,200 | 3.4% |

| 2018 | $82,700 | 5.8% |

| 2019 | $86,850 | 5% |

| 2020 | $90,300 | 4% |

| 2021 | $91,900 | 1.8% |

* For a 1-4 person household

USDA Loan Limits

USDA Guaranteed Loans, which are USDA loans offered through private lenders such as banks, do not have a maximum loan limit. Instead, USDA Guaranteed Loans have maximum household income limits that are shown on the USDA eligibility map above. The maximum household income limit for USDA Guaranteed Loans ranges from $91,900 in most counties to as high as $156,250 in Santa Ana - Anaheim - Irvine, California.

USDA Direct Loans, which are USDA loans offered directly by the USDA for low to very-low income borrowers, do have a maximum loan limit. They also have lower maximum household income limits than USDA Guaranteed Loans.

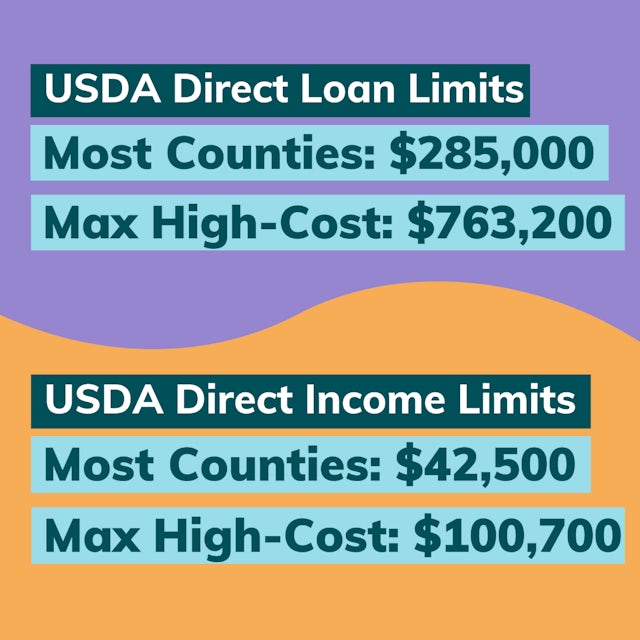

The maximum USDA Direct loan limit for most counties is $285,000 for 2022. In high-cost counties, the maximum loan limit can be as high as $763,200.

The maximum household income limit for USDA Direct loans can range from $42,500 in some counties to as high as $100,700 for a 1-4 person household.

Highest USDA Direct Loan Limits by County

| County | Loan Limit |

|---|---|

| Sonoma County, California | $763,200 |

| Honolulu County, Hawaii | $725,000 |

| Kauai County, Hawaii | $725,000 |

| Maui County, Hawaii | $725,000 |

| Napa County, California | $706,900 |

| King County, Washington | $659,800 |

| Pierce County, Washington | $659,800 |

| Snohomish County, Washington | $659,800 |

| Los Angeles County, California | $657,900 |

What county has the highest USDA loan limits?

For 2022, the highest USDA Direct loan limit is in Sonoma County, California, with a loan limit of $763,200. The county with the highest USDA Direct income limit is Honolulu, Hawaii, which allows a household income of up to $100,700.

USDA Guaranteed vs. Direct Loan Eligibility

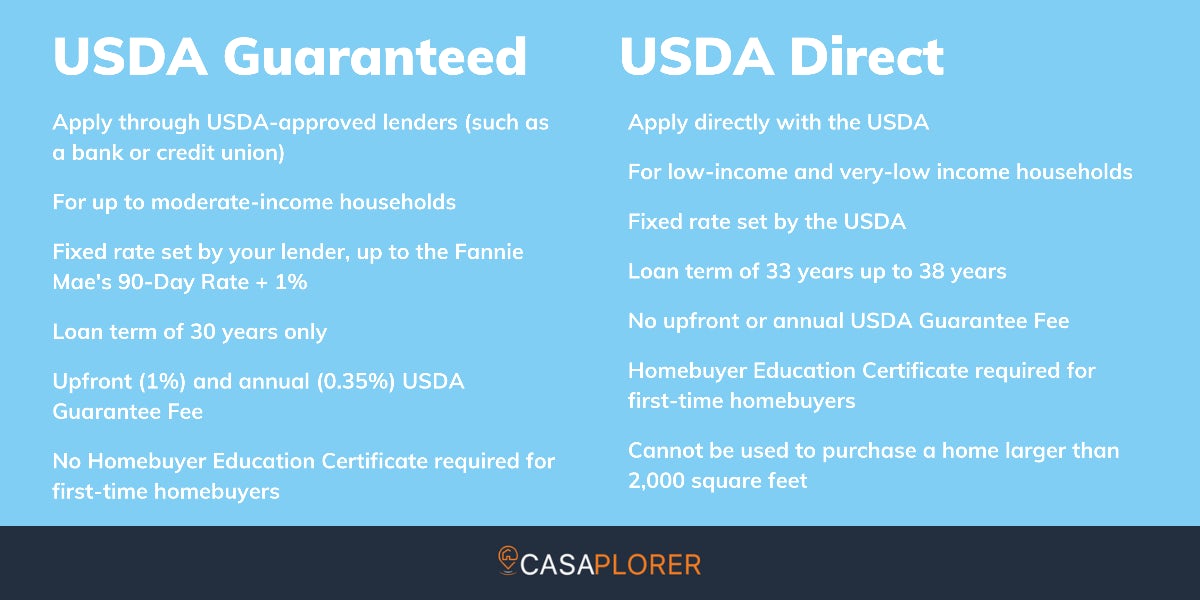

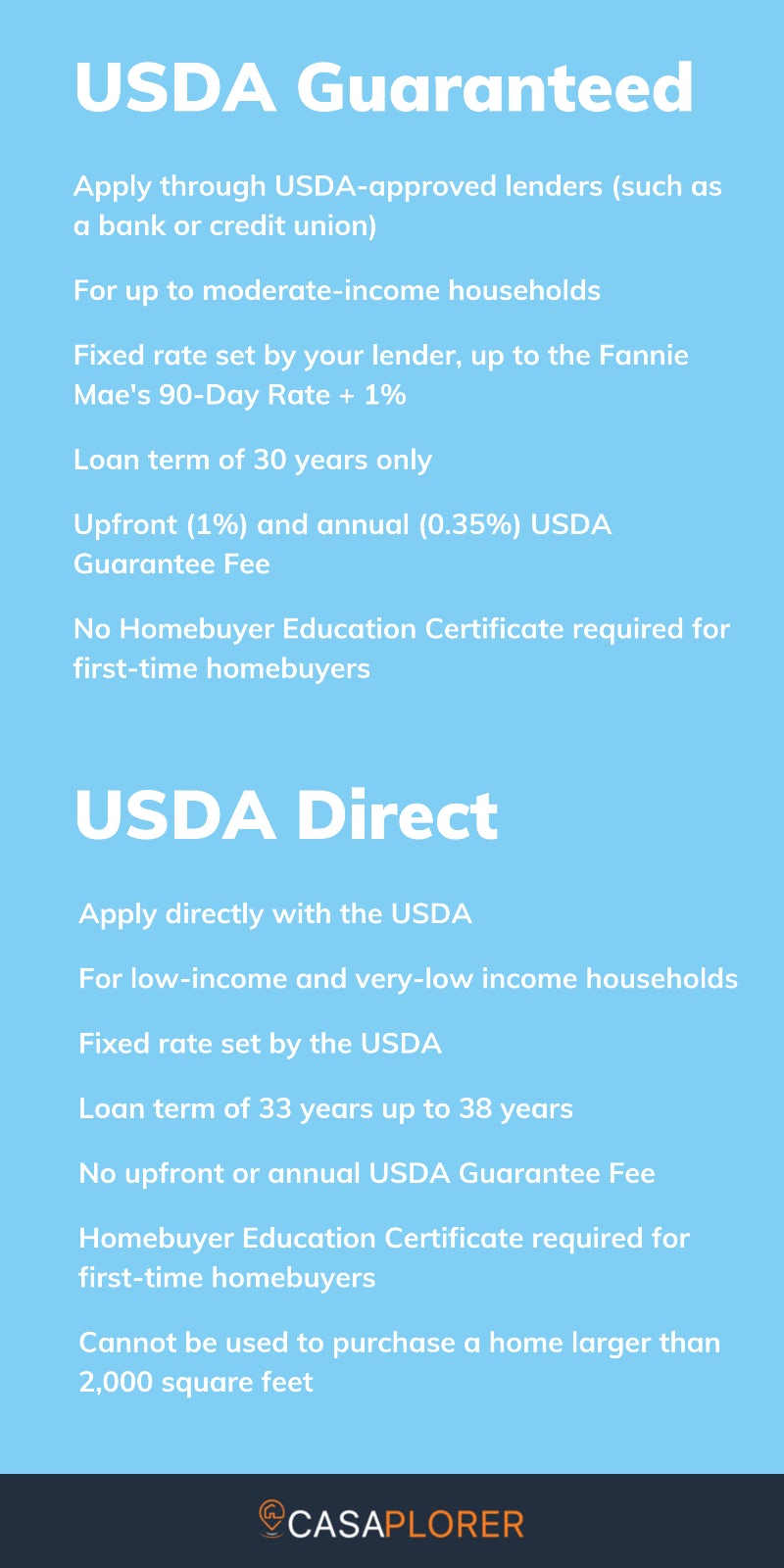

There are some differences in requirements between USDA Guaranteed loans and USDA Direct loans. The main difference is that USDA Guaranteed loans are intended for low-income and moderate-income households, while USDA Direct loans are restricted to low-income and very-low income households.

Low and very-low income households also face another eligibility requirement through repayment ratios. For low-income households, the total amount of monthly principal, mortgage interest, property taxes, and insurance (including USDA mortgage insurance) payments cannot be more than 33% of their monthly income. For very-low income households, their PITI payments cannot be more than 29% of their monthly income. This is in addition to the maximum DTI ratio limit of 41%.

While there is a maximum limit to the amount of monthly housing payments that can be made, USDA Direct borrowers will have a loan term of 33 years, longer than the USDA Guaranteed loan term length of 30 years. Very-low income borrowers can even choose to have a loan term of up to 38 years if they can’t afford a 33-year term. The longer term lengths of USDA Direct loans allow monthly mortgage payments to be spread out over a longer period of time, reducing the size of each payment.

Homes that are larger than 2,000 square feet are not eligible for a USDA Direct loan. The square footage of a home is limited due to USDA Direct loans being restricted to “modest” homes for low and very-low income households. First-time homebuyers looking to get a USDA Direct loan are also required to complete a homebuyer education course in order to be eligible.

USDA Loan Automated Underwriting Process

If you have a credit score of 640 or higher, your USDA loan application can be processed by your lender through an automated underwriting process. The USDA's automated process is called the Guaranteed Underwriting System (GUS). While GUS does not provide automatic approvals of USDA loans, it does provide guidance and underwriting recommendations to USDA lenders. The borrower’s data, including income, must be verified before they can be entered into GUS. The system will also check the borrower’s credit report through the Fannie Mae Credit Interface Service.

The Guaranteed Underwriting System will provide one of four recommendations when evaluating your credit, capacity, and collateral:

- Accept

- Refer

- Refer with caution

- Ineligible

An "accept" recommendation means that your credit, capacity, and collateral is acceptable. It does not mean that your loan is automatically approved. A "refer" recommendation means that your application will need to be manually reviewed. A "ineligible" recommendation means that your application will be denied.

When looking at your property, income, and application eligibility, the recommendations can be either eligible, ineligible, or unable to determine. If eligible, then that means the property is located in an eligible rural area and your income meets the USDA's income limits. Ineligible means that your property is not located in an eligible rural area and your income is over the annual income limit. Unable to determine means that the system couldn’t find the property and manual review will be needed.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.