How to Get Your Free Credit Report and Credit Score

CASAPLORER®Trusted & TransparentHow to Get a Free Credit Report

The Fair Credit Reporting Act (FCRA), part of the Consumer Credit Protection Act (CCPA), is a federal law that requires credit bureaus to provide consumers with a free copy of their credit report at least once every 12 months. Due to the pandemic, you can now get your free credit report once a week online at AnnualCreditReport.com. This weekly benefit ends on April 20, 2022, and will return back to annual free reports.

The free weekly credit reports are provided by Equifax, TransUnion, and Experian, which are the three main credit bureaus in the U.S. To get a copy of your free credit report, visit:

Check Your Free Credit Report

This link will take you to the official AnnualCreditReport.com website.

Three Main Credit Bureaus

There are 3 main credit reporting agencies that are required by federal law to provide you with your free annual credit report: TransUnion, Experian, and Equifax. You may be eligible to receive more frequent credit reports with these credit reporting agencies by requesting a free credit report directly through them. These credit bureaus also have additional products and services, such as credit score access, credit monitoring, or identity theft protection, available for a fee as a subscription. You may be able to receive these paid services for free from other providers.

TransUnion

TransUnion had its start in 1969 when it acquired the Credit Bureau of Cook County. By 1988, TransUnion had expanded across the United States. Today, TransUnion collects data on 1 billion consumers in over 30 countries through 90,000 data sources.

TransUnion offers credit monitoring for $24.95 per month. This allows you to receive your TransUnion credit score and allows you to check your TransUnion credit report daily. You will also get instant credit alerts and identity theft insurance.

TransUnion offers a free annual credit report through AnnualCreditReport.com. This free credit report does not include your credit score, however, access to your VantageScore 3.0 is available at a cost. TransUnion does not directly allow you to access more frequent credit report checks for free, unless required by the Fair Credit Reporting Act.

To check your TransUnion credit report for free, visit TransUnion’s website.

Experian

Unlike TransUnion, Experian allows you to check your credit score directly for free. Experian offers free monthly credit reports with FICO Score included, as well as free credit monitoring.

Starting from $9.99 per month, you can receive your Experian FICO Score daily. For $19.99 per month, you can receive your credit scores from Experian, Equifax, and TransUnion quarterly. You will also get identity theft monitoring and identity theft insurance.

To check your Experian credit report and credit score for free, visit Experian’s website.

Equifax

By registering for a free myEquifax account, you will be able to receive six free Equifax credit reports each year. You can also get your six additional free Equifax credit reports per year from AnnualCreditReport.com. This benefit ends on December 31, 2026.

The free Equifax Core Credit service also allows you to check your Equifax credit report and credit score for free once per month. No credit card is required in order to sign up for Equifax Core Credit.

Equifax's paid subscriptions start from $4.95 for credit monitoring and daily credit score and credit report access. For access to all three bureau credit scores and credit reports once per year, the subscription costs $19.95 per month.

To check your Equifax credit report and credit score for free, visit Equifax’s website.

Are You Entitled to Additional Free Credit Reports?

Besides the annual free disclosure, the Fair Credit Reporting Act requires credit bureaus to provide free credit reports under certain circumstances. You may be eligible to receive a free one-time credit report if:

- You request for a credit report within 60 days of an adverse notice. An adverse notice includes being denied credit, insurance, or employment based on your credit report. It also includes being informed by a debt collection agency that your credit score may be impacted due to a collection.

- You request a credit report due to a fraud alert.

- You believe that you are a victim of fraud.

- You are unemployed and are looking to apply for employment within 60 days.

- You are currently receiving public welfare assistance.

You are also eligible to receive an additional free credit report once every 12 months if you are a resident of any of the following states:

- Alabama

- Alaska

- Arizona

- Arkansas

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Mississippi

- Missouri

- Nebraska

- Nevada

- New Mexico

- New York

- North Carolina

- Ohio

- Oregon

- Pennsylvania

- Rhode Island

- Tennessee

- Texas

- Vermont

- Wisconsin

If you qualify for free additional credit reports, by being a resident of these states or by being eligible due to the circumstances stated in the Fair Credit Reporting Act, you will need to request for these credit reports manually from each credit bureau:

TransUnion: www.transunion.com/credit-reports-disclosures/free-credit-report

Experian: www.experian.com/reportaccess/

Equifax: www.equifax.com/fcra

States With Free Annual Credit Reports

Some states require the first credit report per year to be free, and require credit bureaus to offer additional credit reports at a reduced fee. These states are:

- Colorado, $8 per additional report

- Georgia, $11.50 per additional report

- Maine, $5 per additional report

- Maryland, $5 per additional report

- Massachusetts, $8 per additional report

- New Jersey, $8 per additional report

- Puerto Rico, $11.50 per additional report

- Vermont, $7.50 per additional report

Some states do not require the first credit report per year to be free, but requires credit bureaus to allow residents of these states to purchase one additional credit report at a reduced price:

- California, $8 per credit report

- Connecticut, $5 for the first credit report in a 12-month period, then $7.50 for additional reports

- Minnesota, $3 for the first credit report in a 12-month period, then $11.50 for additional reports

- Montana, $8.50 per credit report

More Ways to Get Your Credit Score and Report For Free

Besides getting your credit score directly from one of the major credit bureaus, you can also check your credit report and credit score for free from banks and credit unions. In most cases, you will need to be a customer with online or mobile banking in order to access your credit report and score for free. Some credit card issuers also offer free access to your credit score.

Summary of Free Credit Score and Credit Reports

| Banks | ||||

|---|---|---|---|---|

| Bank | Update Frequency | Credit Model | Credit Bureau | |

| Chase | Weekly | VantageScore 3.0 | Experian | |

| Wells Fargo | Monthly | FICO Score 9 | Experian | |

| Morgan Stanley | Monthly | VantageScore 3.0 | Experian | |

| US Bank | Monthly | VantageScore 3.0 | TransUnion | |

| Credit Card Issuers | ||||

| Credit Card Issuer | Update Frequency | Credit Model | Credit Bureau | |

| American Express | Weekly | VantageScore 3.0 | TransUnion | |

| Capital One | Weekly | VantageScore 3.0 | TransUnion | |

| Bank of America | Monthly | FICO Score | TransUnion | |

| Citi | Monthly | FICO Score 8 | Equifax | |

| Navy Federal | Monthly | VantageScore 3.0 | TransUnion | |

| HSBC | Monthly | FICO Score | Equifax | |

| Discover | Monthly | FICO Score | Experian | |

| Third-Party Services | ||||

| Company | Update Frequency | Credit Model | Credit Bureau | |

| Credit Karma | Weekly | VantageScore 3.0 | TransUnion/ Equifax | |

| Mint | Weekly | VantageScore 3.0 | TransUnion | |

| Credit Sesame | Monthly | VantageScore 3.0 | TransUnion | |

| NerdWallet | Weekly | VantageScore 3.0 | TransUnion | |

| LendingTree | Monthly | VantageScore 3.0 | TransUnion | |

Banks

Chase

- How often can you check? - Weekly

- Credit score provided - VantageScore 3.0 by Experian

- Credit alerts? ✅

- Available to non-customers? ✅

With Chase Credit Journey, you can check your credit score for free without needing to have a Chase bank account. The credit score provided is VantageScore 3.0 by Experian, and it updates weekly. Chase also offers free credit monitoring and identity monitoring. This allows you to receive alerts anytime there is no activity on your account, such as a new account or credit inquiry.

Wells Fargo

- How often can you check? - Monthly

- Credit score provided - FICO Score 9 by Experian

- Credit alerts? ❌

- Available to non-customers? ❌

Wells Fargo gives you access to your FICO Score 9 by Experian through their Credit Close-Up program, as well as access to your Experian credit report. Your credit score and credit report updates monthly with Wells Fargo. You must be a Wells Fargo customer and enrolled in online banking in order to be eligible for Wells Fargo's Credit Close-Up program. You are considered to be a Wells Fargo customer if you have a deposit, loan, or credit account with Wells Fargo as the primary account holder.

Morgan Stanley

- How often can you check? - Monthly

- Credit score provided - VantageScore 3.0 by Experian

- Credit alerts? ✅

- Available to non-customers? ❌

Morgan Stanley offers complimentary identity and credit protection by Experian to Morgan Stanley clients. This gives you access to credit reports and credit scores from all three bureaus once per month, as well as credit alerts and monitoring. You can also get up to $1 million identity theft insurance.

This identity and credit protection benefit also extends to family members for eligible clients. Platinum Morgan Stanley clients can protect up to four adults in a family, while Premier Morgan Stanley clients can protect up to two adults in a family.

US Bank

- How often can you check? - Monthly

- Credit score provided - VantageScore 3.0 by TransUnion

- Credit alerts? ✅

- Available to non-customers? ❌

Being a U.S. Bank online or mobile customer gives you free access to your VantageScore 3.0 by TransUnion. This score is updated monthly. U.S. Bank also offers free credit alerts through the TransUnion CreditView Dashboard.

American Express

- How often can you check? - Weekly

- Credit score provided - VantageScore 3.0 by TransUnion

- Credit alerts? ✅

- Available to non-customers? ✅

American Express MyCredit Guide is available to both American Express members and to non-cardmembers. The credit score provided is your VantageScore 3.0 by TransUnion, and it is updated weekly. You'll also get access to your TransUnion credit report for free. Rounding out the MyCredit Guide offerings is credit alerts, credit score goals, and a credit score simulator.

Capital One

- How often can you check? - Weekly

- Credit score provided - VantageScore 3.0 by TransUnion

- Credit alerts? ✅

- Available to non-customers? ✅

Capital One CreditWise provides free weekly credit score updates provided by TransUnion. You don’t need to have a Capital One credit card in order to use this free service. CreditWise lets you check your VantageScore 3.0 every week, as well as gives you access to your TransUnion credit report for free. Other benefits include credit alerts with TransUnion, a credit simulator, SSN tracking, dark web surveillance alerts, and credit monitoring with both TransUnion and Experian.

Bank of America

- How often can you check? - Monthly

- Credit score provided - FICO Score by TransUnion

- Credit alerts? ❌

- Available to non-customers? ❌

Bank of America offers free monthly FICO Score updates provided by TransUnion to Bank of America credit card customers. While there is no credit monitoring provided, you can track your monthly credit score to see how it changes over time. Bank of America also provides personal finance resources to help you improve your credit score.

Citi

- How often can you check? - Monthly

- Credit score provided - FICO Score 8 by Equifax

- Credit alerts? ❌

- Available to non-customers? ❌

Citi cardmembers can access their FICO Bankcard Score 8 from Equifax which is updated once per month. Only the primary cardmember can check their credit score for free with Citi. Authorized users, as well as those with a joint account, cannot check their credit score with Citi. It can take up to two months after becoming a Citi cardmember before you can access your FICO Score.

Navy Federal Credit Union

- How often can you check? - Monthly

- Credit score provided - VantageScore 3.0 by TransUnion

- Credit alerts? ❌

- Available to non-customers? ❌

Navy Federal Credit Union's Mission: Credit Confidence offers monthly credit score updates for Navy Federal cardholders. The credit score provided is VantageScore 3.0 by TransUnion. You can receive credit score alerts when your score changes, as well as set credit score goals. There's also a score simulator where you can estimate what your credit score would be if you add or reduce debt, or add a new credit account.

HSBC

- How often can you check? - Monthly

- Credit score provided - FICO Score by Equifax

- Credit alerts? ❌

- Available to non-customers? ❌

If you have a HSBC Credit Card, you can check your FICO Score by Equifax for free every month. You will need to be the primary account holder in order to be eligible. Authorized users of a HSBC credit card cannot check their FICO Score for free with HSBC's service.

Discover

- How often can you check? - Monthly

- Credit score provided - FICO Score by Experian

- Credit alerts? ✅

- Available to non-customers? ✅

Discover’s Credit Scorecard lets both cardmembers and non-customers check their Experian FICO Score for free once per month. Included is SSN monitoring and credit alerts. Discover's Credit Scorecard stopped accepting new registrations on March 1, 2022. The free service will end on June 6, 2022.

Third-Party Services

Credit Karma

- How often can you check? - Weekly

- Credit score provided - VantageScore 3.0 by TransUnion or Equifax

- Credit alerts? ✅

- Available to non-customers? ✅

Credit Karma, owned by Intuit, offers weekly credit score updates through Equifax and TransUnion. You can get your free Equifax credit report and TransUnion credit report with Credit Karma. You'll also get free credit monitoring on both your TransUnion and Equifax credit reports. However, the VantageScore 3.0 credit score that you receive will only be from either Equifax or TransUnion, not both.

Mint

- How often can you check? - Weekly

- Credit score provided - VantageScore 3.0 by TransUnion

- Credit alerts? ✅

- Available to non-customers? ✅

Mint is part of the Intuit family, which includes TurboTax, QuickBooks, and Credit Karma. With Mint, you can check your credit score weekly. The score provided is VantageScore 3.0 by TransUnion. You'll also get your TransUnion credit report for free, as well as daily credit monitoring and alerts for your TransUnion profile.

Credit Sesame

- How often can you check? - Monthly

- Credit score provided - VantageScore 3.0 by TransUnion

- Credit alerts? ✅

- Available to non-customers? ✅

Credit Sesame offers monthly credit score updates with free credit report checks and free credit monitoring. On top of this, you'll also get free identity theft protection with up to $1 million identity theft insurance. With a Premium subscription, starting from $9.95 per month, you can get daily credit score updates from 1 credit bureau and monthly credit score updates from all three credit bureaus.

NerdWallet

- How often can you check? - Weekly

- Credit score provided - VantageScore 3.0 by TransUnion

- Credit alerts? ✅

- Available to non-customers? ✅

NerdWallet offers free weekly credit score and credit report updates. Credit monitoring is also free.

LendingTree

- How often can you check? - Monthly

- Credit score provided - VantageScore 3.0 by TransUnion

- Credit alerts? ✅

- Available to non-customers? ✅

LendingTree lets you check your credit score monthly and offers free credit monitoring.

What Is the National Average Credit Score?

According to Experian, the average credit score in the U.S. was 714 in 2021.

Other Consumer Reporting Agencies

TransUnion, Experian, and Equifax aren’t the only consumer reporting agencies in the United States. There are speciality consumer reporting agencies, which are companies that collect your employment history, medical insurance history, tenant history, and property insurance claim history. Some of these agencies are owned by the clients that they provide services for. As an example, Early Warning Services, which detects and prevents fraud, is co-owned by Bank of America, BB&T, Capital One, JPMorgan Chase, PNC Bank, U.S. Bank and Wells Fargo.

Just like the major credit bureaus, these consumer reporting agencies have to follow the Fair Credit Reporting Act. This means that you can request to see your report from these reporting agencies for free, once every year.

List of Consumer Reporting Agencies

Check and Bank Screening

- Certegy Check Services

- ChexSystems

- CrossCheck

- Early Warning Services

- Global Payments Check Services

- TeleCheck Services

Employment Screening

- Accurate Background

- ADP Screening & Selection Services

- BackgroundChecks.com

- Checkr

- EmpInfo

- First Advantage Corporation

- General Information Services (GIS)

- HireRight

- Info Cubic

- IntelliCorp

- OPENonline

- Pre-Employ.com

- Sterling

- Truework

- The Work Number

Tenant Screening

- Contemporary Information Corp. (CIC)

- CoreLogic Rental Property Solutions

- Experian RentBureau

- First Advantage Corporation Resident Solutions

- Real Page (LeasingDesk)

- Screening Reports

- TransUnion SmartMove

Medical

- MIB

- Milliman IntelliScript

Subprime Borrowers

- Clarity Services

- CoreLogic Teletrack

- DataX

- FactorTrust

- MicroBilt

Personal Property Insurance

- A-PLUS Property

- LexisNexis C.L.U.E

- Drivers History (TransUnion)

- Insurance Information Exchange (iiX)

FICO Score Versions

The most commonly used FICO Score version is FICO Score 8. The version number changes based on the credit score model used. For example, FICO Score 9 is a newer update of the older FICO Score 8 model. As of 2022, the newest FICO Score version is FICO Score 10 and FICO Score 10T. Lenders choose which FICO Score version that they want to use. They do not have to use the latest version.

FICO releases new score models based on credit behavior of consumers. For example, FICO Score 9 now incorporates rental history, which was absent from FICO Score 8. FICO Score 9 also allows paid-off collections to not have a negative impact on your credit score. FICO 10T introduces historical data for the past 24 months, giving lenders a look at the trend of a consumer's credit behavior.

There are some industry specific FICO versions that are exclusively used. For example, FICO Auto Score is used by auto loan lenders, while FICO Bankcard Score is used by credit card issuers. If you are looking to get a mortgage, your FICO Score 2, FICO Score 5, or FICO Score 4 will be used by your mortgage lender, depending on the credit bureau that your credit report is drawn from.

Which FICO Scores Do Mortgage Lenders Use?

| Experian | Equifax | TransUnion |

|---|---|---|

| FICO Score 2 | FICO Score 5 | FICO Score 4 |

| Experian/Fair Isaac Risk Model v2 | Equifax Beacon 5 | TransUnion FICO Risk Score, Classic 04 |

Source: myFICO

Frequently Asked Questions

What is a credit report?

A credit report contains a detailed list of information regarding your credit activity and current credit situation based on information such as the status of your accounts, as well as your ability to pay debt, such as outstanding loans and mortgages.

When you make payments on your various types of loans and debt such as mortgages, auto loans, HELOC’s, and credit card payments, it is all recorded by the businesses providing the loans. These lenders will report your payment habits, debts, loan, and credit history to 1 or more of the 3 main credit reporting agencies or bureaus.

The credit reporting companies collect and combine all information regarding your credit and payment activities into a credit report. Since information is not received by all reporting agencies, credit reports can differ from one agency to another.

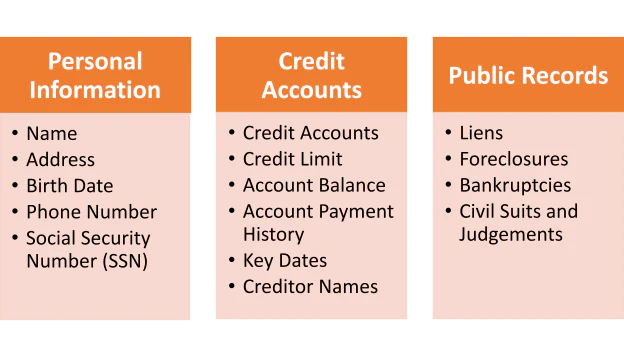

What information is provided in my free credit report?

- Personal Information - The list includes basic information required to ensure that the credit report is for you and the correct information.

- Credit Accounts – This is a major portion of the report, it will include all your credit accounts such as mortgages, personal loans, and revolving lines of credit. Along with the accounts, it will also include the credit limit, balance, payment history, and the dates the accounts were opened and closed.

- Public Records – This section contains some of the negative information regarding your credit such as previous delinquencies, bankruptcies, and civil suits. Information regarding a lawsuit can stay on your report for 7 years or until the statute of limitations runs out. Bankruptcies can be kept for 10 years and unpaid taxes will stay for 15 years.

What is a credit score?

A credit score is a numerical value associated with your creditworthiness or your ability to pay back debtors and lenders. It is calculated by a mathematical formula that uses the information provided in your credit report.

Credit scores are used by lenders to determine the likelihood of repayment. Individuals with higher credit scores are more likely to pay back, versus individuals with a lower credit score who are less likely to pay back their debts.

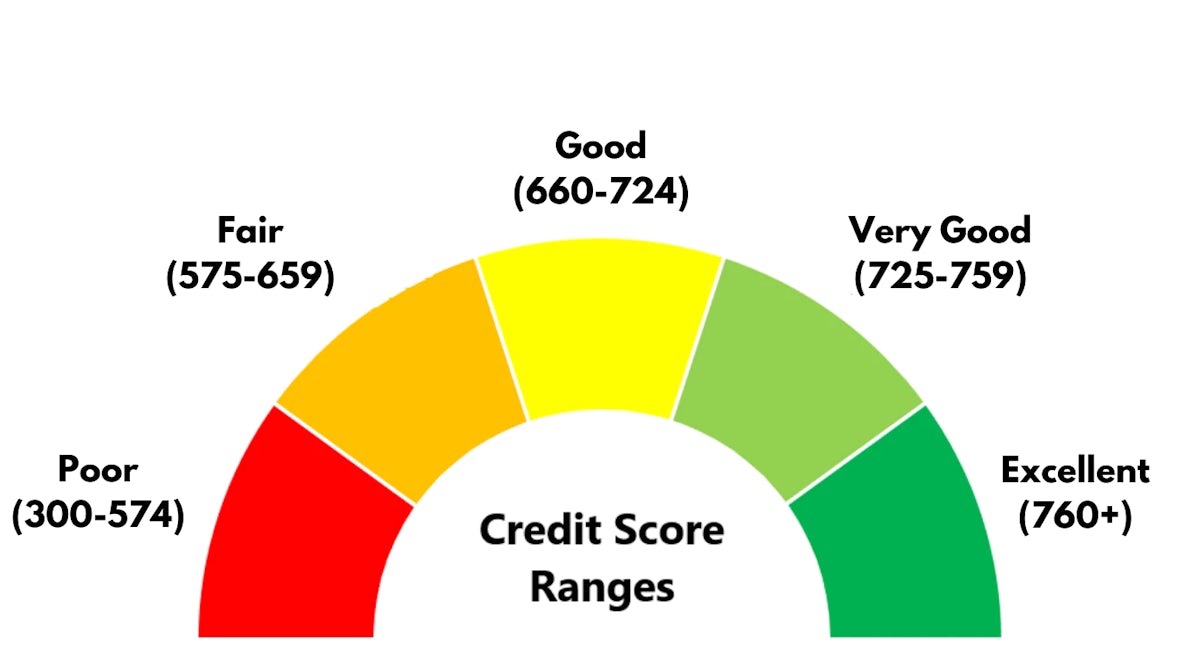

The above figure shows how credit scores are interpreted. An excellent credit score is above 760 where you can qualify for all financial products and will get the best rate. A credit score above 660 is a good score, and you will have access to most products. Borrowers with a credit score below 660 will have room for improvement, however, they may still qualify for most conventional mortgage programs that have a minimum credit score requirement of 620.

If you have a low credit score that is at least 500, you should consider an FHA loan which is catered to individuals with a lower credit score. Other options include VA loans and USDA loans that do not have minimum credit score requirements.

Why does my credit score differ between agencies?

The 3 main credit reporting agencies determine your credit score, however, they can differ from each other because of several reasons:

- Altered Mathematical Formula: The formula that one agency used might differ significantly from what another agency uses. Therefore, it is completely okay if your credit score varies from agency to agency, as long as they are in the same ballpark or range you should be good.

- Varied Scales: Different agencies have different credit score scales. For example, TransUnion and Experian have a scale from 300 – 850, whereas Equifax has a scale from 280 – 850.

- Limited Reporting: Not all lenders report to all 3 agencies, therefore, some of the credit payments might be missing from one of the agencies which can affect the entire report and credit score.

Why doesn’t my free credit report include my credit score?

It is important to understand that there is a difference between your credit report and your credit score. A credit report is a compilation of your credit information that the credit bureau receives, while a credit score is the value calculated based on a formula using the information from your credit report.

You can have multiple credit scores as a result of the manner in which credit scores are calculated. You can always analyze your free credit report as the law states that you can receive 1 free credit report from each of the 3 national agencies every year.

Is it important to check your credit report regularly?

Yes, credit score is a very important factor that is considered when lenders are analyzing your financial ability to repay debt. The credit report is used to calculate the credit score. A lot of financial products’ first requirement is a minimum credit score, for example, conventional mortgages require a minimum credit score of at least 620.

Next, your credit report includes all the positive and negative factors affecting your credit score. You should pay close attention to the negative factors on your credit report to see what you should improve on, whether that’s keeping your credit utilization rate low or making sure to make your payments on-time.

Lastly, it is essential to check your report to ensure all the information being reported is accurate and up to date as it can be a huge hassle to change information on your report in the future. It is also a good habit to ensure no fraudulent activity is taking place using your name and financial information.

How do I fix errors in my credit report?

If you are denied credit or certain financial products as a result of your credit report, you are allowed to request which agency provided your credit report. You can request a free credit report from that credit bureau within 60 days of the negative credit decision. There are two major ways to fix inaccuracies on your credit report:

- Get in touch and contact the credit reporting bureau and the company that provided the wrong information such as banks or lenders.

- Reach out to the credit reporting bureau and state what is wrong and why it is wrong. Keep a copy of all communication and exchanges that you make.

- Use credit improvement agencies for rapid rescoring.

The credit reporting agency and lender are responsible for fixing the errors on your credit report. If your written dispute is met with negligence or inaction, you can reach out to the Consumer Financial Protection Bureau (CFPB) and file a complaint.

Can I get my free credit report annually?

Yes, you can get a free credit report annually from the 3 main agencies once a year.

Does checking your free credit report hurt your credit?

No, checking your credit report has no impact on your credit as it is considered a ‘soft’ inquiry. Only ‘hard’ inquiries negatively affect your credit score. For example, a mortgage lender checking your full financial history and credit would be considered a ‘hard’ inquiry, and it can lower your credit for a short period of time. If several lenders check within a certain time, such as all within 60 days, then it only impacts your credit once. Having many hard inquiries in a short period of time on your credit report can be a red flag to lenders, as it may signal that you are desperate for credit.

How long does it take to get a free credit report?

If you use annualcreditreport.com which is the official legally mandated website, you can receive it immediately. If you order it by phone, it can take 15 days to reach your home.

Who can access my credit report?

The Federal Credit Reporting Act specifies who can access your credit reports. Creditors, lenders, insurers, employers, and businesses that require the credit information can access your credit report.

Can my employer access my credit report?

Yes, but only if you authorize access to the report. Credit bureaus are not allowed to provide your credit report to employers or potential employers without your approval.

Credit Privacy Numbers (CPNs)

A credit privacy number (CPN) is a number similar to a Social Security number (SSN) that people buy. People might buy a CPN in order to hide their real SSN, such as if they want to protect their SSN. However, some might use a CPN to apply for credit in order to hide their bad credit history. Using a CPN to apply for credit is illegal.

Credit Score Statistics

Average Credit Score by State - Map

| State | Average Credit Score |

|---|---|

| Alabama | 691 |

| Alaska | 717 |

| Arizona | 710 |

| Arkansas | 694 |

| California | 721 |

| Colorado | 728 |

| Connecticut | 728 |

| Delaware | 714 |

| District of Columbia | 717 |

| Florida | 706 |

| Georgia | 693 |

| Hawaii | 732 |

| Idaho | 725 |

| Illinois | 719 |

| Indiana | 712 |

| Iowa | 729 |

| Kansas | 721 |

| Kentucky | 702 |

| Louisiana | 689 |

| Maine | 727 |

| Maryland | 716 |

| Massachusetts | 732 |

| Michigan | 719 |

| Minnesota | 742 |

| Mississippi | 681 |

| Missouri | 711 |

| Montana | 730 |

| Nebraska | 731 |

| Nevada | 701 |

| New Hampshire | 734 |

| New Jersey | 725 |

| New Mexico | 699 |

| New York | 722 |

| North Carolina | 707 |

| North Dakota | 733 |

| Ohio | 715 |

| Oklahoma | 692 |

| Oregon | 731 |

| Pennsylvania | 723 |

| Rhode Island | 723 |

| South Carolina | 693 |

| South Dakota | 733 |

| Tennessee | 701 |

| Texas | 692 |

| Utah | 727 |

| Vermont | 736 |

| Virginia | 721 |

| Washington | 734 |

| West Virginia | 699 |

| Wisconsin | 735 |

| Wyoming | 722 |

Source: Experian (2021)

Which States Have the Best and Worst Credit Scores?

According to Experian, Minnesota had the highest average credit score in 2021, with an average FICO Score of 742. The five states with the highest average credit scores are:

- Minnesota - 742

- Vermont - 736

- Wisconsin - 735

- New Hampshire - 734

- Washington - 734

Mississippi was the state with the lowest average credit score in 2021, with an average credit score of 681. The five states with the lowest average credit scores are:

- Mississippi - 681

- Louisiana - 689

- Alabama - 691

- Oklahoma - 692

- Texas - 692

National Average Credit Score Over Time

Average Credit Score by Age

Average Credit Score by Age - Table

| Age | Average Credit Score |

|---|---|

| 18 - 24 | 679 |

| 25 - 40 | 686 |

| 41 - 56 | 705 |

| 57 - 75 | 740 |

| 76+ | 760 |

Source: Experian (2021)

Average Credit Score by Income

Average Credit Score by Income - Table

| Income | Average Credit Score |

|---|---|

| $30,000 or less | 590 |

| $30,0001 - $49,999 | 643 |

| $50,000 - $74,999 | 737 |

Source: American Express

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.