Types of Mortgage Loans

Types of Mortgage Loans

Navigating mortgage loans in the United States can be overwhelming. There are many options designed to help various financial situations and goals. Using the best mortgage loan for your unique situation when buying a home is essential. This article will demystify mortgage loans by explaining the options along with their benefits and requirements. Continue reading to learn the best type of mortgage loan for you.

Comparing Mortgage Interest Rates

Sample Lenders, September 1 2022

Conventional Loans

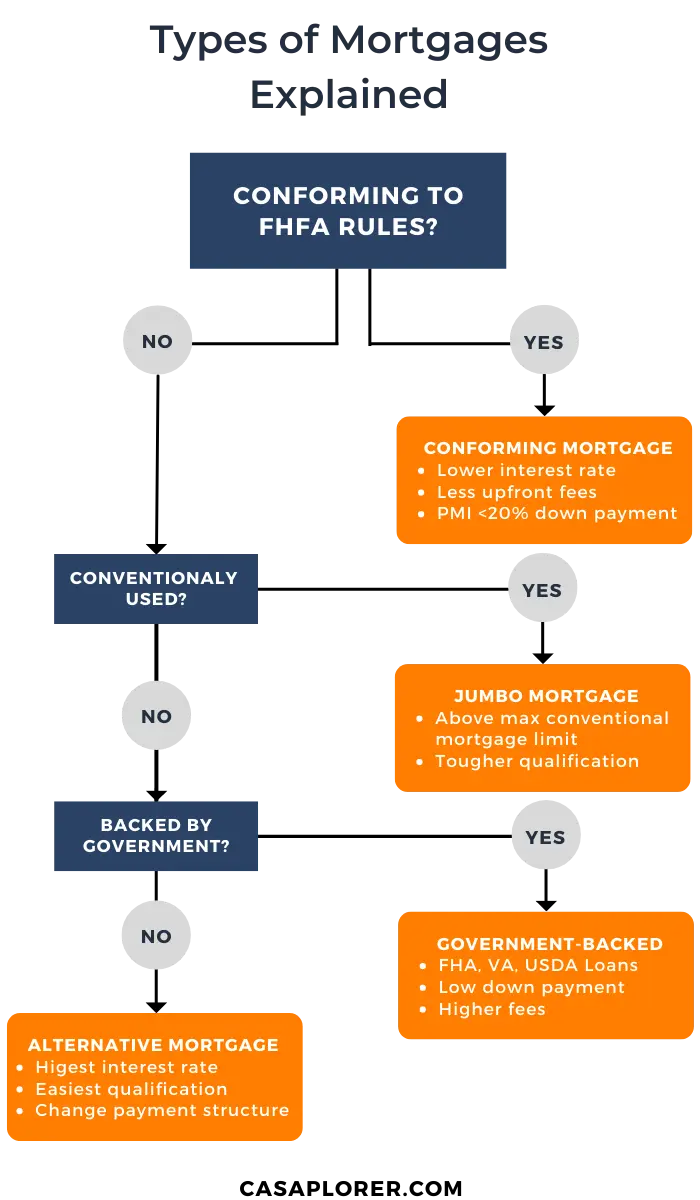

As a category, conventional loans have low interest rates and fewer upfront fees. They can be subdivided into conforming and non-conforming loans.

- A conforming loan meets Federal Housing Finance Agency's (FHFA) requirements. As a result, lenders can sell the debts to mortgage investors such as Fannie Mae or Freddie Mac.

- Non-conforming loans, such as a jumbo mortgage can’t be sold to Fannie Mae or Freddie Mac. However, they can still be sold to investors.

Conforming Mortgage

A conforming mortgage, also known as a qualified mortgage, means it meets FHFA requirements. These mortgages typically have lower interest rates but more approval requirements. The primary requirement is the maximum mortgage limit, which varies by region. If your mortgage exceeds the limit, you'll need a jumbo mortgage with a slightly higher interest rate.

To qualify for a conventional conforming mortgage, you will need to meet the following criteria;

- Mortgage below the maximum regional limit

- 20% down payment, or private mortgage insurance (PMI)

- A credit score of at least 620

- DTI (debt-to-income ratio) below 50%

Jumbo Mortgage

A jumbo mortgage is a non-conforming loan because it exceeds the maximum mortgage limit. They typically have low-interest rates due to stricter approval requirements. These mortgages can’t be sold to government-backed agencies such as Fannie Mae and Freddie Mac. However, lenders can still sell these loans to investors.

To qualify for a jumbo mortgage, you will need to meet the following criteria

- Cash reserves to make 12 months of mortgage payments

- Mortgage above the maximum regional limit

- 20-30% down payment

- A credit score of at least 700

- DTI (debt-to-income ratio) below 43%

| Loan Type | APR | Benefits | Requirements |

|---|---|---|---|

| Conforming Mortgage | 4.611% - 6.361% | Low interest rates and fewer upfront fees. |

|

| Jumbo Mortgage | 4.789% - 5.560% | Low interest rates for expensive homes. |

|

| FHA Loan | 6.308% - 7.072% | Low down payment with competitive interest rate. |

|

| VA Loan | 5.206% - 6.265% | Low interest rate and no down payment for veterans. |

|

| USDA Loan | N/A | Ability for rural residents with a low to moderate income to buy homes without a down payment. |

|

| Alternative Mortgages | Highest | Ability to change payment structure. | Varying |

Government-Backed Loans

Government-backed loans also fall under the category of non-conforming loans. As a result, lenders can't resell the debt. These loans are designed to make homeownership more accessible and easier to qualify for. The government agency will back the loan in the event of default. Therefore there is no risk to the lender.

Government-backed loans have the lowest interest rates but come with various fees. These fees may undercut the lower rate and cost you more than a conventional loan. There are three types of government-backed loans.

FHA Loan

A Federal Housing Administration (FHA) loan is known for providing competitive interest rates with a low down payment. They are an excellent option for potential homeowners who can't afford a 20% down payment. You can qualify for an FHA loan with a minimum down payment of 3.5%. However, you must pay additional mortgage insurance premiums.

To qualify for an FHA loan, you will need to meet the following criteria

- A credit score of at least 580 with a 3.5% down payment

- Or a credit score of at least 500 with a 10% down payment

- DTI (debt-to-income ratio) below 43%

VA Loan

A Veterans Affairs (VA) loan allows veterans to buy homes with a 0% down payment and low interest rate. These loans are available to any veteran with "good" credit. You can also use a VA loan to buy a home without a down payment or improve your existing home. The catch is that you'll need to pay a funding fee, which can be rolled into the loan amount.

To qualify for a VA loan, you will need to meet the following criteria:

- Served at least 90 consecutive days during wartime

- Or served at least 181 days during peacetime

- A credit score of at least 620

- DTI (debt-to-income ratio) below 41%

USDA Loan

The U.S. Department of Agriculture (USDA) loan is designed for rural homeowners with low to moderate incomes. These loans can be used to buy, build, or improve a home in a rural area.

To qualify for a USDA loan, you typically will need to meet the following criteria

- DTI (debt-to-income ratio) below 41%

- Earn a household income below 115% the national median

- Purchase a home in a designated rural area (population below 20,000)

Loan Options

You can alter the five previously mentioned mortgages with the following loan options. Most lenders allow you to select between the interest rate and term length. This section will further explain your options after deciding which one of the five loans is best for you.

| Fixed vs. ARM | Mortgage Insurance | Term Length | |

|---|---|---|---|

| Conforming Mortgage | Fixed or ARM | PMI with down payments below 20% | Typically 10 to 30 years |

| Jumbo Mortgage | Fixed or ARM | PMI with down payments below 20% | Typically 15 or 30 years |

| FHA Loan | Fixed or ARM |

| 15 or 30 years |

| VA Loan | Fixed or ARM |

| Typically 15 or 30 years |

| USDA Loan | Fixed |

| 30-year only |

Fixed Rate vs. Adjustable Rate Mortgage (ARM)

Your interest rate decides the amount of interest you pay over your loan term. A fixed interest rate will never change. You will have predictable payments, and your monthly mortgage payment will stay the same. However, an ARM may be a good option if you plan on selling your home before the interest rate adjusts.

An adjustable-rate mortgage (ARM) has an introductory fixed period with a lower interest rate that will eventually increase or "adjust." The initial interest rate is usually lower than a fixed-rate mortgage. However, once the introductory period ends, your interest rate will be higher than a comparable fixed-rate mortgage. As a result, your monthly mortgage payments will be lower at first but will likely increase after the fixed period ends.

Note that some mortgage options can only be fixed-rate. As an example, USDA loans can only have a fixed interest rate.

Mortgage Insurance

Mortgage Insurance If you put less than 20% down on your home, you'll need to pay for mortgage insurance. This is to protect your lender if you stop making payments on your loan. There are two types of mortgage insurance; private mortgage insurance (PMI) and government-sponsored mortgage insurance. You can cancel PMI when you reach 20% equity in your home.

Your type of mortgage will affect your mortgage insurance.

- Conventional Loans: The size of your down payment will affect the cost of PMI. The larger your down payment is, the lower your monthly mortgage insurance payments will be.

- FHA Loan: An upfront mortgage insurance premium (MIP) and a monthly MIP. The upfront MIP is 1.75% of the loan amount and can be rolled into the loan. The monthly MIP is 0.45% to 1.05%, depending on the loan term, loan amount, and down payment. You can get rid of the monthly MIP after 11 years if you put at least 10% down on your home.

- VA Loan: There is an upfront funding fee of 2.15% to 3.3% of the loan amount. The funding fee can be rolled into the loan. You will also pay an annual premium of 0.5% of the outstanding loan balance. The funding fee and yearly premium are much lower if you're a disabled veteran or qualifying spouse.

- USDA Loan: While there is no mortgage insurance, you will need to pay an upfront guarantee fee of 1% to 3% of the loan amount. The guarantee fee can be rolled into the loan. You will also pay an annual premium of 0.35% of the outstanding loan balance.

Loan Term Length

The term length is how long you have to pay back your mortgage. The most common term lengths are 30 years and 15 years. However, some lenders offer 10-year, 20-year, and 40-year mortgage terms. Your type of mortgage may also restrict you to certain lengths. For example, a USDA loan can only have a 30-year term.

A shorter loan means higher monthly payments, but you'll pay off your home faster and less in interest overall. A longer loan term means lower monthly payments, but you'll pay more in interest over the life of the loan.

You may be able to refinance your mortgage to a different term length. For example, you may have initially chosen a 30-year term. But after a few years, you may want to refinance to a 15-year term to pay off your home faster.

Alternative Mortgages

Aside from the five more common loans discussed above, some borrowers may prefer alternative mortgages. Otherwise known as non-QM loans, these are typically offered by portfolio lenders and are non-conforming due to their unique features. Some lenders may even let borrowers roll fees into a no-closing cost mortgage. Borrowers select these options if they prefer the features or can't qualify for a standard mortgage. However, these loans are riskier to lenders and always have a higher interest rate. This section will discuss the possibilities of alternative mortgages and why you may want one.

| Name | Description |

|---|---|

| Debt-Service Coverage Ratio (DSCR) Loan | Typically used for investment properties. Allows you to qualify for a mortgage based on your future rental income. |

| Piggyback Loan | A second mortgage used in combination with a first mortgage and allows you to avoid paying private mortgage insurance (PMI). |

| Interest Only | Allows you to make smaller, interest-only payments each month. You'll need to pay back the initial principal borrowed at the end of your term. |

| Balloon Mortgage | While this varies by lender, you'll avoid monthly payments and make a final lump sum payment at the end of your term. It's best matched with the BRRRR method. |

| Construction Loan | Allows you to finance building a home. This loan provides you with more funding every time you accomplish a predetermined milestone. You must pay back the principal and interest at the end of your term. |

| Reverse Mortgages | For retiring homeowners with sufficient home equity. Borrow against your home and only repay when you move. |

| Chattel Mortgages | Ability to finance the purchase of transportable homes. Typically used for mobile homes, modular homes, and vehicles. |

| Assumable Mortgages | The home seller can transfer their existing mortgage to the new buyer. |

| Private Mortgages | Used when additional options aren't available. Require larger down payments with higher interest rates. |

| Hard Money Loans | Short-term loans with a high interest rate. |

| Blanket Mortgages | Bundle multiple properties under one mortgage to reduce closing costs. |

| Fix and Flip Loans | A category of loans designed to help real estate investors with flipping property. |

| Commercial Construction Loan | Allows businesses to finance the cost of building real estate. |

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.