Balloon Mortgage

CASAPLORER®Trusted & TransparentA balloon mortgage resembles a regular mortgage in all the aspects besides the payment structure that the borrower follows to pay back the mortgage. As the name suggests, with a balloon mortgage, the borrower has to make a lump sum payment or balloon payment at some point during the mortgage term. Meanwhile, with a regular mortgage, the borrower pays off the mortgage completely throughout the term by making monthly mortgage payments.

What You Should Know

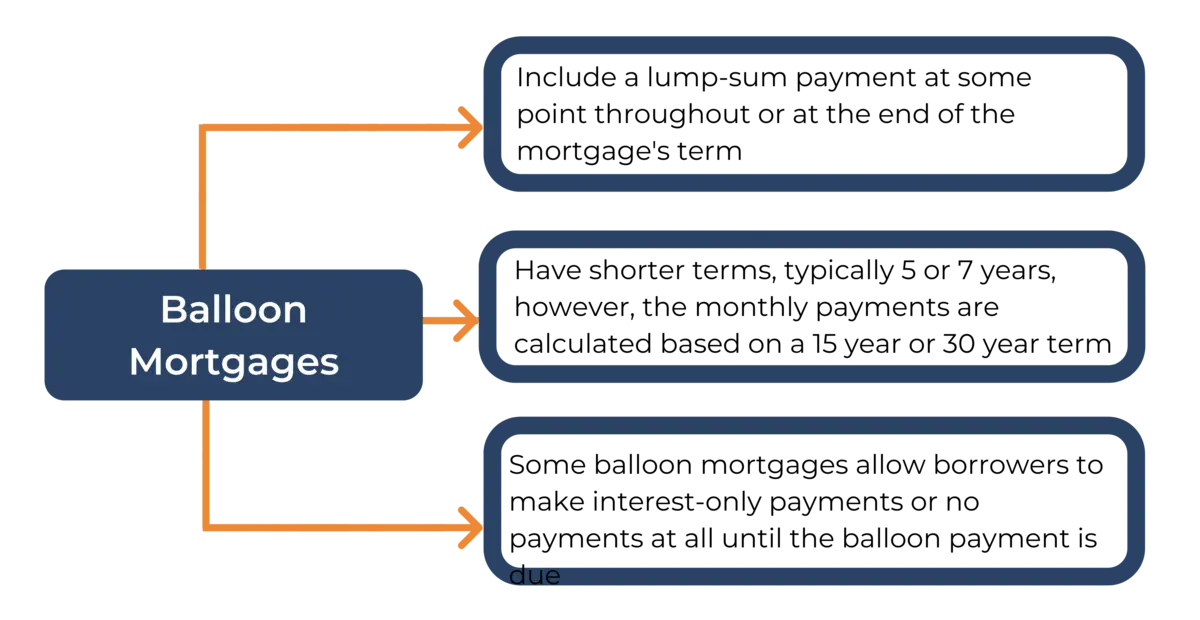

- With a balloon mortgage, the borrower has to make a lump sum payment at some point during or at the end of the mortgage term to pay it off

- Some balloon mortgages may come with principal and interest payments, interest-only payments or no payments at all until the balloon payment is due

- Balloon mortgages usually have fixed mortgage rates

- There are typically no prepayment penalties if you wish to pay off some of the principal during the term of the mortgage

What is a Balloon Mortgage?

A balloon mortgage is a type of home loan where the borrower makes fixed monthly payments throughout the term of the loan and there is a lump sum payment that must be paid at some point throughout the term. Generally, this lump sum is paid at the end and it serves to pay off the remaining principal balance owed. Balloon mortgages come in shorter terms, usually 5 and 7 years, however, the payments are calculated based on a term of 30 years. This means that the monthly mortgage payments will be lower but the borrower will have to face the balloon payment at some point.

The main obvious downside of balloon mortgages is that you would have to save in order to be able to make the balloon payment at the end of your loan. Some balloon mortgages can also have the lump-sum payment half-way in the loan’s term.

How do Balloon Mortgages Work?

There are different types of balloon mortgages. For some of them, you can make interest-only payments throughout the term and then pay the principal balance in full at the end. Others allow you to make interest and principal payments, however, these would be lower than in regular mortgages. In turn, the balloon payment would also be lower since you will be paying off some of the principal with the periodic payments. Mortgages with balloon payments are rarely offered to consumers. Instead, they are often used in construction loans, commercial mortgages, or in bridge loans. You can use the commercial loan calculator to estimate your balloon payment on your mortgage.

There are different types of balloon mortgages in terms of how and when the principal, interest and the lump-sum is paid. These include:

- Balloon Payment -This is the most common type of balloon mortgage, where your monthly mortgage payment is calculated normally as if the loan has a 15-year or 30-year term. However, instead of paying it for this long, you will have to make a balloon payment in 5 or 7 years to cover the remaining amount owed.

- Interest-only repayments -Some balloon mortgages allow borrowers to pay only interest on their mortgage throughout the term. At the end of the term, the borrower will need to make one balloon payment equivalent to the original principal balance. These loans are more common in commercial real estate.

- No monthly payments -Other balloon mortgages do not require to pay neither interest nor principal throughout the mortgage’s term. With these types of mortgages, the borrower would have to pay the whole amount borrowed and the interest accumulated at the end of the term. The term is typically one year.

Example

You want to purchase a house worth $250,000 through a balloon mortgage with a 7 year term and a 3% interest rate. You will have to make a monthly mortgage payment of $1,054 for 7 years. At the end of the term, or after 7 years, you have to make a balloon payment of $209,955.

Payment Schedule of a Balloon Mortgage

We will start off by showing the typical payment schedule of a balloon mortgage where the borrower makes principal and interest payments. Let’s say that you take out a mortgage of $350,000 with an interest rate of 3% and a balloon payment scheduled in 10 years. The payment schedule would look something like this:

| Month | Principal | Interest | Payment | Ending Balance |

|---|---|---|---|---|

| 1 | $600.61 | $875.00 | $1,476 | $350,000.00 |

| 2 | $602.12 | $873.50 | $1,476 | $349,399.39 |

| 3 | $603.62 | $871.99 | $1,476 | $348,797.27 |

| 4 | $605.13 | $870.48 | $1,476 | $348,193.65 |

| 5 | $606.64 | $868.97 | $1,476 | $347,588.52 |

| 6 | $608.16 | $867.45 | $1,476 | $346,981.88 |

| 7 | $609.68 | $865.93 | $1,476 | $346,373.72 |

| 8 | $611.20 | $864.41 | $1,476 | $345,764.04 |

| 9 | $612.73 | $862.88 | $1,476 | $345,152.83 |

| 10 | $614.26 | $861.35 | $1,476 | $344,540.10 |

| 108 | $784.56 | $691.06 | $1,476 | $276,422.97 |

| 109 | $786.52 | $689.10 | $1,476 | $275,638.41 |

| 110 | $788.48 | $687.13 | $1,476 | $274,851.89 |

| 111 | $790.46 | $685.16 | $1,476 | $274,063.41 |

| 112 | $792.43 | $683.18 | $1,476 | $273,272.95 |

| 113 | $794.41 | $681.20 | $1,476 | $272,480.52 |

| 114 | $796.40 | $679.22 | $1,476 | $271,686.11 |

| 115 | $798.39 | $677.22 | $1,476 | $270,889.71 |

| 116 | $800.39 | $675.23 | $1,476 | $270,091.32 |

| 117 | $802.39 | $673.23 | $1,476 | $269,290.93 |

| 118 | $804.39 | $674.22 | $1,476 | $268,488.55 |

| 119 | $806.40 | $669.21 | $1,476 | $267,648.15 |

| 120 | $808.42 | $667.19 | $1,476 | $266,877.75 |

With a balloon mortgage, you would have to make a lump-sum payment at the end of the term. In this case the lump-sum you would owe is $266,877.75. As you can see, this is still a pretty large amount of money to come up with even if you have been paying off the mortgage for 10 years. In order to avoid having to come up with such a big amount, borrowers can typically make principal payments throughout the mortgage’s term without any prepayment penalties. If principal payments are made throughout the term, then you will be left with a smaller amount to pay at the end of the term.

Payment Schedule of Mortgage with Interest-only payments

Next we will explore what the payment schedule of a balloon mortgage with interest-only payments looks like. In this case, since you are not paying off any principal, you would pay the same amount in interest each month throughout the mortgage term. Taking the example of a $350,000 mortgage with a 3% interest rate, your repayment schedule will look like this:

| Month | Principal | Interest | Ending Balance |

|---|---|---|---|

| 1 | $0 | $875.00 | $350,000.00 |

| 2 | $0 | $875.00 | $350,000.00 |

| 3 | $0 | $875.00 | $350,000.00 |

| 4 | $0 | $875.00 | $350,000.00 |

| 5 | $0 | $875.00 | $350,000.00 |

| 6 | $0 | $875.00 | $350,000.00 |

| 7 | $0 | $875.00 | $350,000.00 |

| 8 | $0 | $875.00 | $350,000.00 |

| 9 | $0 | $875.00 | $350,000.00 |

| 10 | $0 | $875.00 | $350,000.00 |

| 108 | $0 | $875.00 | $350,000.00 |

| 109 | $0 | $875.00 | $350,000.00 |

| 110 | $0 | $875.00 | $350,000.00 |

| 111 | $0 | $875.00 | $350,000.00 |

| 112 | $0 | $875.00 | $350,000.00 |

| 113 | $0 | $875.00 | $350,000.00 |

| 114 | $0 | $875.00 | $350,000.00 |

| 115 | $0 | $875.00 | $350,000.00 |

| 116 | $0 | $875.00 | $350,000.00 |

| 117 | $0 | $875.00 | $350,000.00 |

| 118 | $0 | $875.00 | $350,000.00 |

| 119 | $0 | $875.00 | $350,000.00 |

| 120 | $0 | $875.00 | $350,000.00 |

By making interest-only payments, you would end up paying a smaller amount monthly, but a large lump-sum balloon payment at the end of the term. Since during the term, you only paid off the interest on the mortgage, your whole principal amount of $350,000 would be due at the end of the term. You can calculate your own payment schedule using an interest-only mortgage calculator.

Balloon Mortgages vs Other types of loans

The main difference between balloon mortgages and other types of loans is the lower periodic payments that balloon mortgages offer. Of course, this comes at the cost of making a huge lump-sum payment at the end or at some point during the term of the loan. Some borrowers choose balloon mortgages because it may offer them a lower interest rate or they may want to pay only interest initially. On the other hand, from the lender’s point of view, balloon mortgages present more risk than other types of loans, since there is a possibility that the borrower may not afford to make the balloon payment when it comes due.

Conventional mortgages - Compared to conventional mortgages, with a balloon mortgage, a borrower faces more uncertainty. This uncertainty relates to the amount of monthly payments they will make, the principal payments, and when the mortgage will be completely paid off. With a regular 15-year or 30-year conventional mortgage, the borrower knows that they will have to make a fixed monthly payment and the loan will be completely paid off at the end of the term.

Government-backed mortgages - FHA and USDA do not offer balloon mortgages.

Adjustable-rate mortgages - Adjustable-rate mortgages typically have a fixed interest rate for the first few years of the mortgages, and then convert to a rate that fluctuates according to an underlying rate, usually the prime rate. Balloon mortgages, on the other hand, typically come with fixed mortgage rates as their terms are shorter.

Pros and Cons of Balloon Mortgages

Balloon mortgages have certain characteristics which make them unique compared to other types of mortgages. Based on someone’s specific circumstances, they might find a balloon mortgage more fitting to their financial needs. However, it is always useful to evaluate the pros and cons that this mortgage represents before making a final decision.

| Pros | Cons |

|---|---|

|

|

Pros

Lower Monthly Payment - The most obvious advantage of balloon mortgages is that you will have to make a lower monthly payment no matter which type of balloon mortgage you choose. If you take out a balloon mortgage with interest-only payments, your periodic monthly payments will consist only of interest. On the other hand, even with a balloon mortgage where you make partial principal payments, the monthly payment would still be lower considering that you will not pay off the loan fully by the end of the term.

Initially more affordable - You don’t have to make any big lump-sum payments for several years into the loan. You would only need to make your monthly mortgage payments, which, as we mentioned, will be lower than those of regular mortgages.

Build your finances - Balloon mortgages leave you some room to breath in the beginning by letting you focus on saving and building your credit score, rather than coming up with a mortgage payment that you may not always afford depending on your specific financial circumstances.

Better mortgage rates - Balloon mortgages sometimes come with better mortgage rates, which means you will end up paying less in interest throughout the term of your mortgage.

Shorter term - Balloon mortgages come in shorter terms. Therefore, if you believe that your finances will allow you to make a big lump-sum payment in a few years, you don’t have to commit 15 or 30 years to a mortgage.

Cons

Balloon Payment - The balloon payment that will be due at a certain point throughout the mortgage term or at the end of it presents a huge risk for borrowers. If they have not been able to save a considerable amount of money to make the balloon payment as it comes due, then they risk defaulting on their loan and facing foreclosure.

Risky for lenders - Not only borrowers, but lenders also face a lot of risk when giving out balloon mortgages. While a borrower may be able to afford the low monthly payments during the term, there is no guarantee that they will have the financial means to afford the balloon payment. In the case that the lender has to foreclose on your property, they will have to face the foreclosure costs and lengthy procedures.

Difficult to refinance - To refinance a mortgage, you typically need to have built up some equity in your home. With the small monthly payments that balloon mortgages offer, a borrower may end up building too little equity and may not be eligible to qualify for refinancing.

How to pay off a balloon mortgage?

In order to pay off your balloon mortgage, you have three options:

Save for the balloon payment

The riskiest aspect of a balloon mortgage is whether you will be able to afford the balloon payment when it comes due. If you cannot make the payment then you will end up defaulting on your loan and lose your home. Usually balloon mortgages are taken out by individuals who believe that they will experience a significant increase in income in the near future. This can be the case when the person expects to be promoted or is certain that they will have more seniority within a workplace in the next few years, which lets them have an idea of their income. No matter what the reason is behind taking out a balloon mortgage, it is always crucial to start saving money for the balloon payment as soon as and as much as you can. So that if something unexpected happens to your employment status or anticipated promotion, you will still have a considerable amount saved.

House flippers are another group of people who may be interested in taking out a balloon mortgage. It is sometimes easier to get a balloon mortgage if you intend to improve the condition of the property and flip it, since you will have the means to pay off the balloon payment.

Refinance the mortgage

Another way of paying off your balloon mortgage is refinancing it. Before you decide to try and refinance your balloon mortgage, you need to have a few things in mind in terms to how your mortgage terms and payments will change compared to your balloon mortgage, such as:

- Monthly Payment -If you take out a balloon mortgage that requires interest-only payments, then refinancing to a regular mortgage will significantly increase your monthly mortgage payments. The reason behind this is that you will also be making principal payments. Moreover, the mortgage will have to be completely paid off at the end of the term, which is why the periodic payments are bigger.

- Closing costs - You will need to be able to afford the closing costs associated with refinancing your balloon mortgage.

- Credit Score - To qualify for refinancing, you are required to have a minimum credit score. For conventional mortgages, this requirement is typically a score of 620. For FHA loans, on the other hand, you only need to have a credit score of 580. Therefore, if your credit is not on the right track, then you may not even be able to refinance.

- Income - Apart from the credit score, to refinance into a regular mortgage you will also need to fulfill some income and employment requirements. For instance, your DTI ratio should not exceed 43%. The DTI ratio shows the portion of your income that serves to pay your monthly debt obligations.

- Equity - The biggest issue with refinancing is that you may be required to have a certain amount of equity in your home in order to be able to refinance. With a balloon mortgage, equity builds up slowly and there’s not much you can do about it besides making a large down payment.

Sell your home

If you plan to stay in your home only for a few years, then you can sell the home in order to get the proceeds needed to make the balloon payment. If you sell before the balloon payment is due, than you can get the necessary funds to cover the large lump sum.

Should I get a balloon mortgage?

The answer to this question depends on your own financial circumstances. The most obvious risk is whether you will be able to afford the balloon payment at the end of the loan. If you are certain that you will have the means to pay it off, then a balloon mortgage has many perks, such as smaller monthly payments leaving you more flexibility with your finances.

There are a number of scenarios when it would make sense to take out a balloon mortgage. These include:

- When your credit is not good enough to take out a regular mortgage but you are certain that it will improve in the future. At this point in the future, you will be able to refinance your mortgage before having to make the balloon payment.

- When you do not plan to stay in the home for long. This can include the case where you plan to flip the house.

- When you believe that there will be a significant decrease in interest rates in the near future and you plan to refinance the mortgage when that happens.

Alternative mortgages

If you find the balloon payment of a balloon mortgage too big of a risk, then there are a number of other types of loans you can consider instead.

Adjustable-rate mortgages - As mentioned earlier, adjustable rate mortgages typically start with a fixed mortgage rate for the first few years and then the rate fluctuates. The risk of an adjustable mortgage rate is considerably smaller than having a large balloon payment at the end of the term. Moreover, this way, as a borrower, you will be able to build equity faster.

30-year fixed mortgage - With a 30-year fixed mortgage, you would have to continue making equal periodic monthly payments throughout the term of the loan. You would not have to make any balloon payment at the end of the term, since the whole mortgage will be paid off until then. If at any point you decide to make a payment towards your principal, you still can. However, you may face prepayment penalties.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.