Debt-Service Coverage Ratio (DSCR) Loans: Getting a No-Income Verification Mortgage

What You Should Know

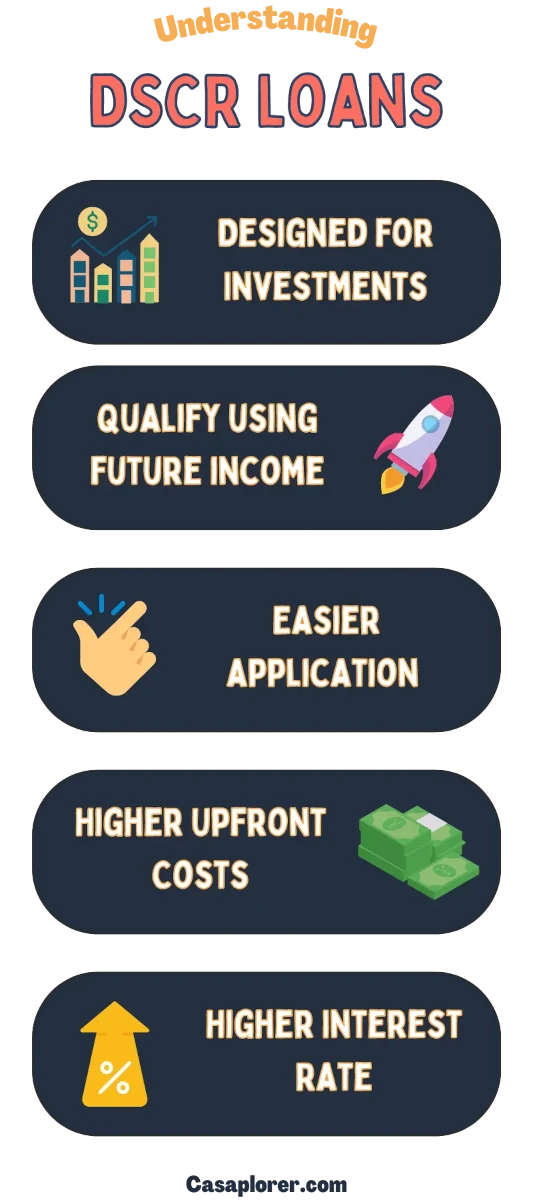

- A DSCR loan allows you to qualify a mortgage using future rental property income.

- The interest rate is typically 3% to 5% higher than conventional loans.

- You will need a minimum 20% down payment.

- Most lenders also want to see a six-month reserve fund.

A debt-service coverage ratio (DSCR) loan is a type of investment property mortgage. The loan allows borrowers to receive funding without needing to prove their income. Instead, borrowers can qualify for the mortgage using the future income they will receive from the rental acquisition of interest. This article will thoroughly explain DSCR loans, how to get one, compare it with conventional loans, and more. Continue reading to become an expert in DSCR loans.

DSCR Loan Explained

A DSCR loan is a non-QM loan, which is a non-qualified mortgage. These types of mortgages are for buyers who don't fit the standard criteria lenders use to approve a mortgage. Conventional lenders typically require thorough proof of income, including tax returns and banking statements. Instead, DSCR loans allow borrowers to qualify using future income and credit score history.

The main benefit of a DSCR loan is that it's easier to qualify for this mortgage than a conventional one. To qualify for a DSCR loan, you'll need a solid debt service ratio and prove that the rental property can generate enough income to cover the mortgage payments. The lender will also look at your credit score and history to determine if you're a good candidate for the loan.

It's important to note that DSCR loans come with higher interest rates than conventional loans. This is because they're considered to be a higher risk by lenders.

| Pros | Cons |

|---|---|

|

|

Calculating Your Debt-Service Coverage Ratio (DSCR)

Lenders will calculate your debt-service coverage ratio (DSCR) to qualify you for a loan. This calculation includes your net operating income (NOI) and annual debt service. Lenders will then divide the property's NOI by your debt service to calculate your DSCR.

Lenders use this to calculate if your property generates enough profits to make debt payments with a safety margin. Most lenders look for a minimum DSCR of 1.25x, meaning you profit 1.25x your annual debt payments. Some lenders may enable a lower DSCR but they will charge a higher interest rate and potentially require a more significant down payment.

Lenders believe your personal income shouldn't matter if the property is sufficiently profitable. The following section explains how to calculate your DSCR.

Step One: Annual Net Operating Income (NOI)

Your net operating income (NOI) is the total revenue generated by the property minus operating expenses. These expenses can include, but are not limited to:

- Mortgage payments

- Property taxes

- Insurance

- Maintenance and repairs

- Utilities

To calculate your NOI, take your total revenue and subtract your operating expenses. For example: Let's say you generate $30,000 in revenue from your rental property each year. After deducting $10,000 in operating expenses, your NOI would be $20,000.

Step Two: Annual Debt Service

Your annual debt service is the total amount you'll need to pay towards the mortgage each year. This includes the principal, interest, taxes, and insurance (PITI). To calculate your annual debt service, take your monthly mortgage payment and multiply it by 12. For example: If your monthly mortgage payment is $1,000, your annual debt service would be $12,000.

Step Three: Divide NOI by Debt Service

Now that we've gone over how to calculate both the NOI and debt service, we can finally calculate the DSCR. To do this, take your NOI and divide it by your annual debt service. For example: If your NOI is $20,000 and your annual debt service is $12,000, your DSCR would be 1.67x.

This calculation is necessary because it tells lenders how much profits your property generates compared to the amount you'll need to pay towards the mortgage each year. Most lenders typically require a ratio of 1.25x or higher to qualify for a DSCR loan. Lenders prefer a higher percentage because it shows you have excess ability to make debt payments.

DSCR Loan Requirements

| Criteria | Requirement |

|---|---|

| Down Payment | Minimum 20% |

| Property Type | Investment property |

| Credit Score | Minimum 640 |

| DSCR Ratio | Typically above 1.25x |

| Reserve Fund | Typically 6x monthly debt service |

While a DSCR loan has a more straightforward application process, there are still funding requirements. This section will dive into the criteria to help you qualify for a loan.

Down Payment

The down payment for a DSCR loan is typically 20% of the purchase price or appraised value, whichever is higher. This is higher than most QM loans, such as an FHA, VA, or USDA. These options have minimum down payments ranging from 0% to 3.5%. The higher down payment requirement is because a DSCR loan is riskier to lenders.

Property Type

DSCR loans can only be used to finance investment properties such as:

- Single-family homes

- Multi-family homes

- Condo units

- Townhomes

There are a few reasons why lenders only finance investment properties with DSCR loans. The first reason is that these loans are already considered high risk. Lenders want to minimize their risk by only lending to borrowers who they feel have the ability to repay the loan. The second reason is that investment properties generate income. This income can be used to repay the loan if the borrower cannot do so.

Credit Score

While there is no minimum credit score requirement for a DSCR loan, most lenders prefer borrowers to have a credit score of 640 or higher. This is because borrowers with a higher credit score are considered to be less of a risk. If you have a lower credit score, you may still be able to qualify for a DSCR loan. However, you may be required to put down a larger down payment or pay a higher interest rate.

DSCR Ratio

As mentioned earlier, most lenders require a minimum DSCR ratio of 1.25x. Your property must generate enough income to cover 125% of the monthly mortgage payments and other property-related expenses. For example: If your annual debt service was $12,000, you would need to generate at least $15,000 in NOI.

Reserve Fund

In addition to the down payment, most lenders require you to have a reserve fund. A reserve fund is money set aside in case of an emergency. For example, if your property needs repairs or you lose a tenant, you can use the reserve fund to cover these expenses. Most lenders require a reserve fund equal to six months of mortgage payments. So, if your monthly debt service is $1,000, your reserve fund would need to be $6,000.

DSCR Loan Interest Rates

The interest rate for a DSCR loan is typically higher than the interest rate for a conventional mortgage. This is because DSCR loans are considered to be high risk. The average interest rate for a DSCR loan is between 7% and 10%. However, your interest rate will depend on factors such as your credit score, the type of property you're financing, and the lender you're working with. Comparing interest rates from multiple lenders is essential before choosing a loan. This will help you ensure that you're getting the best deal possible.

DSCR loans are riskier to lenders because they are a type of non-QM loan. Non-QM loans are mortgages that don't meet the standards set by government-sponsored enterprises (GSEs). While non-QM loans used to be very rare, they're becoming more popular. This is because the Qualified Mortgage (QM) rule has made it harder for some borrowers to qualify for a mortgage. The QM rule is a set of guidelines that lenders must follow when approving a mortgage. These guidelines include the borrower's income, debts, and credit score.

The QM rule was established to protect borrowers from taking on loans they couldn't afford. However, it has also made it harder for some borrowers to qualify for a mortgage. If you don't meet the standards set by the QM rule, you may still be able to qualify for a non-QM loan. Non-QM loans have different requirements than QM loans. For example, some non-QM loans don't require borrowers to have a minimum credit score. This makes them a good option for borrowers with bad credit.

Non-QM loans are typically available through portfolio lenders. Portfolio lenders are banks or other financial institutions that hold on to their origin loans. They don't sell them to the secondary market. This means that portfolio lenders can make their own rules when approving a loan.

DSCR Loan vs. Conventional Loan

The DSCR loan is a type of mortgage that is designed for investors. While the qualification process is simple, you will have a higher interest rate and down payment requirement. Conventional loans have stricter qualification criteria in exchange for more favorable lending terms. Conventional loans are typically for homeowners and not real estate investors.

| DSCR Loan | Conventional Loan | |

|---|---|---|

| Interest Rate | Higher | Lower |

| Lending Requirements |

|

|

| Documentation Requirements | Less | More |

Interest Rate

The interest rate for a DSCR loan is typically 3% to 5% higher than the interest rate for a conventional mortgage. For example, if the average interest rate for a DSCR loan is around 7% to 10%, a conventional mortgage would range around 4% to 5%.

Lending Requirements

| DSCR Loan | Conventional Loan | |

|---|---|---|

| DSCR Ratio | Minimum DSCR ratio of 1.25x | Maximum debt-to-income ratio of 50% |

| Down Payment | Minimum 20% down payment | Minimum 3% to 20% down payment |

| Credit Score | Minimum credit score of 640 | Minimum credit score of 620 |

| Reserve Fund | Six-month reserve fund | No reserve fund requirements |

Documentation Requirements

DSCR loans are more straightforward because they require less documentation. For example, a conventional loan requires sufficient proof of income. This proof is used to calculate your debt-to-income (DTI) ratio. The documentation typically includes some or all of the following:

- Payment stubs

- Banking statements

- Tax returns

- etc.

In comparison, a DSCR loan doesn't need this information.

Overall, the DSCR loan is a good option for experienced investors who want to invest in an income-producing property and have the money for a 20% down payment.

How to Improve Your DSCR Ratio

If you're having difficulty receiving a DSCR loan, this section will discuss ways to improve your forecasted ratio. This will help you qualify for the loan.

Decrease Your Mortgage Interest Rate

The first way to improve your DSCR ratio is to get a lower interest rate on your mortgage. A lower interest rate will decrease the amount you need to pay towards your mortgage each month. This will increase your NOI, which will, in turn, increase your DSCR ratio. Additionally, it will decrease your annual debt service. As a result, a lower mortgage rate will benefit the numerator and denominator of the ratio.

There are a few ways to get a lower interest rate on your mortgage. Lenders will reward you with a lower interest rate if they believe you're a low-risk borrower. One way to prove this is by having a high credit score. You can also make a larger down payment to decrease your interest rate.

Another way to get a lower interest rate is to shop around. Different lenders offer different interest rates. You can use a mortgage broker to help you compare rates from different lenders. This is especially effective if you have a good relationship with your lender and always make your payments on time.

Make a Larger Down Payment

As mentioned, making a larger down payment will help you get a lower interest rate on your mortgage. This will help improve your DSCR ratio.

A larger down payment will also decrease the amount you need to borrow. This will lower your monthly mortgage payments and your annual debt service. As a result, a larger down payment will also benefit the numerator and denominator of your ratio.

For example: If you're looking to purchase a $100,000 property, you would need to borrow $80,000 if you made a 20% down payment. However, if you made a 30% down payment, you would only need to borrow $70,000.

Remember that you'll need a reserve fund equal to six months of mortgage payments. So, if your monthly mortgage payment is $1,000, your reserve fund would need to be $6,000.

Extend Your Loan Term

Another way to improve your DSCR ratio is to get a longer loan term. A longer loan term will decrease your monthly mortgage payments. This will increase your NOI and reduce your annual debt service. As a result, a longer loan term will benefit the numerator and denominator of your ratio.

For example: If you're looking to purchase a $100,000 property and qualify for a 30-year loan, your monthly mortgage payment would be $377. However, if you only qualify for a 15-year loan, your monthly mortgage payment would be $693.

Getting a Loan if Your DSCR is Too Low

If your DSCR is too low, you can consider a few options.

The first option is to look for a different type of loan. Other types of loans available may be more flexible with their requirements. Another option is to find a cosigner or guarantor for the loan. This person agrees to make the loan payments if you cannot do so.

You can also try to negotiate with the lender. Explain your financial situation and why you believe you'll be able to make the payments on time. The lender may be willing to work with you to find a solution.

Finally, you can try to increase the NOI of the property. This can be done by increasing the rent or finding ways to decrease the operating expenses. Talk to your lender to see what may be the best option for you. These are just a few options to consider if your DSCR is too low.

The Bottom Line

Overall, a DSCR loan simplifies the real estate investment process by removing proof of income requirements. Instead, investors can qualify for a loan using the future property income. In exchange for simplicity, borrowers must pay a larger down payment and interest rate. Most lenders also require a minimum DSCR of 1.25x. This means your annual NOI exceeds 1.25x your yearly debt service.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.