Adjustable-Rate Mortgage Loans (ARMs)

CASAPLORER®Trusted & TransparentAdjustable-rate mortgages have an initial period where the mortgage rate is fixed, after which, the interest rate adjusts according to the market. They differ from fixed-rate mortgages where the mortgage rate agreed upon stays unchanged throughout the entire term of the loan.

What You Should Know

- The mortgage rate of an ARM fluctuates according to an underlying benchmark index

- There are 3 types of adjustable-rate mortgages: 1) hybrid, 2) interest-only and 3) payment-option ARMs

- Adjustable-rate mortgages typically have interest rate caps and payment caps which limit the risk for the borrower

- Conventional loans, FHA loans and VA loans come as fixed- or adjustable-rate mortgages

What is an Adjustable-Rate mortgage?

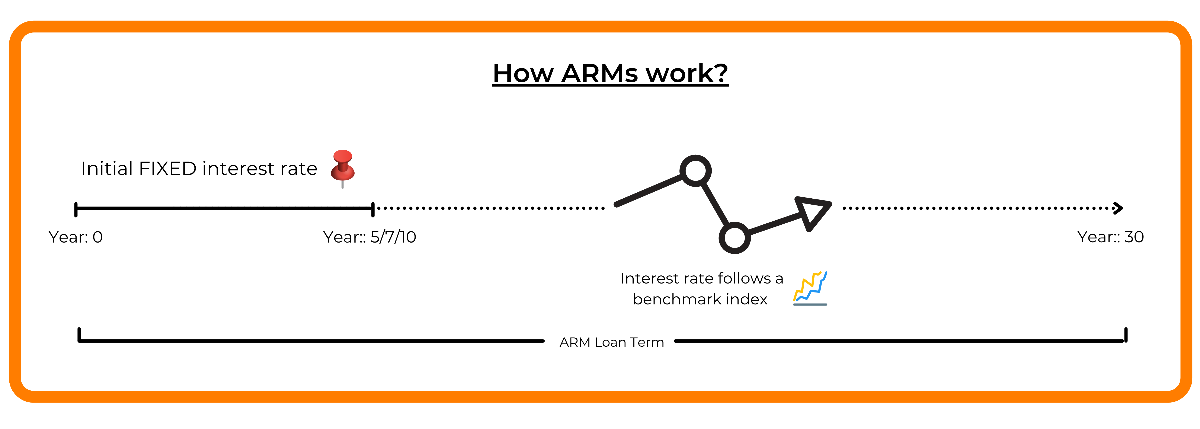

A mortgage with an adjustable rate is one where the mortgage rate changes according to a certain index after an initial period has passed. Contrary to fixed-rate mortgages, the mortgage rate in adjustable-rate mortgages stays fixed only for a period of time which can be the first 5, 7, or 10 years of the mortgage’s term. After this initial period passes, the interest rates fluctuate according to an index and margin. This means that a borrower can get a higher or lower interest rate after the initial period passes, which can be considered riskier than what fixed-rate mortgages have to offer. Adjustable-rate loans are available as 15- or 30-year mortgages.

How do adjustable-rate mortgages work?

In order to fully understand how adjustable-rate mortgages work, we will first explain some terms related to these specific types of mortgages:

Initial Rate

The mortgage rate stays fixed for a certain period of time initially. This rate is typically lower than the mortgage rate offered by fixed-rate mortgages, which makes adjustable-rate mortgages more attractive for some borrowers. The period during which the rate stays fixed is shown by the first number. For example, for an ARM 5/1, the interest stays fixed for 5 years, while for an ARM 7/1, the interest is fixed for 7 years. During this period, borrowers can easily calculate the interest they will be charged on the loan.

Adjustment Period

During this period of time, the mortgage rate fluctuates and follows the index, which we will explain later on. The mortgage rate can be adjusted monthly, quarterly, yearly, every 3 years or every 5 years. So it is possible for you to be charged a different interest rate every month.

Index

The index refers to the benchmark interest rate that the mortgage rate of an ARM follows. The benchmark interest rate can be the prime rate which is affected by the Fed Funds rate; the London Interbank Offered Rate (LIBOR); the Cost of Funds Index (COFI) or the one-year constant-maturity treasury (CMT) securities. If the index rate rises, the interest rate of the adjustable-rate mortgage will rise as well and vice versa. You could ask your mortgage lender to find out which index your mortgage rate depends on and research on how it has fluctuated in the past.

Margin

The interest rate on your adjustable-rate mortgage is made up of the index and a margin, which is decided by the lender. Because of this, the margin may differ from lender to lender, therefore you can shop around in order to find the best deal. Sometimes, the lender will decide the margin they charge you according to your creditworthiness, which can be checked through their credit reports. Therefore a borrower with poor credit would be charged a higher margin than a borrower with better credit. The margin is added to the index rate to find the fully indexed rate, which is the rate that you will be charged.

If your lender charges a margin of 2% and the index used is currently 4%, then the fully indexed rate will be 4% + 2% = 6%. If in the future, the index increases by 1% to 5%, then the fully indexed rate will be 5% + 2% = 7%.

Interest-rate caps

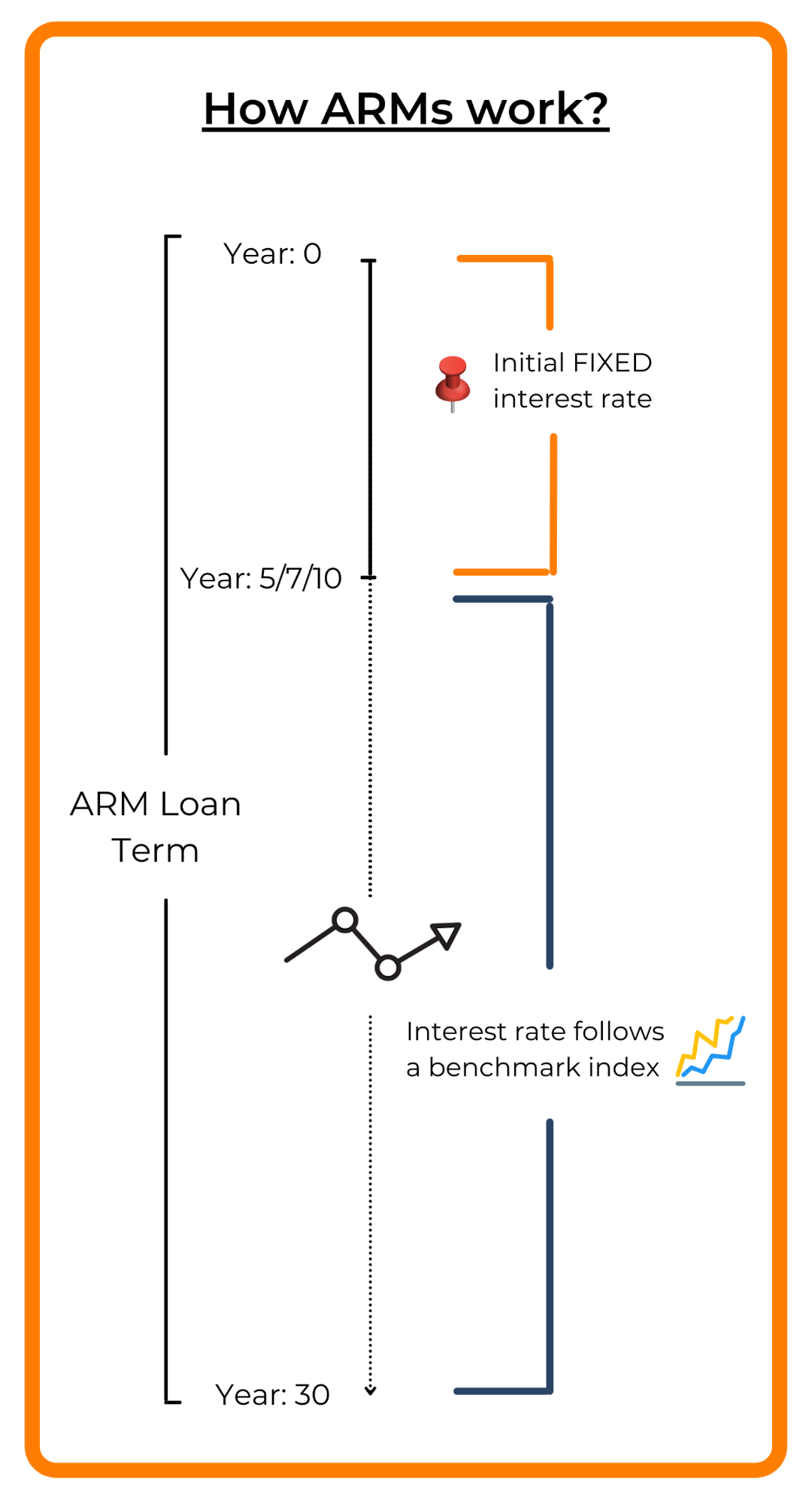

The risk with adjustable-rate mortgage is the fact that the interest rate can increase after the initial period has passed. This will increase your monthly mortgage payment and cost you more interest, therefore making your mortgage more expensive. However, in order to limit the risk these mortgages present, there are caps to how much the interest rate can fluctuate throughout the life of the loan. There are two types of caps: periodic adjustment caps and lifetime caps.

- Periodic adjustment caps limit the amount by which your interest rate can change from one period to the other. For example, one lender can have a periodic adjustment cap of 3%. This means that no matter how the index changes, your mortgage rate cannot increase or decrease by more than 3% the next period. This leaves room for asking how the lender makes back the amount they could not charge because of the cap. The answer is simple. The difference between the index change and the mortgage cap is carried over to the next period.

Example - Interest rate cap

Imagine that you have an adjustable-rate mortgage which has a periodic adjustment cap of 3% and the mortgage rate is adjusted every year according to an index. Your current mortgage rate is 4%. In the first year, the index increases by 5%, while in the second year the index increases by only 1%. How would your mortgage rate change during this 2-year period?

Year 1:

Interest rate cap = 3% < 5%

Mortgage rate increases by rate cap ⇒ New mortgage rate = 4% + 3% = 7%

“Leftover interest rate” = Index rate change - Cap rate = 5% - 3% = 2%

Year 2:

Interest rate cap = 3% > 1%

Mortgage rate increases by index rate change and last year’s “leftover interest”

New mortgage rate = 7% + 1% + 2% = 10%

- Lifetime caps, on the other hand, limit the amount by how much your mortgage rate can change throughout the entire life of the loan. They are another way on how the lender limits the risk you take with adjustable-rate mortgages. For example, if the mortgage rate on your ARM is 5% and it has a lifetime cap of 7%, no matter how the index changes, you will never pay more than a 12% interest on your ARM. This means that even if the index increases add up to more than 7% in the years throughout the loan, nothing above 7% will be applied.

Payment Caps

Just like interest rates, there can also be caps on the amount of mortgage payment you are required to make with an adjustable-rate mortgage. If an ARM has a payment cap of 6%, this means that your mortgage payment from one period to the next will never change by more than 6% no matter how much the interest rate changes by. For example, if your current monthly mortgage payment is $1,200, it can only go up to $1,272 (+6%) or down to $1,128 (-6%). If the interest rate increase would have resulted in a higher payment, then the leftover is added to the mortgage balance.

Example - Negative Amortization

Negative amortization is the technique used when the amount of interest that could not be charged because of the payment cap is added to your mortgage balance. Imagine that:

Current mortgage rate = 3%

Mortgage payment = $1,012

Payment cap = 8%

Index increase = 3%

| What is the new mortgage rate? | Current mortgage rate + Index rate increase 3% + 3% = 6% |

|---|---|

| What would the monthly payment be with this new rate? | Using the Mortgage Calculator = $1,439 |

| What is the maximum allowable mortgage payment? | Current mortgage payment * (1 + Payment Cap) $1,102 * (1 + 0.08) = $1,092.96 |

| How much will be added to the balance of your loan? | $1,439 - $1,092.96 = $346.04 |

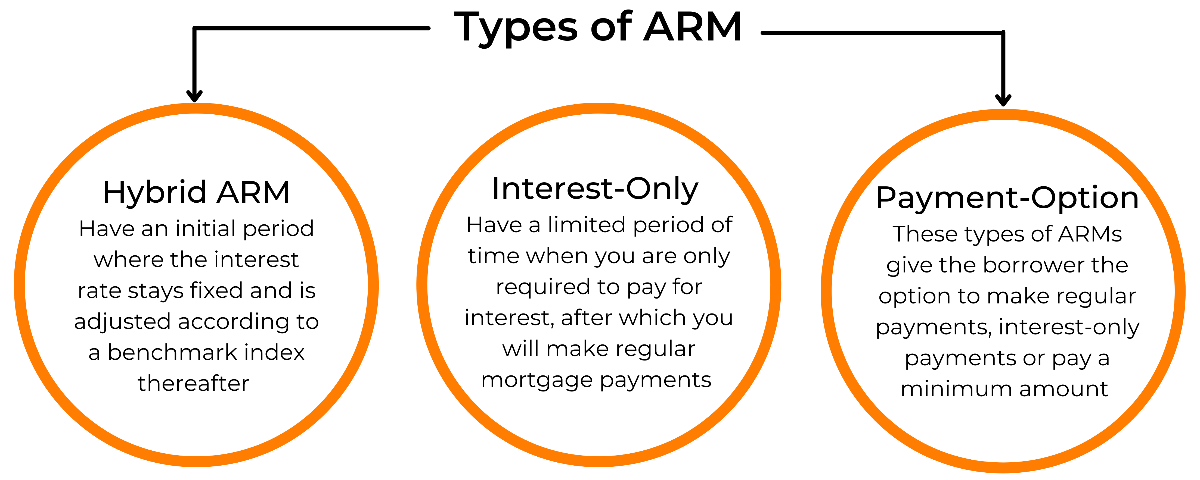

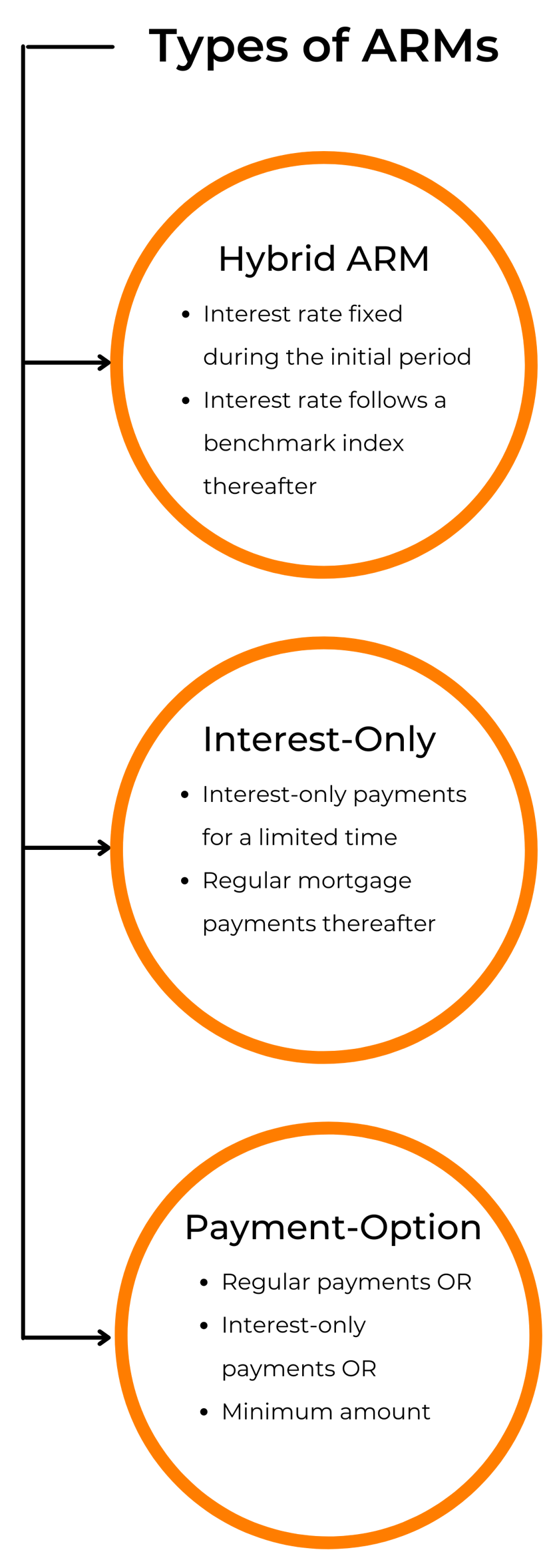

Types of ARMs

There are three main types of adjustable-rate mortgages which we will discuss below:

Hybrid ARM

So far, we have been referring to hybrid ARMs. They are called hybrid since they have an initial period where the interest rate is fixed and a period where the interest rate fluctuates. Hybrid ARMs are denoted by two numbers separated by a slash. The first number shows the number of years during which the interest rate stays fixed, while the second number shows how frequently the interest rate will adjust after the initial period ends. For example, for an ARM 7/1, the mortgage rate will stay fixed for the first 7 years of the loan and will adjust yearly after the 7 years have passed. Common hybrid ARMs are ARM 5/1, 7/1, and 10/1. You can also find ARM 5/5, which means that the interest rate stays fixed for 5 years and adjusts every 5 years thereafter. Some ARMs are advertised as 2/28 or 3/27. In this case, the second number shows the number of years during which the interest rate will be adjustable.

Interest-only (I-O) ARMs

Interest-only ARMs allow borrowers to make only interest payments during the I-O period which typically ranges from 3 to 10 years. Since borrowers are not paying for principal during this period, their monthly payments will be significantly lower, which makes this an appealing alternative for borrowers who want to spend on other expenses when they first purchase a home. However, after the I-O period ends, the monthly payments will significantly increase even if the interest rate doesn’t change. This is because the borrower will now make principal payments in addition to interest.

For example, if you take out a 30-year mortgage with an I-O period of 7 years, you will be making only interest payments for the first 7 years. In the 8th year and forward, you will be required to pay back principal plus interest. It is important to note that the longer the I-O period offered by an ARM, the bigger your monthly payment will be when the interest-only period ends. If you want to calculate a payment schedule on an interest-only loan, you can use an interest-only mortgage calculator to do so.

Payment-option ARMs

From the name, this type of ARM gives borrowers different options of paying back their mortgage. The options include:

- Paying back principal and interest - This is the traditional way of making mortgage payments. By making these types of payments you will lower the balance owed on your mortgage and therefore you will be charged less interest in future periods.

- Making interest-only payments - This option allows you to pay only the interest on your mortgage. However, you have to keep in mind that by not lowering your mortgage balance, in the future you will be making higher interest payments.

- Paying a minimum amount - You can also pay an amount that is even lower than the monthly interest owed. The interest you have not paid will in turn be added to your loan increasing your mortgage balance and increasing the future monthly payments on your loan.

What mortgage types offer adjustable rates?

Borrowers have a variety of options when it comes to the types of loans that are ARMs. These include:

- Conventional loans, most of which are backed by Freddie Mac and Fannie Mae, come as fixed-rate mortgages and adjustable-rate mortgages. For ARMs, borrowers need to make at least a 5% down payment.

- FHA loans, which are backed by the Federal Housing Administration, and are aimed at low-income earners are also offered as adjustable-rate mortgages. The FHA places annual and lifetime interest rate caps to limit borrower’s risk, according to the type of ARM taken.

- VA loans, which are backed by the Department of Veterans Affairs, offer borrowers the option of adjustable-rate mortgage loans. Keep in mind that only veterans, service members or their spouses are eligible for VA loans. Also, while VA loans have no minimum down payment requirement, you would have to pay the VA Funding Fee.

| ARM Type | Interest Rate Caps |

|---|---|

| 1-year and 3-year ARMs | Annually: Up to 1% increase Lifetime: Up to 5% increase |

| 5-year ARMs | Annually: Up to 2% increase Lifetime: Up to 6% increase |

| 7- and 10-year ARMs | Annually: Up to 2% increase Lifetime: Up to 6% increase |

Things to consider before getting an ARM

Before taking out an ARM, make sure you do an evaluation of your financial situation, how you expect it to change in the future, and your plans on the house. Some of the factors to consider include:

Income - How do you expect your income to change in the future, specifically after the initial period where the interest rate stays fixed ends? Remember that you have to account for the risk of interest rates increasing. You can also look at the interest rate and payment caps in order to see if you would be able to afford the worst-case scenario that you reach the cap.

Future Debts - Are you planning to take on other loans in the future? For example, you may plan to purchase a car 5 years down the road or continue your higher education and get a Master’s degree. All these expenses are typically covered through loans, which will increase the amount of your monthly debt obligations. Keep in mind that if you have these debts before you apply for the mortgage, they may increase your Debt-to-Income ratio, which is a factor lenders take into consideration when evaluating your application.

Moving - Do you plan to move from the house in the near future? Usually, adjustable-rate mortgages are a good option when you plan to move from the house before the initial fixed interest rate period ends. This is because that period offers interest rates lower than fixed-rate mortgages, saving you in interest if you don’t keep the house through the adjustable period. Another option for borrowers is also mortgage refinancing.

Prepayments - Do you plan to make any prepayment or pay off the mortgage early? Some lenders may charge penalty fees to borrowers who pay off their mortgage early or make prepayments on it.

Pros and Cons of ARMs

Adjustable-rate mortgages present a number of benefits and drawbacks that borrowers should consider before taking out one.

| Pros | Cons |

|---|---|

| Lower initial mortgage rate | Risk of increasing interest rates |

| Caps limit risk | Prepayment penalties |

| Interest rates may fall |

Pros

Lower initial rate - Adjustable-rate mortgages come with a lower initial interest rate than fixed-rate mortgages. This means that you get to make lower monthly payments initially. The lower interest rate is most beneficial when you plan to move out before the initial period ends or if you are planning to refinance your mortgage.

Caps limit risk - Interest rate caps and payment caps limit the risk borrowers assume when taking out ARMs. Interest caps limit the amount by which interest rates can change even if the underlying index fluctuates drastically. On the other hand, payment caps ensure that there is no major change in your monthly mortgage payment.

Interest rates may fall - The mortgage rate of adjustable-rate mortgages follow an index that may go up or down during the adjustment period. If the index rate goes down, the mortgage rate you are charged for your ARM will also go down.

Cons

Risk of increasing interest rates - If the index rate increases then your mortgage rate will increase too. Even though the interest rate caps may limit the change in your mortgage rate, the difference that you are not charged will still be carried over to the next period. This can make ARMs very expensive for borrowers.

Prepayment penalties - If you are planning to pay off your ARM early, for example, as soon as your fixed-rate period ends, then it’s important to know that you may face prepayment penalties. Prepayment penalties make it more expensive for borrowers to pay off their loan or make earlier payments on it.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.