Closing Cost Calculator for Buyers

Closing Cost Calculation

Fixed Closing Cost

Appraisal Fee | $ |

Property Tax | $ |

Prepaid Interest | $ |

HOA Fees | $ |

Total Fixed Closing Cost | $1,198 |

Variable Closing Cost

Home Inspection Fee | $ |

Homeowners Insurance | $ |

Application Fee | $ |

Credit Report Fee | $ |

Lawyer Fee | $ |

Loan Origination Fee | $ |

Title Insurance | $ |

Title Search Fee | $ |

Discount Points | $ |

Upfront MIP | $ |

FHA, VA & USDA Loan Fees | $ |

Total Variable Closing Cost | $9,425 |

What You Should Know

- Closing costs are the fees paid by a buyer and a seller at the time of closing on a real estate transaction.

- A buyer usually pays 3% to 6% of the home sale price in closing costs while the seller usually pays up to 12% of the home sale price in closing costs.

- The buyer usually pays closing costs that are related to property inspection, loan origination, mortgage insurance, and other fees.

- Some closing costs are fixed, but many of them are variable, which provides an opportunity for the buyer to shop around and get the best price.

Our closing costs calculator determines your total closing costs when you purchase a home. Closing costs will include all the expenses such as lender fees & third-party fees which will help you estimate the total funds that will be required at closing. Closing costs range from 2% to 5% of the loan amount, however, they can vary significantly as there are several expenses that you can shop around for and get a better deal, along with the fixed costs which do not change.

What Are Closing Costs?

Closing costs are the total fees that are paid for the services required when you purchase a new home or refinance your existing home. Closing costs are usually paid by the buyer of the home, but the seller pays some closing costs in the form of real-estate commission.

Closing costs will include expenses such as property-related charges, lender fees, insurance costs and any other costs that are incurred to finalize the mortgage. Some of these expenses are fixed such that they are the same for anyone buying a similar valued home, for example, property taxes. On the other hand, some of the expenses you can shop around for and get a lower fee, for example, home inspection fee or lawyer costs.

When you apply for the mortgage, your lender is required to provide you the Loan Estimate document which will include an outline of the closing costs. Once the mortgage is approved and the deal has gone through, a few days before the settlement date, the lender will give you the Closing Disclosure document which will show all the closing costs that will have to be paid.

How Much Are Closing Costs?

Closing costs are the fees that a buyer and a seller need to pay at the time of closing on a real estate deal. Closing costs are composed of the fees charged by service providers that are involved in the real estate transaction. A buyer and a seller pay closing costs towards different items depending on the state they are in. As a rule of thumb, every party pays for the services that are related to them. For example, a seller will pay the commission to the real estate agents for their help facilitating the transaction while a buyer will pay loan origination fees to their lender for providing the funds for the transaction.

The buyer’s closing costs will include expenses such as property-related charges, lender fees, insurance costs, and any other costs that are incurred to finalize the mortgage. Some of these expenses are fixed such that they are the same for anyone buying a similarly valued home, for example, property taxes. On the other hand, some expenses, such as home inspection fees or lawyer costs, are variable, which means that it is best to check different service providers and find the best deal.

When you apply for the mortgage, your lender is required to provide you with the loan estimate document which will include an outline of the closing costs. Once the mortgage is approved and the deal has gone through, a few days before the settlement date, the lender will give you the Closing Disclosure document which will show all the closing costs that will have to be paid.

Map of Average Closing Costs Across All 50 States

States With the Highest and Lowest Closing Costs

Which states have the highest closing costs and the lowest closing costs in the United States? According to ClosingCorp, the District of Columbia (D.C.) has the highest average total closing costs with taxes in the U.S. at $25,800. This means that a homebuyer looking to purchase a home in Washington D.C. will need to have $25,800 to cover closing costs, and that doesn't even include the down payment! That makes up 4% of the average sales price, which is below the 4.88% in Pennsylvania.

| State | Average Closing Costs with Taxes | % of Average Sales Price |

|---|---|---|

| District of Columbia (D.C.) | $29,888 | 4.32% |

| Delaware | $17,859 | 5.80% |

| New York | $16,849 | 4.53% |

| Maryland | $14,721 | 4.02% |

| Washington | $13,927 | 2.68% |

When looking at the state with the lowest buyer closing costs, Indiana is the cheapest at just $1,909, or 0.99% of the average home sales price. For the lowest closing costs as a percentage of the sales price, the cheapest states are Wyoming and Colorado, which are tied at 0.86%.

| State | Average Closing Costs with Taxes | % of Average Sales Price |

|---|---|---|

| Missouri | $2,061 | 1.06% |

| Indiana | $2,200 | 1.18% |

| North Dakota | $2,501 | 1.01% |

| Wyoming | $2,589 | 0.94% |

| Mississippi | $2,756 | 1.96% |

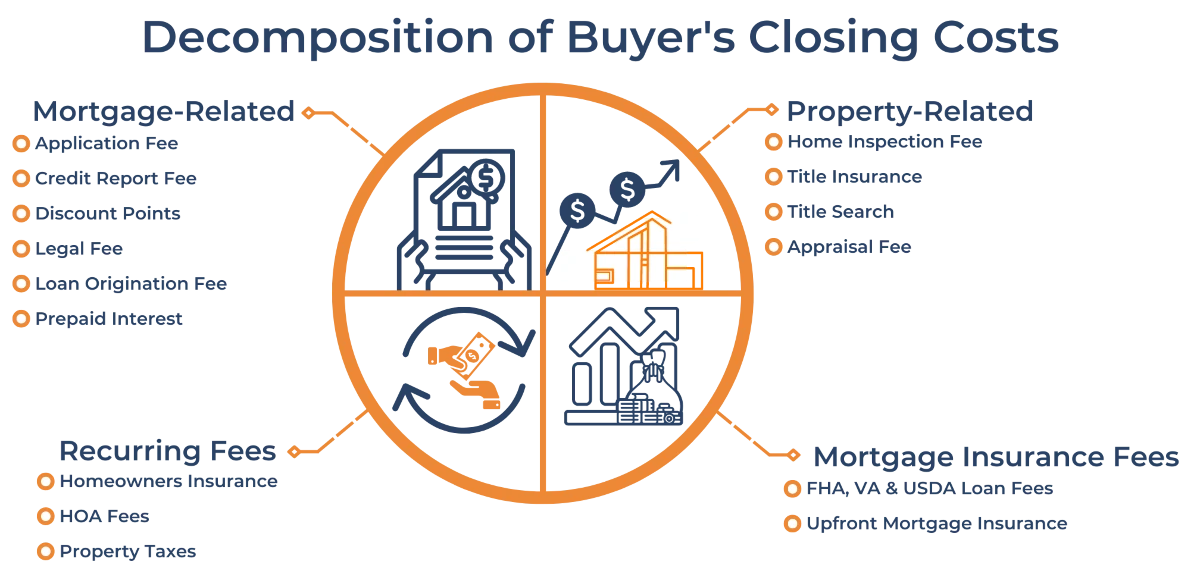

What Is Included in Closing Costs?

Closing costs can be divided into four main cost segments with each having its own subset of fees. Some of the fees are fixed, such that their cost does not change from situation to situation. However, a majority of the fees are variable, which means you can shop around different providers to get the lowest cost offer.

Closing Costs Summary Table

| Closing Costs Summary Table | ||

|---|---|---|

| Specific Fee or Expense | Fixed or Variable | |

| Property-related Fees | Title Insurance | Shop |

| Home Inspection Fee | Shop | |

| Title Search | Shop | |

| Appraisal Fee | Fixed | |

| Mortgage-related Fees | Credit Report Fee | Shop |

| Application Fee | Shop | |

| Loan Origination Fee | Shop | |

| Legal Fee | Shop | |

| Discount Points | Shop | |

| Prepaid Interest | Fixed | |

| Mortgage Insurance Fees | Upfront Mortgage Insurance | Shop |

| FHA, VA & USDA Loan Fees | Shop | |

| Annual Fees | Homeowners Insurance | Shop |

| Property Taxes | Fixed | |

| HOA Fees | Fixed | |

Property Related Fees

- Appraisal Fee - An appraisal is required by the lender to determine the value of the property and the amount that needs to be borrowed. The appraisal fee is around $350.

- Home Inspection Fee - This fee is used to determine if the property meets safety and quality standards. Home inspection fees can range from $350 - $600, our calculator assumes $450.

- Title Search - If the property being purchased is not new, then a title search is required to ensure there are no issues of ownership or liens. Title search fees can range from $400 - $800, our calculator assumes $600.

- Title Insurance - Lenders will require you to get title insurance to ensure that if a situation arises where your ownership is disputed, they can recoup their loan. Title insurance can range from 0.5% - 1% of the home price, our calculator assumes 0.5%.

- Transfer Tax - Transfer tax covers the cost of transferring the deed and the title to a new homeowner. This tax can be quite hefty and is only applicable in some states.

Which States Have a Transfer Tax?

Mortgage-Related Fees

- Credit Report Fee – The lender uses this fee to obtain your credit report. It costs about $25.

- Application Fee – Processing the application has a fee of $350.

- Loan Origination Fee – This fee is one of the largest, and it is also known as the underwriting or processing fee. It involves preparing and evaluating your mortgage such as notary fee, documentation, checking your financial records, verifying information, and the service provided during the entire process. The fee can change depending on the lender, and hence, it is very important to shop around and find the lowest-cost lender. The fee can range from 0.5% - 1% of the loan value, our calculator assumes 0.75%.

- Legal Fee – A lawyer is required at closing to verify all the documents, with legal fees charged hourly. Fees can range from $600 - $1300, our calculator assumes, $1,000.

- Discount Points – Points can be bought which can in turn help reduce your mortgage rate. One point can be bought for 1% of the loan amount and it lowers your mortgage rate by 0.25%. For example, if your loan amount is $300,000 at a mortgage rate of 3.25%, you can buy 1 discount point for $3,000 ($300,000 * 1%) and reduce your mortgage rate to 3% (3.25% - 0.25%). Use our mortgage points calculator to see how points will affect your mortgage.

- Prepaid-Interest – Lenders will require you to pay any interest that is charged from the date of settlement to the first monthly mortgage payment. Prepaid interest can vary based on the number of days interest has to be paid, our calculator assumes 0.14% of the loan amount.

Mortgage Insurance Fees

- Upfront Mortgage Insurance – If the down payment is less than 20% of the home value, then the lender will require you to get private mortgage insurance (PMI). PMI can be financed into the mortgage, or it can be paid upfront.

- FHA, VA & USDA Fees – Government-backed loans have initial costs that have to be paid. FHA loans require FHA Mortgage Insurance Premium (MIP) which is 1.75% of the loan amount. VA loans have the VA funding fee and USDA loans have guarantee fees.

Annual Fees

- Property Taxes – You will be required to pay two months of property taxes. The property rate will be dependent on your location.

- Homeowners Insurance – Lenders will require you to get insurance against potential damages. In most cases, 12 months of insurance is paid upfront, our calculator assumes a cost of 0.4% of the home price.

- Homeowners Association Fees – Some condominium associations, also known as homeowners associations, have fees for maintenance and improving the public condominium property and amenities.

After Closing Costs

There are some costs which generally occur when you move to your new home. They are not part of closing costs, but they should be considered. These costs include moving costs, the bump in expenses which occurs after each move, and the cost of replacing furniture and appliances which are past their prime time and you feel are not worth the move.

Frequently Asked Questions

Who Pays Closing Costs?

A buyer and a seller face different closing costs, so they both face some expenses at the closing of the deal. A seller and a buyer pay for different expenses, so they pay different amounts. On average, a buyer pays 3% to 6% of the home price towards closing costs while a seller may pay up to 12% of the home price towards closing costs. Depending on the market, some items in the closing costs may be negotiated between the buyer and the seller depending on who has more negotiating power. In addition to that, depending on where the deal takes place, a buyer or a seller may be required to pay for certain items that they are not required to pay for elsewhere.

| Buyer Pays | Seller Pays |

|---|---|

|

|

How to Calculate Closing Costs?

Closing costs calculations may look difficult, but they are straightforward as long as you understand what closing costs include. You first estimate the amount for various costs required during closing. Some items may have a fixed cost while others may vary depending on the provider and the property. It is best to shop around and look for providers beforehand to estimate the budget precisely and save money. Once you have an idea of how much every item in closing costs would be, you can sum them up to have the total closing costs. It might be difficult to precisely say how much you will need to pay in closing costs beforehand, so it is best to aim at a property that you can afford.

Example

For example, how much are closing costs on a house with a price of $400,000 with an $80,000 down payment in New York?

Negotiable Fees: Services You Can Shop For

- Home Inspection Fee - $450

- Application Fee - $350

- Credit Report Fee - $25

- Lawyer Fee - $1000

- Loan Origination Fee – $4,000 (0.1% of Loan Value)

- Discount Points – $0

- Title Insurance - $2,000 (0.5% of Home Price)

- Homeowners Insurance – $1,600

- Title Search Fee - $600

- Upfront Mortgage Insurance Premium (MIP) - $0

- FHA, VA & USDA Loan Fees - $0

Total Negotiable Costs = $8,425

Fixed Fees: Services Where the Cost Does Not Change

- Appraisal Fee - $350

- Prepaid Interest – $448 (0.14% of Loan Value)

- Property Tax – $1,127 (1.69% tax rate for New York)

- HOA Fees – $400

Total Fixed Costs = $3,925

Total Closing Costs = $12,350

Closing Costs as a Percentage of Loan Value = 3.85% ($12,350/$320,000 * 100)

Total Cash Amount Required at Closing = $92,350 ($12,350 Total Closing Costs + $80,000 Down Payment)

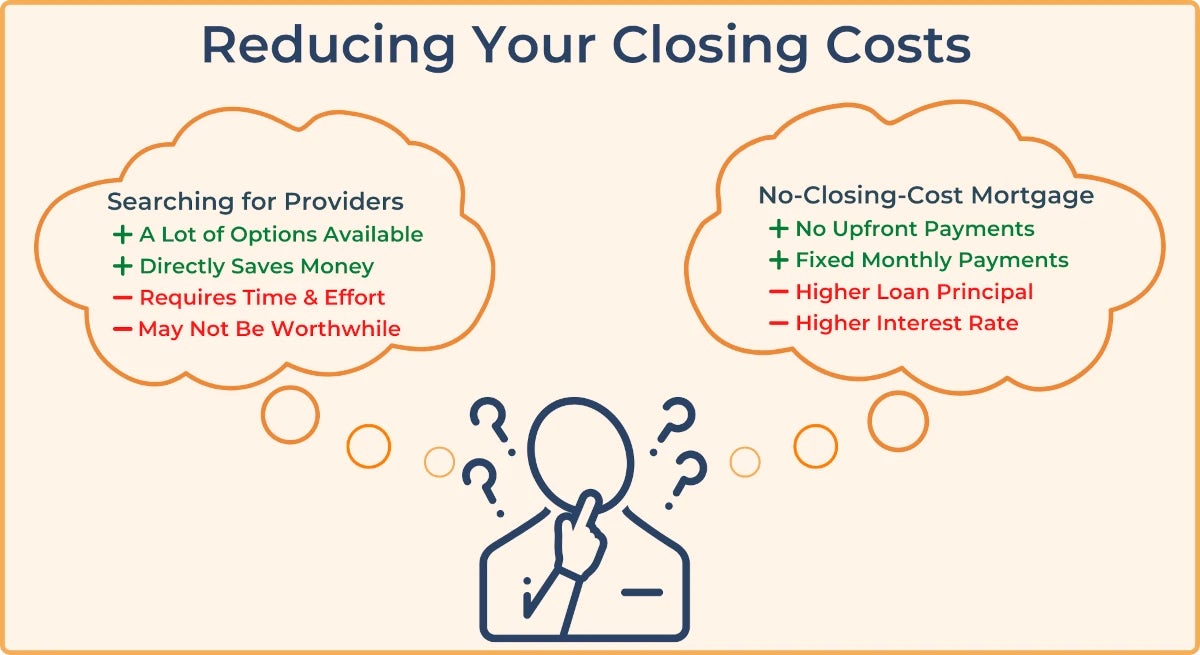

How Do I Reduce My Closing Costs?

Closing costs can be quite hefty given that they depend on the price of the house, but there are ways to save money or simply defer closing costs to a later date. The majority of the closing costs are variable for the buyer, which means that there is a huge potential to save money if the buyer is willing to shop around and find the best deal for as many services as the closing costs include. One of the highest closing costs is lender fees, especially origination charges, which can be close to 1% of the loan amount. If you shop around for different lenders, you may be able to negotiate the origination fee down, which may lead to thousands of dollars in savings. Other items such as title insurance, legal fees, mortgage insurance premiums, and others can also be negotiated, which will provide additional savings.

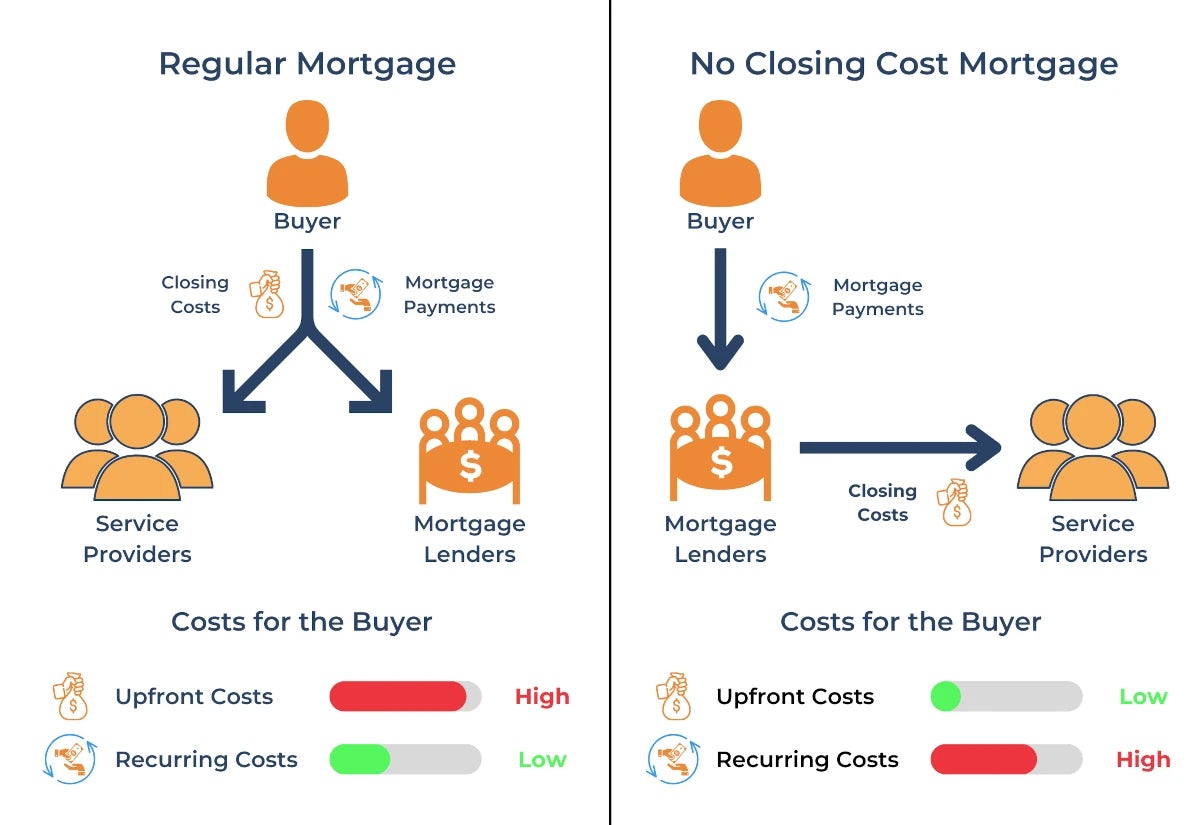

If you have chosen the best providers, but you are still looking to lower your closing cost expense, you may consider rolling it into a mortgage and amortizing it with the principal. Some lenders offer mortgages that include closing costs in the principal amount, which allows the buyer to postpone closing cost payments.

No-Closing-Cost Mortgages

Some banks and lenders offer no-closing-cost mortgages and no-closing-cost refinances . With this special type of loan, the lender bundles the closing costs of your mortgage directly into your principal balance. This means that you can pay the closing costs over time instead of having to pay them all upfront at closing. However, no-closing-cost mortgages typically have a higher mortgage interest rate than conventional mortgages. This means that you will be paying more interest over time. No-closing-cost mortgages are still a suitable alternative for borrowers that might not have enough savings to cover closing costs today and can be a lower-interest cost option compared to alternatives such as getting a personal loan to pay for buyer closing costs.

No-closing-cost mortgages allow buyers to save money on upfront expenses, but a borrower should be aware that they will have to pay for closing costs anyways because they will be rolled into the mortgage. No-closing-cost mortgages also have a higher interest rate that applies to the whole principal. Since the increase in the interest rate applies to the whole principal, the borrower of a no-closing cost mortgage may face a much larger interest expense on their loan than a borrower with a regular mortgage.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.