Land Loans

CASAPLORER®Trusted & TransparentIf you are looking to purchase vacant land instead of a house that is already built, then land loans are an option you should definitely consider. Since the collateral is now the land instead of an actual house, regular mortgages cannot be used for this type of purchase.

What You Should Know

- Land loans are a way of financing the purchase of vacant land

- Land Loans can be used for raw land, unimproved land, or improved land

- Land loans are riskier for lenders which is why they have stricter qualification requirements

- Interest rates on land loans tend to be higher than interest rates on regular mortgages

What is a Land Loan?

A land loan is a financing option for individuals who want to purchase a lot of land for residential or business purposes. The type of land loan you qualify for will depend on where you want to purchase the lot of land and what you plan to use it for. Typically, people who purchase land loans want to build a house on it from scratch.

You might be wondering what makes land loans different from construction loans, which are also used to construct a home from the beginning. For starters, individuals who use construction loans are more clear and confident in their plans for the land. They have already made a plan and know where to start once they have received financing. On the other hand, land loans are more common when the borrower isn’t quite sure on when and how they want to go about building a structure on the land.

Land loans are riskier for lenders for a number of reasons. First off, people are less worried about losing a lot of land, rather than a house. This means that they are not as inclined to keep making the mortgage payments if they are facing difficult financial circumstances. This may lead to lenders not recovering the amounts lent in full. Secondly, there is less demand for land, which makes it difficult for lenders to sell it in the case of default.

Types of Land Loans

There are three types of land loans, which differ from one another from the degree of development of the land itself.

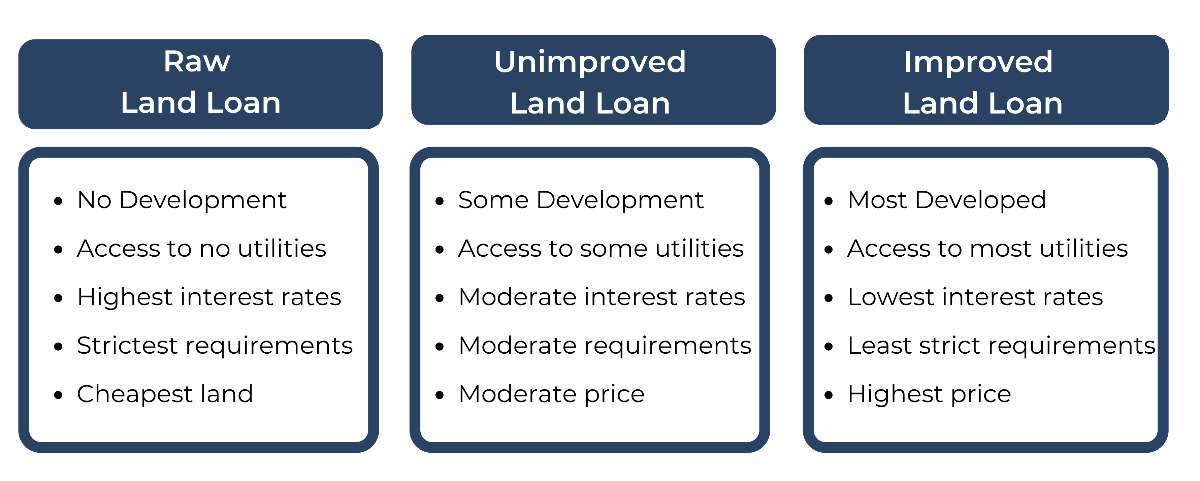

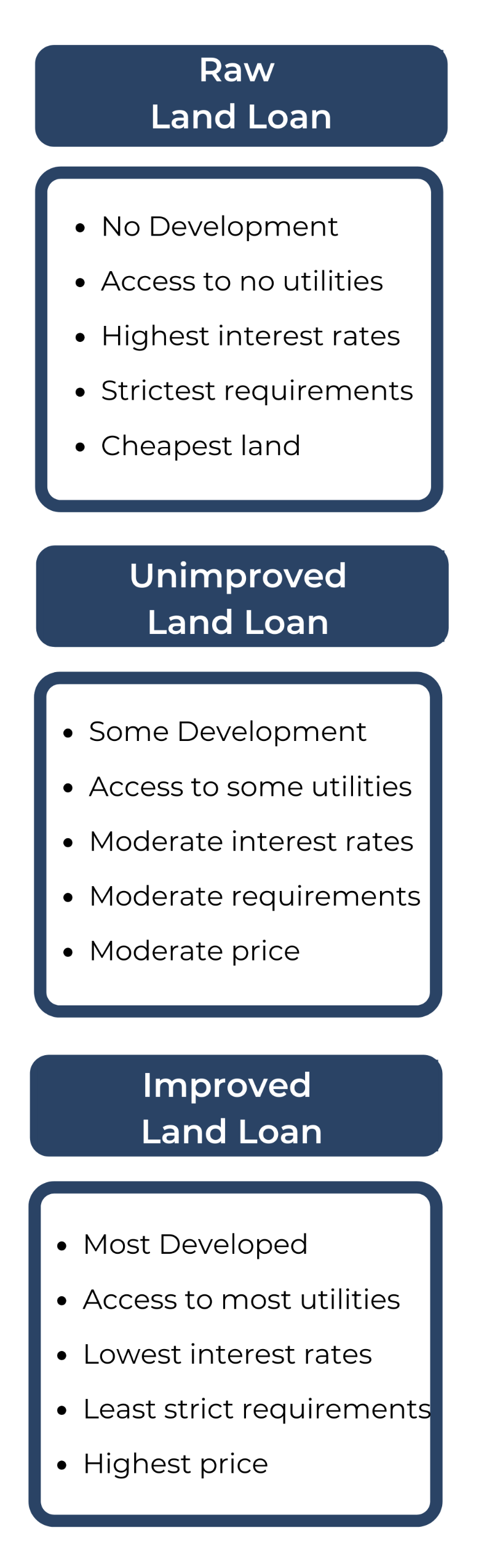

- Raw Land Loan

Raw land includes land that does not have access to electricity, sewers, or even roads. It is land that is not developed at all, and that a borrower would need to develop in order to construct something on it. Since they offer very little, raw land is the cheapest option for people who are looking to purchase land. However, it also poses the most risk for lenders financing these purchases since it is harder to find buyers for raw land. For this reason, lenders put stricter eligibility criteria and ask for a higher down payment, which can also reach 50% of the purchase price. In order to minimize their losses in case, the borrower does default on the land loan, lenders charge higher interest rates on land loans. In order to increase your chances of approval for a raw land loan, make sure you have a clear and detailed plan on how you will develop the land, a large down payment, and a high credit score.

- Unimproved Land Loan

While unimproved land is more developed than raw land, it still tends to lack some basic utilities and amenities, such as an electric meter, a natural gas meter, and a phone box. It is also difficult to get financing for an unimproved land loan, and a detailed development plan, large down payment, and high credit score are still applicable. However, lenders are not as strict as with raw land loans since unimproved land is relatively easier to sell and for a higher price. You can still expect to make a down payment higher than 20%.

- Improved Land Loan

Improved land is the type of land that has access to most amenities and utilities, such as electricity, water, gas, and roads. Improved land is the most expensive type of land since you won’t have to spend money developing it, however, it is also the type of loan that is easiest to obtain financing for. Since there are more buyers who would be interested in improved land rather than raw and unimproved land, lenders find it easier to sell it if the borrower defaults on the loan. While the qualification requirements are less strict, you would still need to have a relatively larger down payment than you would need for regular mortgages.

How do land loans work?

Land loans work in a similar way as regular mortgages. The borrower will typically need to meet some eligibility criteria and provide supporting documentation to prove their creditworthiness. As mentioned earlier, lenders set stricter requirements for borrowers of land loans, since they present a higher risk. Some of these requirements include:

Credit Score - You would typically need to have a credit score of at least 720 to qualify for a land loan. The higher the credit score you have, the better your chances of getting a lower interest rate.

Down Payment - The down payment typically required ranges from 20% to 50% of the purchase price of the loan. The large down payment limits the losses of the lender in case the borrower defaults on the loan.

Debt-to-Income Ratio - The DTI ratio required is typically 30% to 40%. However, as with credit scores, the lower your DTI ratio, the higher your chances of approval and your chances of receiving a lower interest rate.

Loan Term - Land loans come at shorter rates than regular mortgages that have 15- and 30-year loan terms. They typically are 2 to 5 years long and some of them come in the form of balloon mortgages. This means that you would pay the regular monthly payment throughout a specific period, and then make a balloon one-time lump-sum payment at the end of the term.

Intended Use - You would need to present the lender with a detailed plan on how you will develop and use the land once you have received funding. The lender will also need to know about the current condition of the land since they will have to assess its riskiness.

You would also need to provide the necessary documentation on your income, employment, assets, and debt obligations. Once the lender has assessed your information, they will make a decision on whether they will approve your land loan application, and if so, they will assign an interest rate.

Land loans interest rates

Since land loans are riskier for lenders that give them out, they come with relatively higher loan interest rates than regular mortgages. Interest rates on land loans start from 4% and go up to 6%. The exact interest rate you will be charged will depend on the riskiness you present as a borrower, so your credit score, down payment, and DTI ratio, as well as the type of land you have chosen. For example, unimproved land loans come with higher interest rates than improved land loans, but lower rates compared to raw land loans. The reason behind this is that different types of land have different demands and different prices, which affect the chances of the lender recovering the amount lent.

How to get a land loan

If you are trying to get a land loan, then following these three basic steps may be a good place to start:

Choose the land lot - The type of land you choose will determine the amount of work needed to develop it and to construct a house or other building on it. So make sure you choose a lot of land you are interested in before starting to shop around for land loans. You can use websites such as LandWatch, LandSearch, and Land.com to start your search.

Make a detailed plan - Whichever lender you choose to work with, you will need to demonstrate that you have given some thought and you have come up with a detailed plan on how you intend to use the land. The lender will need to be certain that your plan is realistic and that in the case you default, the land will be of use to them. Therefore, start thinking about what you want to do with the land, how you will realize your plans, who will help you in the process, and how much this is all going to cost.

Shop around for lenders - Since land loans are more expensive than regular mortgages, it is important to do your research and see what terms and rates different lenders have to offer. A broker that has experience working with land loans can be a useful resource in this scenario. You can use a land loan calculator to estimate how much a land loan would cost based on different land loan terms and payment frequencies.

Pros and Cons of Land loans

Before you decide to take out a land loan, make sure you evaluate the pros and cons that these types of loans present.

| Pros | Cons |

|---|---|

| Land loans make it possible for individuals to build their dream home where they want and how they want it | It is more difficult to qualify for a land loan due to the strict qualification requirements |

| Land loans give business owners the opportunity to expand or transfer their business to other areas | Land loans come with higher interest rates since the lenders who give them out assume a bigger risk than lenders of regular mortgages where the home is the collateral |

| Some government programs make it possible for borrowers to get a lower interest rate and down payment | There are fewer lenders that offer land loans, which makes it difficult for borrowers to shop around |

| Land loans come with shorter terms, which means that the monthly payments may be larger |

How to find the land lot for you

There are a number of things you should consider before deciding on a lot of land to work on. These include:

Utilities - Depending on the type of land, you may have access to none, some or most of utilities. Since you will need access to all of the utilities in order to build a home, you need to make sure that you have the necessary budget, permits, land space, and that you are abiding by local and state laws.

Zoning and Restrictions - Make sure that there are no zoning issues or restrictions on how you can use your lot of land.

Surveying and boundaries- Complete a boundary survey in order to know the exact boundaries of the piece of land you are about to purchase. To be approved of a land loan, most lenders will require the American Land Title Association (ALTA) boundary survey.

WIldlife and environmental - If you plan to build on the land, do your research and make sure that the land is not protected by any government associations for reasons such as endangered species protection.

Future Plans - The value of your land can change depending on what surrounds it. Therefore, it is very important to be aware of any new facilities that may be built in the near future close to your land.

Land Financing Options

- Lender land loans

These are the land loans we have been referring to so far offered by financial institutions, such as community banks and credit unions. In order to find a lender, make sure to start your search in the area where the land is located. It is easier for local lenders to assess the value of nearby land. However, still, make sure to shop around before making a final decision.

- USDA Rural Housing Site Loans

If you are planning to purchase a piece of land in a rural area, you may be eligible for loans available by USDA. To qualify for USDA loans, your household income must not exceed 115% of the area’s median income, and the population of the area must be less than 20,000 people. The types of loans available include:

- Section 523 loans - You can use this type of loan if you plan to build your own home

- Section 524 loans - You can use this type of loan if you will hire a contractor to build the home for you

- SBA 504 Loans

Those who plan to use the land for business purposes can explore the loan options offered by the U.S. Small Business Administration (SBA). With an SBA 504 loan, you can get financing not only from the lender but from the SBA as well. The SBA can cover up to 40% of the purchase price of the land, while the lender provides 50% and you are only required to put down the remaining 10%.

- Home Equity Loans or HELOCs

If you already own a property, you can use the equity you have built in it in order to purchase a lot of land. Home equity loans and HELOCs are types of second mortgages that enable homeowners to borrow against their home equity. They require no down payment and their interest rates are lower than other types of secured loans. However, by borrowing against your home equity, you are putting your home at risk and could end up losing it if you fall behind on your mortgage payments and default on your loan.

- Seller Financing

Seller financing takes place when the seller acts as the lender for the borrower. Thus instead of taking out a loan from a financial institution, the borrower takes a loan from the lender. Seller financing is sometimes beneficial for borrowers who may face less strict qualification requirements. While this may seem perfect to borrowers who cannot afford a large down payment, there are also downsides to using seller financing. Ownership of the land is not clear because the legal title of the property stays with the seller, which can bring problems down the road. Moreover, the seller may charge higher interest rates, which makes this option more expensive.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.