Is Private Mortgage Insurance Tax Deductible?

What You Should Know

- Private mortgage insurance is tax deductible for all tax years until and including the year 2021, but it may not always be a good idea to deduct PMI premiums.

- Private mortgage insurance can be written off under itemized deductions, but it cannot be written off under standard deductions.

- If total itemized deductions are smaller than the standard deduction, then the taxpayer should not deduct PMI and proceed with the standard deduction.

- Currently, no legislation allows PMI deductions for the tax year 2022 and future tax years, but it may change as the US Congress passes new bills.

What Is the PMI?

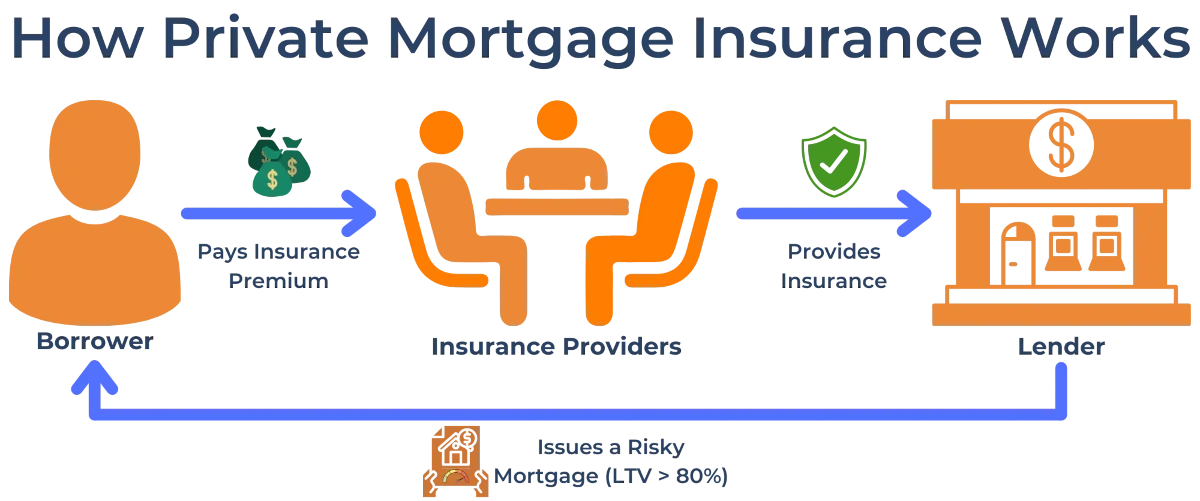

When a homebuyer does not have enough funds to cover a 20% down payment for a conventional loan, the lender may require the borrower to get private mortgage insurance (PMI). The borrower pays for private mortgage insurance, and the insurance protects the lender in case the borrower defaults on their loan. Even though PMI does not benefit the borrower directly, some people choose to pay private mortgage insurance premiums and contribute a down payment as low as 3%.

Homeowners who take PMI usually pay a premium of 0.5% to 1% of the outstanding principal annually. Even though it may look like a small number, borrowers with high mortgage balances may pay thousands of dollars in private mortgage insurance premiums. Given that homebuyers who take PMI do not benefit from the insurance, it is reasonable for the homebuyers to avoid it at all costs. A homebuyer who is considering taking on PMI and paying a down payment of less than 20% should calculate the private mortgage insurance premium they will pay over the lifetime of the loan and decide whether they are willing to pay for it.

How Much You Have to Pay for PMI Annually

| PMI Premium | Outstanding Mortgage Principal | ||||

|---|---|---|---|---|---|

| $300,000 | $500,000 | $750,000 | $1,000,000 | $1,500,000 | |

| 0.50% | $1,500 | $2,500 | $3,750 | $5,000 | $7,500 |

| 0.75% | $2,250 | $3,750 | $5,625 | $7,500 | $11,250 |

| 1% | $3,000 | $5,000 | $7,500 | $10,000 | $15,000 |

| 1.50% | $4,500 | $7,500 | $11,250 | $15,000 | $22,500 |

Is PMI Tax Deductible?

Many people who take on private mortgage insurance as a way of putting down less than 20%, may want to deduct PMI from their tax base since it is an expense similar to deductible interest payments. Some people may want to avoid PMI by taking a piggyback loan, which may allow them to deduct a portion of their expenses. Even though it is not yet clear whether PMI premiums are tax deductible for the year 2022, borrowers with active private mortgage insurance may be able to deduct mortgage insurance premiums for the previous tax years including the tax year 2021.

In 2019, the US Congress passed a Tax Relief and Support for Families and Individuals program as a part of the Further Consolidated Appropriations Act, 2020. This legislation allows the following deductions:

- Private mortgage insurance premiums can be deducted for the year 2021 through itemized deductions.

- Private mortgage insurance premiums can be retroactively deducted for the years from 2018 to 2020. The deductions can be filed via amended tax returns for the respective years. Federal returns can be amended within three years of filing.

- Private mortgage insurance premiums can technically be retroactively deducted for the years before 2018, but it requires filing amended tax returns for the respective years. Federal returns cannot be amended three years after filing.

It is important to note that a borrower who wants to deduct their mortgage insurance premiums will have to use itemized deductions for their income tax calculations. Depending on the financial situation of a borrower, it may not always be a good idea to deduct mortgage insurance premiums.

Should You Deduct PMI?

PMI deduction is only allowed under itemized deductions, which means that it cannot be written off under standard deduction. Standard deduction allows taxpayers to write off a fixed amount of their income from the tax base without providing any justification. On the other hand, itemized deductions may vary based on the individual, and all deductions must be justified. If a borrower wants to deduct PMI premiums, they should consider the total amount they can write off as itemized deductions.

Standard Deduction Amounts by Filing Type and Year

| Tax Year | Filing Type | ||

|---|---|---|---|

| Single Filer | Married Filing Jointly | Head of Household | |

| 2018 | $12,000.00 | $24,000.00 | $18,000.00 |

| 2019 | $12,200.00 | $24,400.00 | $18,350.00 |

| 2020 | $12,400.00 | $24,800.00 | $18,650.00 |

| 2021 | $12,550.00 | $25,100.00 | $18,800.00 |

As a rule of thumb, if total itemized deductions are less than standard deductions for a respective year, the taxpayer should not deduct mortgage insurance premiums and proceed with the standard deduction instead. If the total itemized deduction is less than the standard deduction, then the taxpayer will be losing money even if they deduct PMI premiums fully.

Example - When to Deduct PMI

An individual is considering filing a tax return amendment for the previous 3 years as well as filing taxes for the current year to deduct their PMI expense. The table below provides information on how much the individual spent on private mortgage insurance premiums for each year, all other itemized deductions applicable to the individual, and standard deductions allowed for each year.

| Year | PMI Expense | Other Itemized Deductions | Standard Deduction |

|---|---|---|---|

| 2018 | $5,000.00 | $5,900.00 | $12,000.00 |

| 2019 | $4,320.00 | $6,200.00 | $12,200.00 |

| 2020 | $3,780.00 | $10,250.00 | $12,400.00 |

| 2021 | $3,130.00 | $12,000.00 | $12,550.00 |

Based on this information, the individual wants to calculate whether it makes sense for them to amend their tax returns for the previous years as well as choose itemized deductions for the current year to benefit from PMI write-off. Individuals also have a marginal tax rate of 24%, which allows them to estimate how much they can save or lose by choosing to itemize deductions for a given year.

| Year | Itemized Deduction | Standard Deduction | Savings With Itemized Deductions |

|---|---|---|---|

| 2018 | $10,900.00 | $12,000.00 | -$264.00 |

| 2019 | $10,520.00 | $12,200.00 | -$403.20 |

| 2020 | $14,030.00 | $12,400.00 | $391.20 |

| 2021 | $15,130.00 | $12,550.00 | $619.20 |

After calculating their total itemized deductions and comparing them to standard deductions, the individual realizes that it does not make sense for them to amend their tax returns for the years 2018 and 2019, but they may be able to save some money by itemizing deductions for the years 2020 and 2021. The individual chose to use the standard deduction for the years 2018 and 2019, and they chose to itemize deductions for the years 2020 and 2021.

Restrictions on PMI Deductions

Even though deducting private mortgage insurance may be a good idea for some people, these deductions may not be available for everyone. There are two important restrictions a taxpayer should know before choosing to write off their PMI premiums.

Mortgage Origination Date

PMI premium deduction is allowed only for mortgages that have originated on or after January 1, 2007. Even though it is a strict requirement that may now allow a borrower to write off their PMI premiums, it can be bypassed via mortgage refinancing. If a borrower refinances their mortgage on or after January 1st, 2007, they are left with a mortgage that does not prevent the borrower from writing off PMI expenses.

Income Phaseouts

People who earn a high enough income may not be eligible to deduct their PMI expenses fully. The allowed PMI deduction is reduced by 10% for every $1,000 of income of a taxpayer that exceeds the Adjusted Gross Income (AGI) limit. The AGI limits are set at $100,000 for single filers, heads of household and married filing jointly while the limit for married filing separately taxpayers is set at $50,000.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.