Home Construction Loan Calculator 2026

- Step 1: Select Your Mortgage Type.

- Step 2: Enter Information About Your Property.

- Step 3: Provide Construction and Mortgage Information.

- Step 4: Calculate your results.

| Period | Principal | Interest | Ending Balance |

|---|---|---|---|

| Year 0 Month 1 | $192.25 | $666.67 | $159,808 |

What You Should Know

- A construction loan lets you borrow money to build, renovate, or improve a house.

- Your general contractor receives the construction loan money in draws as the construction progresses.

- During construction, you only have to make interest-only payments. After the construction, you can repay or refinance the loan into a mortgage.

- Construction loan rates are variable and are generally higher than mortgage rates.

About This Construction Loan Calculator

This construction loan calculator lets you estimate your construction loan payments throughout and after the project is complete. This calculator determines your interest-only payments for every month of the construction and calculates the mortgage payment for the loan after the project is complete. It can also help you estimate FHA, USDA, and VA construction loan fees if you choose one of them.

How Do You Calculate a Construction Loan?

Suppose you want to build a house on a piece of land you found. You want to know your monthly payments for the loan during and after construction. The following financial information is available about the cost of the land, construction, and loan:

| Property Information | |

|---|---|

| Cost of Land | $100,000 |

| Construction Cost | $250,000 |

| Down Payment | $70,000 |

| Construction Information | |

| Construction Loan Interest Rate | 9% |

| Length of Project | 12 Months |

| Mortgage Information | |

| Mortgage Rate | 5% |

| Mortgage Term | 30 Years |

Using this construction loan calculator, we can find the loan payments and other important information. The following table shows the results this calculator has returned:

| Construction Loan Information | |

|---|---|

| Initial Construction Loan | $50,833.33 |

| First Interest-Only Payment | $381.25 |

| Last Interest-Only Payment | $2,100.00 |

| Mortgage Information | |

| Initial Mortgage Balance | $280,000.00 |

| Monthly Mortgage Payment | $1,503.10 |

The results show us the initial loan and the initial interest we pay on that loan. We also see the smallest and the largest monthly interest-only payments we will have to pay on the loan. The calculator also shows the initial mortgage balance after the construction is completed and the fixed monthly mortgage payments to amortize the mortgage balance.

Average Cost to Build a House by State

The cost of land largely depends on the location, but it can be easily determined before applying for a construction loan. The construction cost is much more difficult to determine accurately, but it is still possible to estimate how much funds your project requires on average in your area. In 2022, the average cost to build a house in the U.S. is around $284,500, ranging between $109,500 and $460,000. The average price per square foot of a house to build is around $150, which may cost as much as $500 in some cases. The price of the construction depends on the square footage, materials, project complexity, and local wages.

Average Cost to Build a House by State

Types of Construction Loans

This calculator supports four different types of construction loans: conventional, FHA, USDA, and VA. All four types are similar in purpose and structure but different in requirements, rates, and fees. Understanding what options are available and how much they cost may help you save thousands of dollars in interest and fees.

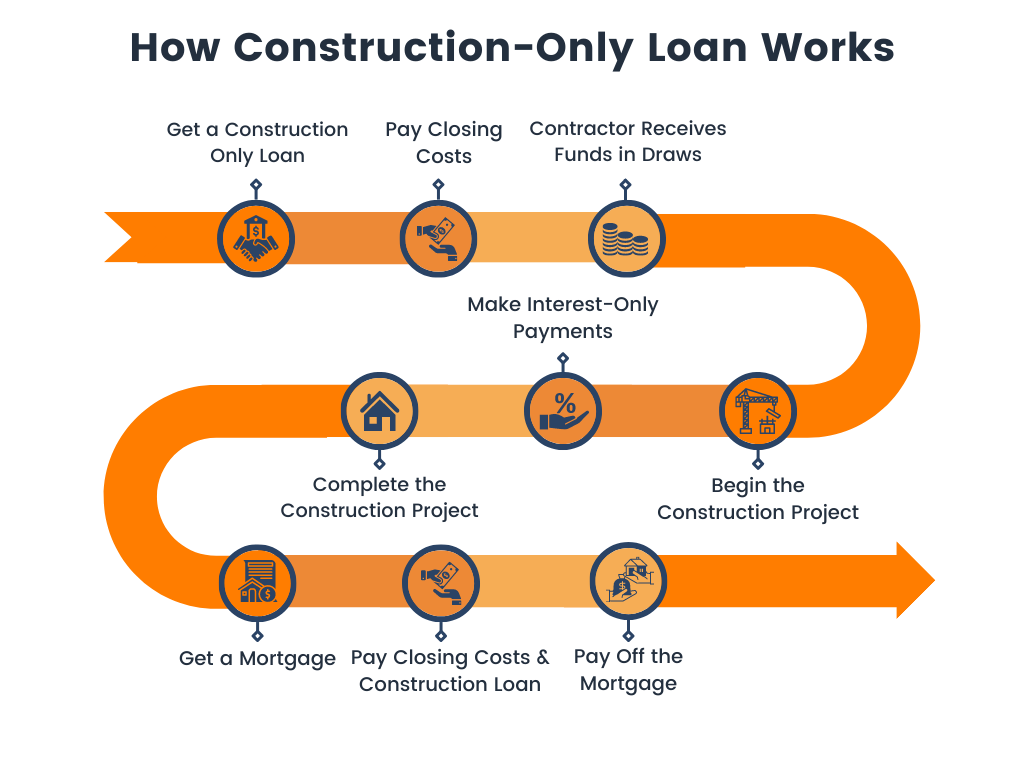

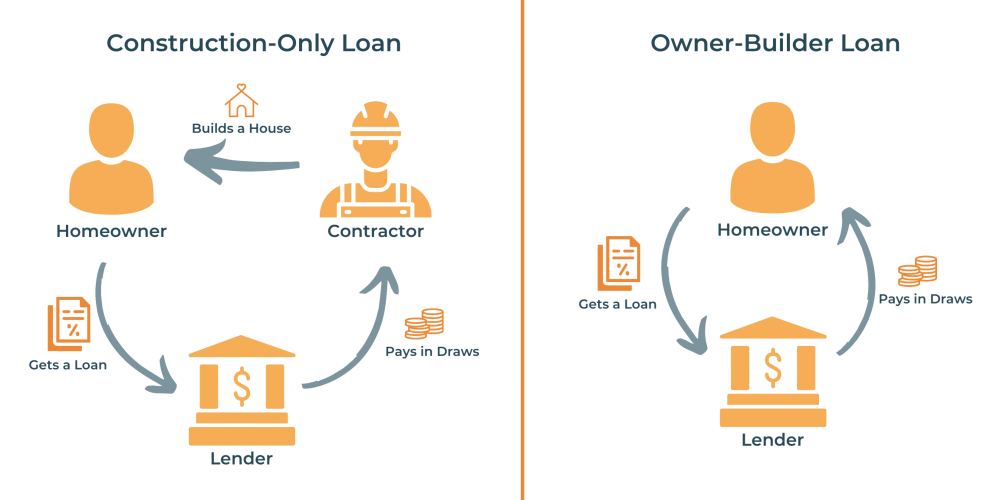

Construction-Only Loan

This type of construction loan has a similar structure as an interest-only loan with a balloon payment at maturity. The borrower pays interest-only payments during the construction, and they will pay the remaining balance in one payment at the end of the construction. This may be a good loan for people who can pay off their loan in full without getting on another loan. If a borrower takes a mortgage to cover the balloon payment, they will pay closing costs twice: at the construction loan origination and the mortgage origination.

This loan is good for people who are certain they can pay off the loan in full or cover a large portion of it. If you cannot cover a large portion of the principal, you will pay extra closing costs that can be avoided with another construction loan product.

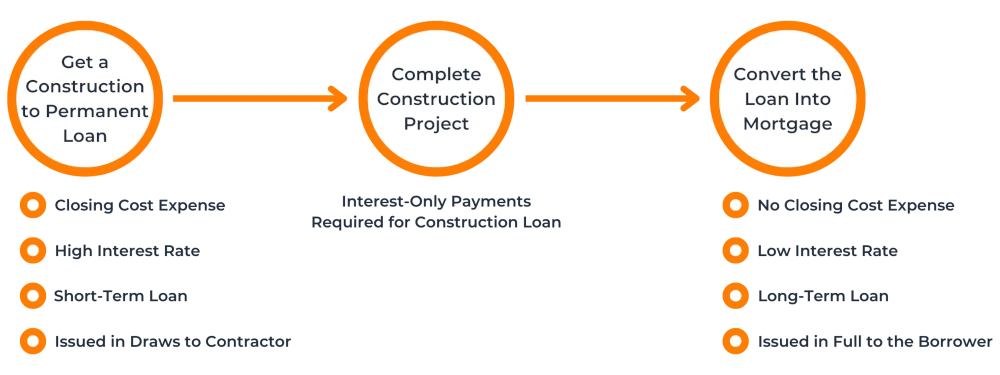

Construction-to-Permanent Loan

Construction-to-permanent loans combine a construction loan and a mortgage in one product. This means that the borrower has to pay closing costs only once since the loan originated once. This loan has a similar structure to interest-only loans because the borrower of a construction-to-permanent loan has to pay off interest only for a specified time period and amortize the principal over the years after that.

Most people may choose this option. This is a good option for people who are certain they will need a mortgage once the construction is complete. This type of loan allows the borrowers to avoid paying for closing costs twice, which may save up to 6% of the total cost.

Owner-Builder Loan

An owner-builder loan allows the owner to manage the construction process directly. In this case, the borrower is the builder who will oversee and work on the project. An owner-builder loan provides financing directly to the owner, but it may require proof that the owner is qualified to oversee the construction. The other loan details are similar to a construction-only loan.

A borrower has to get this loan from a lender who will provide financing in draws. Once the construction is finished, the borrower must pay the loan principal in full. Usually, borrowers get a mortgage to repay the construction loan once the house is built. Since the borrower gets two separate products, they must pay closing costs twice.

Home Renovation Loan

This is a home improvement loan. Even though these loans are not considered construction loans, some can be used to finance small projects or cover a part of a large project. Some unsecured renovation loans can offer financing up to $20,000. It may not be enough to build a house, but it may be enough to build a staircase or complete another small project.

Some borrowers may get backed loans such as a home equity loan or home equity line of credit (HELOC). These loans have low interest rates and origination fees, making them a great financing option for small projects. The calculator on this page can be used as a renovation loan calculator by adjusting the inputs to reflect the renovation loan terms.

Construction Loan Characteristics

While conventional construction loans require a 20% down payment, others require a lower down payment. Various government programs guarantee construction loans to provide access to everyday Americans. Using these programs, you may qualify with a lower credit score or a down payment as low as 0%.

Programs with lower downpayment requirements usually have additional eligibility requirements. For example, most loans have maximum loan restrictions and income caps. Some loans may even require you to live in rural areas to be eligible. The following table compares different construction loans.

Construction Loans Comparison

| FHA | VA | USDA | |

|---|---|---|---|

| Minimum Down Payment | 10%/ 3.5% | 0% | |

| Minimum Credit Score | 500/ 580 | N/A | |

| Maximum DTI | 43% | 41% | |

| Loan Size Limits | Yes | No | |

| Income Limits | No | No | |

| Additional Requirements | N/A | Veteran, or spouse of deceased veteran | |

| Fee Name | Mortgage Insurance Premium (MIP) | Funding Fee |

FHA Construction Loan

The Federal Housing Administration (FHA) guarantees FHA construction loans. They aim to provide financing for low to moderate-income families so they can become homeowners. The FHA construction loan is typically available as a construction-to-permanent loan. FHA also offers a 203(k) loan, which allows you to borrow money to buy a house and renovate it.

FHA Construction Loan Down Payment Requirements

- Credit score of and above 580: You can qualify for the FHA construction loan with a 3.5% down payment.

- Credit score between 500 and 580: You can qualify for the FHA construction loan with a 10% down payment.

- Credit score below 500: You cannot qualify for an FHA loan.

Key Requirements for FHA Construction Loan

- The borrower must have a credit score of at least 500.

- The maximum debt-to-income ratio is 43%.

- The property must be your primary residence.

- There is a maximum loan limit that varies by county.

- You must get an FHA-approved builder.

- Payment of mortgage insurance premiums (MIPs).

VA Construction Loan

The Department of Veterans Affairs (VA) guarantees VA construction loans. The Veteran Affairs Department aims to help veterans, active military personnel, and their families get homes.

A VA construction loan allows qualified borrowers to get a VA construction loan with a 0% down payment and no maximum loan limit. Finding a VA construction-to-permanent (C2P) loan can be challenging. Instead, you may find a VA construction-only loan that you can refinance into a standard VA mortgage.

Key Requirements for VA Construction Loan

- The maximum debt-to-income ratio is 41%.

- Have a Certificate of Eligibility (COE).

- The property must be for your primary residence.

- You must get a VA-approved builder.

- Payment of VA funding fee.

USDA Construction Loan

The United States Department of Agriculture (USDA) issues USDA construction loans through their Rural Development Housing and Community Facilities Program. This program aims to improve the quality of life in rural areas by providing affordable financing.

The USDA offers different types of construction loans. One of the most popular USDA construction loans is the USDA Single Close Construction Loan. It is a Construction-to-Permanent loan, which means that the borrower needs to pay for closing costs only once.

This program is designed to construct rural homes with a 0% down payment. However, few lenders and builders partner with the program due to strict requirements. As a result, you may need to begin with a conventional construction loan and refinance it into a 30-year USDA mortgage.

Key Requirements for USDA Construction Loan

- The borrower must have a credit score of at least 640.

- The maximum debt-to-income ratio is 41%.

- The property must be for your primary residence.

- You must meet the regional income requirements.

- The property must be located in a USDA-designated rural area.

- Payment of USDA guarantee fees.

Frequently Asked Questions

How Do I Estimate Construction Costs?

Estimating the construction cost means calculating how much it costs to build a house. There are several factors that contribute to the construction cost of a house:

- Land - You will first need to purchase land on which you will build your house. The land cost can range anywhere from $5,000 - $150,000, depending on the area and location. Using a land loan calculator, you can estimate your cost of land financing.

- Survey - Before you can start your project, you have to get all necessary documents, which require surveys and engineers working with your plans. It may cost around $5,000 to cover all surveyor and engineer work.

- Site Work - This includes costs for grading, excavation, construction, and anything else that is not related to building the physical structure of the house. The cost to do site work can range from $2,000 to $6,000. The exact cost will depend on the size of the land and its condition.

- Foundation - The foundation is one of the most expensive parts of the house. The cost of the foundation includes the material and labor for breaking ground and pouring the foundation. The foundation usually costs up to $30,000, depending on the home's square footage.

- Framing - This is the most significant part of the home construction budget. Framing includes building the outer structure of the house by fitting together pieces for support. The cost of framing a house will depend on the size of the house and the materials used. On average, it costs $40,000 to $68,000 to frame an entire house.

- Exterior - Building the exterior of a house means covering the entire area of the house that is exposed to the outside. The exterior includes sheathing, roofing, placing windows and doors, and siding. The exterior can cost $30,000 to $75,000.

- System Installation - The systems may include the HVAC, electrical, and plumbing. Each of these systems on their own is expensive. The total cost of system installation can go up to $50,000.

- Interiors - The interior part of a house includes flooring, painting, insulation, appliances, and other features. The cost of the interiors will depend on the materials and appliances that you choose to use. The prices usually range from $50,000 to $150,000.

By allocating the amount you will spend on each category of costs and adding them up, you will get a rough estimate of what construction will cost.

Is a Construction Loan Harder to Get Than a Mortgage?

It is harder to get a construction loan than to get a mortgage. Construction loans also have higher interest rates than mortgages. Construction loans are considered riskier than mortgages because the collateral, which is the house, is not yet built.

Lenders are more cautious about approving construction loans. They require more documentation, including a clear plan of how and when the house will be built and information about a general contractor managing the project. Many lenders may also require a larger down payment and set a higher interest rate than they would for a mortgage.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.