First Time Home Buyer Programs in Arizona

CASAPLORER®Trusted & Transparent

If you are considering purchasing your first ever house in Arizona, then you might want to know that the Arizona Department of Housing, or ADOH, offers a variety of programs to help you make that dream a reality. This agency aims to make homeownership possible for mainly low-income families and neighborhoods in Arizona. Through programs such as HOME+PLUS or Pathway to Purchase, the department offers assistance to first-time and sometimes repeat buyers, with the down payment, closing costs, and other prepaid items. There are requirements, however, that need to be fulfilled, mainly in terms of credit history and income.

First-Time Home Buyer Eligibility Calculator

What You Should Know

- HOME+PLUS program offers assistance with paying closing costs and reduced mortgage insurance premiums

- The Pathway to Purchase program offers down payment assistance up to 10% of the home’s purchase price

- Maricopa County and Pima County have specific down payment assistance programs available for their residents

- Federal programs include conventional loans, FHA, VA, and USDA loans

Arizona State Programs | |||

|---|---|---|---|

| No | Program | Type | Jurisdiction |

| 1 | HOME+PLUS | Main Programs | Arizona State |

| 2 | Pathway to Purchase Down Payment Assistance | ||

County-Specific Programs | |||

| 3 | Home in Five Advantage Program | Restricted Eligibility to Pima County and Tucson | Arizona State |

| 4 | Family Housing Resources Down Payment Assistance | Restricted Eligibility to Maricopa County | |

| 5 | Pima Tucson Homebuyer’s Solution Program | Restricted Eligibility to Pima County and City of Tucson | |

Federal Programs | |||

| No | Program | Type | Jurisdiction |

| I | Conventional Mortgage | Fannie Mae and Freddie Mac | Federal |

| II | FHA Loans | Federal Housing Administration | |

| III | VA Loans | U.S. Department of Veterans Affairs | |

| IV | USDA Loans | U.S. Department of Agriculture | |

Arizona State Programs

HOME+PLUS

HOME+PLUS by the Arizona Industrial Development Authority (AzIDA) is a program that offers first-time homebuyers down payment assistance in the form of a forgivable loan when they take out a 30-year fixed mortgage. This mortgage can be a conventional loan, an FHA loan, a VA loan, or a USDA loan. Borrowers do not have to apply separately for the down payment assistance. Instead, they will be considered for assistance when applying for the first mortgage.

The HOME+PLUS down payment assistance program can also be viewed as a no-payment forgivable second mortgage. This is a type of second mortgage that the borrower does not need to pay back. Instead, the loan becomes forgivable after 3 years. Therefore, if you sell the house or refinance your mortgage before the period of the first three years ends, then you will have to pay back the amount that was lent to you for the down payment.

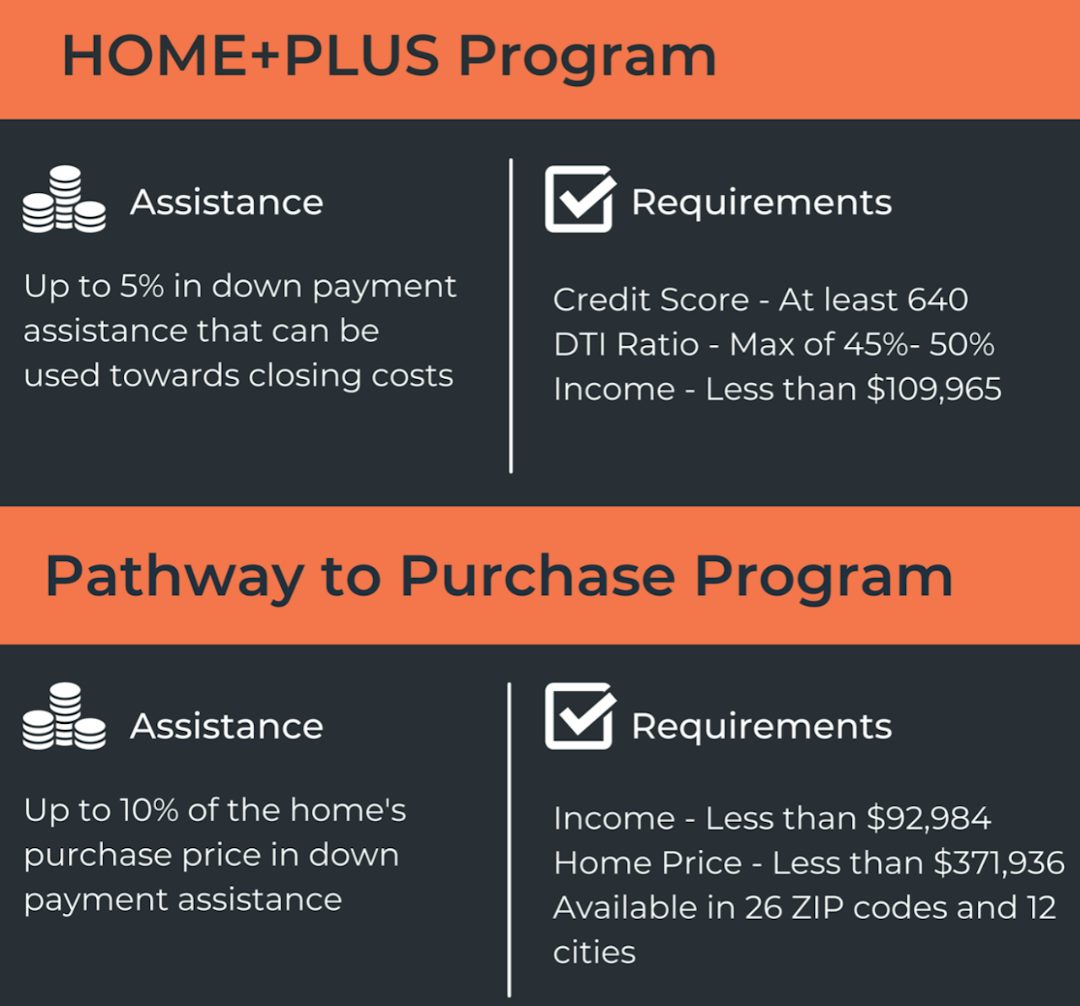

Through the HOME+PLUS program, first-time homebuyers in Arizona can receive up to 5% in down payment assistance. The funds received can also be used towards closing costs. Moreover, the program also offers reduced mortgage insurance premiums so that your monthly mortgage payment remains low. In order to be eligible for the down payment assistance, you will have to fulfill a set of requirements.

Requirements for borrower

- Credit Score - Borrowers must have a credit score of at least 640

- Debt-to-Income Ratio - The DTI ratio must be a maximum of 45% to 50%

- Income - To be eligible, borrowers must have an annual income of less than $109,965

- Education - Borrowers must complete an education course for homebuyers

Requirements for property

- Location - Property must be located in Arizona and the purchase price must not exceed purchase price limits

- Type of property - Eligible properties include single- or two-family homes, townhouses, condominiums, and manufactured homes

- Use - The property must be a primary residence

Pathway to Purchase Down Payment Assistance

If you have had to face foreclosure in the past and are worried about whether you will be able to qualify for a mortgage now, then the Pathway to Purchase Down Payment Assistance program may be the one for you. The program is the result of the collaboration of the Arizona Department of Housing (ADH) and the Arizona Home Foreclosure Prevention Funding Corporation (AHFPFC) and the eligible loans are only the Fannie Mae HFA Preferred Mortgages. It is available in 26 Zip codes in 12 cities in Arizona that are most affected by foreclosure.

Borrowers that qualify for the P2P Down Payment Assistance program can receive up to 10% of the home’s purchase price in the form of a deferred, no-interest second mortgage where they don’t need to make any monthly payments. Just like the HOME+PLUS program, the P2P program is a 30-year, fixed-rate mortgage which is combined with down payment assistance.

Requirements for borrower

- Income - Borrowers must have an annual income of less than $92,984

- Education - Applicants must complete a HUD-approved homebuyer education course

Requirements for property

- Use - The home must serve as a primary residence

- Price - The purchase price of the home must not exceed $371,936

- Location - The program is offered only in Bull Head City, Casa Grande, Glendale, Green Valley, Kingman, Phoenix, Rio Rico, Sahuarita, Sierra Vista, Tucson, Vail, and Yuma

County-specific assistance programs

Family Housing Resources Down Payment Assistance

Family Housing Resources aims to make homeownership more affordable for individuals by offering assistance with upfront costs such as down payment, closing costs, or prepaid items. The FHR offers this assistance through the HOME Down Payment Assistance Program.

To be precise, potential homebuyers can receive up to 3.5% of the purchase price of a property in assistance. However, there is a cap of $3,700. This means that if 3.5% of the purchase price of your new home comes up to more than $3,700, you will still only be able to receive $3,700. As mentioned earlier, you can use the funds to pay for the down payment, closing costs, or any prepaid items.

Requirements for borrower

- DTI Ratio - Borrowers’ DTI ratio must not exceed 45%

- Liquid Assets - After the contribution towards the home purchase, the borrower’s liquid assets must not exceed $10,000

- Down Payment - Borrowers must put at least $1,000 down

- Debts - To be eligible for assistance, borrowers must not owe any money to the City of Tucson for Section 8 or Public Housing

- Education - Borrowers are required to complete the FHR’s Homebuyer Education Class

Requirements for property

- Location - Property must be located in Pima County of Tucson

- Use - The home must serve as the borrower’s primary residence

- Home Inspection - Borrower must pay for a home inspection

Maricopa County Home in Five Advantage Program

The Home in Five Advantage Program is offered by Maricopa County in order to assist future homeowners with the large costs associated with taking out a mortgage. Targeted towards low- and middle-income families, the program offers eligible applicants down payment and closing costs assistance.

Borrowers who qualify for the Home in Five Advantage Programs may receive up to 5% of the home’s purchase price in assistance and use it towards paying their down payment and closing costs. The program also offers the benefit of a loan with competitive mortgage rates. Other borrowers who fulfill some additional requirements may also be eligible for an extra 1% in funds. These groups of borrowers include K-12 teachers, first responders, U.S. military personnel, veterans, and individuals whose annual income does not exceed $36,450.

Requirements of borrower

- Credit Score - Borrowers must have a minimum FICO credit score of 640

- Income - The annual income of applicants must not exceed $108,920

- Debt-to-Income Ratio - To be eligible, the DTI ratio of borrowers must not exceed 50%

- Education - Borrowers are required to complete a homebuyer education course before closing

Requirements for property

- Timeline - Borrowers must move in the property within 60 days of closing on the mortgage

- Use - The property must serve as the borrower’s primary residence

- Location - The property must be located in Maricopa County

- Property type - Borrowers can purchase an existing home, condominium, or townhouse

Pima Tucson Homebuyer’s Solution Program

Similar to other programs, the Pima Tucson Homebuyer’s Solution Program offers assistance to individuals looking to purchase a house by covering some of the costs associated with a mortgage. These costs can include the down payment or other out-of-pocket expenses. First-time and repeat home buyers are eligible to apply for the program.

The program offers a 30-year, fixed first mortgage together with assistance funds that may be up to 3%, 4%, or 5% of the loan amount. The funds can be used towards making the down payment for the house, paying for closing costs, or any prepaid items. An additional advantage is that you won’t have to pay for any repayment or recapture tax from receiving this assistance.

Requirements for borrower

- Applicants must meet qualifying criteria for the FHA, VA, USDA & Freddie Mac guidelines

- Income - Borrowers applying for conventional loans, must have a maximum annual income of $88,950. The income of borrowers of FHA, VA, USDA loans must not exceed $83,020

- Education - Eligible applicants must complete a homebuyer education course

Requirements for property

- Use - The property must be used as a primary residence by the borrower

- Location - The property must be located within Pima County and the City of Tucson

- Property Type - New or existing residential, one–four units - detached or attached - condominiums or townhomes

Federal Programs

Conventional Mortgage

Conventional mortgages are home loans that are not insured by the federal government. There are two types of conventional mortgages: conforming loans and jumbo loans. Conforming loans are those that follow the standards and criteria set by Fannie Mae and Freddie Mac, while jumbo loans do not follow these criteria. As far as assistance for conventional mortgages goes, these agencies offer some programs in order to make homeownership more affordable for first-time buyers.

Freddie Mac - HomePossible Program

- Aimed at very low-to low-income earners

- Minimum down payment of 3%

- Minimum credit score of 660

- No upfront mortgage insurance

- Allows borrowers to use alternate sources of income

Fannie Mae - HomeReady Program

- Minimum down payment of 3%

- Minimum credit score of 620

- No upfront mortgage insurance

- Borrowers can include nontraditional sources of income

FHA Loans

FHA loans are a type of non-conventional loans backed by the Federal Housing Administration. This means that if the borrower defaults on the mortgage, the government will pay back the lender for the amount lost. FHA loans have less strict qualification requirements for borrowers that make it easier for them to get approved. The loans come in 15- or 30-year terms and can be a fixed- or adjustable-rate mortgage.

- Minimum credit score of 500 for a down payment of 10%

- Minimum credit score of 580 for a down payment of 3.5%

- DTI Ratio must not exceed 43%

- The home must be the borrower’s primary residence

- Borrowers are required to pay for upfront FHA MIP and annual variable MIP

FHA Loan Requirements

VA Loans

VA loans are backed by the U.S. Department of Veterans Affairs. The requirements for VA loans are somewhat more lenient than for FHA loans, however, fewer people are eligible. Eligible applicants include veterans, military service members, or their spouses.

- No minimum down payment required

- No minimum credit score requirement

- DTI Ratio must not exceed 41%

- The home must be the borrower’s primary residence

- No insurance required

VA Loan Requirements

USDA Loans

USDA loans are backed by the U.S. Department of Agriculture. These loans aim to make homeownership more affordable for low-income earning individuals who live in rural areas. In order to be eligible for USDA loans, applicants must live in an area with a population of fewer than 20,000 people.

- No minimum down payment required

- No minimum credit score requirement

- DTI Ratio must not exceed 41%

- The home must be the borrower’s primary residence

- The household income must not exceed 115% of the area’s median income

USDA Loan Requirements

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.