US Federal Reserve Interest Rate

Latest Updates and History Since 1982

Current Fed Funds Rate

3.50% - 3.75%

June 17, 2026 - Federal Reserve Update

Federal Reserve Overnight Rate on HoldOn June 17, 2026, the Federal Open Market Committee (FOMC) kept the federal funds rate target range unchanged at 3.50% - 3.75%. The committee said economic activity is expanding at a solid pace despite elevated uncertainty, while productivity growth and capital investment are strong. Job gains have kept pace with the workforce, the unemployment rate has changed little, and inflation remains elevated relative to the committee’s 2% goal.

Highlights from the June 17, 2026, Federal Reserve meeting include:

- The Federal Funds Rate target range is 3.50% - 3.75%.

- The U.S. inflation rate was 4.2% in May 2026.

- The job market added 172,000 nonfarm jobs in May 2026, and the unemployment rate stayed steady at 4.3% in May 2026.

The Federal Reserve is committed to achieving a US inflation rate of 2% over the long run while promoting maximum employment. In May 2026, the inflation rate of 4.2% (YoY) is above the target inflation rate of 2%. The core inflation rate is at 2.9%. The CPI had a monthly increase of 0.5% for all items and an increase of 0.2% for all items, less food and energy.

According to the CME FedWatch Tool, financial markets currently expect the Fed Funds Rate to stay the same during the next Federal Reserve meeting on July 29, 2026. This prediction may change as economic conditions evolve.

Federal Funds Rate Chart

(Upper Limit)

(Lower Limit)

About US Federal Reserve

The US Federal Reserve System, also known as the Fed, is the central bank of the United States and is in charge of conducting monetary policy. It also supervises and regulates financial institutions like large banks and helps maintain the stability of the financial system. It was established in 1913 with the Federal Reserve Act signed by President Woodrow Wilson. It was given three main goals: maximum stable employment, stable prices, and moderate long-term interest rates. Unlike other central banks, for example, the Bank of Canada, the US Federal Reserve is not in charge of issuing or printing currency.

The US Federal Reserve System is a combination of government and private groups that aims to be non-partisan. The Federal Open Market Committee (FOMC), the main decision-making body of the Federal Reserve, consists of 12 voting members: seven from the Board of Governors and five regional Reserve Bank presidents. While the Board of Governors is appointed by the President and confirmed by the Senate, they are appointed for 14-year terms. They can only serve a single term, giving them freedom from the political cycle or worry about re-appointment. The private sector also has significant input into the FOMC as commercial banks play a large role in deciding the presidents of the regional Reserve Banks. This combination of private and public influence allows the US Federal Reserve to remain unbiased and make decisions independently of the federal government and private sector lobbying.

About The Fed Interest Rate

The US Federal Reserve interest rate, or the Fed Funds Rate, is the rate at which commercial banks in the US lend to each other overnight. Banking regulations used to require every bank to hold a percentage of their deposits as reserve with Federal Reserve. Commercial banks used to participate in the overnight market to lend or borrow money from each other in order to manage their deposit levels. Banks with shortage of deposits could borrow money to ensure they are complying with regulations while banks with excess deposit could lend in order to earn a higher interest rate compared with what the Fed offers them as interest on reserve balances (IORB). In March 2020, the Fed brought the reserve requirement ratio down to 0%. Since then commercial banks are not required to hold reserves. Still commercial banks actively participate in the overnight market in order to manage their liquidity.

The US Federal Reserve, as part of its monetary policy operations, aims to keep the Fed Funds Rate within a certain range. The FOMC meets eight times a year to set this range and can use the tools of the Federal Reserve System to make sure that the actual rate, the Effective Fed Funds Rate, is kept within their desired range.

Through affecting interest rates, the Federal Reserve affects the US economy. Interest rates affect the economy through various channels as higher interest rates encourage more saving and discourage borrowing, while lower interest rates discourage saving and encourage borrowing. The most important of these channels is the housing market.

Lower interest rates translate into lower mortgage rates and increase activity (and often prices) in the real estate market. Rising real estate activity would encourage home-building activity and create jobs. On the other hand, increased home prices would increase asking rent prices, which would, in time, increase the average rent tenants are paying and the cost of living.

Prices are sticky on their way down while often are easily accelerated on their way up. Thus low-interest rates often cause price inflation which would cause an increase in CPI.

Fed Funds Rate History

Fed Funds Rate FOMC Meeting Schedule for 2024

| Date of Fed Meeting | Fed Rate Decision | Fed Rate Change |

|---|---|---|

| January 31, 2024 | 5.25% - 5.5% | No Change |

| March 19, 2024 | 5.25% - 5.5% | No Change |

| April 30, 2024 | 5.25% - 5.5% | No Change |

| June 11, 2024 | 5.25% - 5.5% | No Change |

| July 30, 2024 | 5.25% - 5.5% | No Change |

| September 17, 2024 | To Be Decided | - |

| November 6, 2024 | To Be Decided | - |

| December 17, 2024 | To Be Decided | - |

As of August 2024, the Federal Reserve has been maintaining the upper bound rate of 5.50% for over a year, since the meeting on July 2023. During that time, the inflation rate has decreased to be within the inflation rate target range and the unemployment rate has started to climb up. The Federal reserve has not yet announced a rate cut, but there is a high expectation that the rate cutting cycle will start from the September Fed meeting.

In response to the outbreak of COVID-19 and economic shutdowns in the US, the US Federal Reserve moved rapidly to cut their target Fed Funds rate range. In an emergency meeting on March 4th, the Fed lowered their target range by 50 basis points from 1.5% - 1.75% to 1.0% - 1.25%. Only two weeks later, another emergency meeting was held on March 15th to drop the Fed Funds rate down to the zero lower bound with a 100 basis point cut. Reducing the policy rate to its lower bound of zero was the beginning of the Fed’s response to the coronavirus pandemic.

February 2020 started with around $4170B of assets on the Fed’s balance sheet. In March 2020 Fed started what it calls quantitative easing (QE). By March 2022, total assets on the Fed’s balance sheet reached $8970B. In other words, $4800B money was created in just over two years.

During QE, the Fed creates money and uses it to purchase assets. Purchased assets are often government bonds and government agency-guaranteed mortgage-backed securities (MBS). The idea behind QE is that private investors would be pushed into riskier investments or consumption and stimulate the economy when the Fed buys riskless assets.

QE complements reducing the Fed rate. Fed funds rate affects prime rates and sets interest rates for very short-term borrowing or borrowings with a variable rate. QE would lower interest rates for medium and long-term borrowings like fixed mortgages.

Looking back, we can say that the combination of low rates and QE worked too well. It stimulated the economy so well that we are facing an inflation problem, and worse than that, pushing investors toward riskier assets caused bubbles. The prime example of this is the cryptocurrency bubble which has already burst.

Inflation went above and beyond the Fed’s target in April 2021. Until March 2022, the Fed was in denial about inflation. But in March 2022, the Fed started increasing its benchmark rate. As importantly, since June 2022, the Fed would refrain from reinvesting as much as $47.5B of maturing securities it is holding every month. This number is expected to double to $95B monthly in September. When the Fed allows a security it was holding to mature without reinvesting the proceeds; it is equivalent to annihilating that money.

This money supply reduction should cause bubbles to burst, some assets to deflate, and demand to moderate. All these effects are expected to moderate inflation over the coming months.

* Meeting associated with a Summary of Economic Projections.

Federal Reserve Rate Meeting History

Federal Reserve Meeting Schedule for 2023's

| Date of Fed Meeting | Fed Rate Decision | Fed Rate Change |

|---|---|---|

| February 1, 2023 | 4.5% - 4.75% | +0.25% |

| March 22, 2023 | 4.75% - 5% | +0.25% |

| May 3, 2023 | 5% - 5.25% | +0.25% |

| June 14, 2023 | 5% - 5.25% | No Change |

| July 26, 2023 | 5.25% - 5.5% | +0.25% |

| September 20, 2023 | 5.25% - 5.5% | No Change |

| November 1, 2023 | 5.25% - 5.5% | No Change |

| December 13, 2023 | 5.25% - 5.5% | No Change |

Federal Reserve Meeting Schedule for 2022's

| Date of Fed Meeting | Fed Rate Decision | Fed Rate Change |

|---|---|---|

| January 26, 2022 | 0% - 0.25% | No Change |

| March 16, 2022 | 0.25% - 0.5% | +0.25% |

| May 4, 2022 | 0.75% - 1% | +0.5% |

| June 15, 2022 | 1.5% - 1.75% | +0.75% |

| July 27, 2022 | 2.25% - 2.5% | +0.75% |

| September 21, 2022 | 3% - 3.25% | +0.75% |

| November 2, 2022 | 3.75% - 4% | +0.75% |

| December 14, 2022 | 4.25% - 4.5% | +0.5% |

Federal Reserve Meeting Schedule for 2021's

| Date of Fed Meeting | Fed Rate Decision | Fed Rate Change |

|---|---|---|

| January 26, 2021 | 0% - 0.25% | No Change |

| March 16, 2021 | 0% - 0.25% | No Change |

| April 27, 2021 | 0% - 0.25% | No Change |

| June 15, 2021 | 0% - 0.25% | No Change |

| July 27, 2021 | 0% - 0.25% | No Change |

| September 21, 2021 | 0% - 0.25% | No Change |

| November 2, 2021 | 0% - 0.25% | No Change |

| December 14, 2021 | 0% - 0.25% | No Change |

Federal Reserve Meeting Schedule for 2020's

| Date of Fed Meeting | Fed Rate Decision | Fed Rate Change |

|---|---|---|

| January 28, 2020 | 1.5% - 1.75% | - |

| March 3, 2020 | 1% - 1.25% | -0.5% |

| March 15, 2020 | 0% - 0.25% | -1% |

| March 23, 2020 | 0% - 0.25% | No Change |

| April 29, 2020 | 0% - 0.25% | No Change |

| June 10, 2020 | 0% - 0.25% | No Change |

| July 28, 2020 | 0% - 0.25% | No Change |

| September 15, 2020 | 0% - 0.25% | No Change |

| November 4, 2020 | 0% - 0.25% | No Change |

| December 15, 2020 | 0% - 0.25% | No Change |

Historical US Federal Reserve Interest Rates

Prior to the Great Financial Crisis (GFC), the US Federal Reserve used a target rate rather than a range. This became problematic when they lowered the rate to zero during the GFC. As a result, the US Federal Reserve changed their targeting system to a range-based system rather than a specific rate after the GFC.

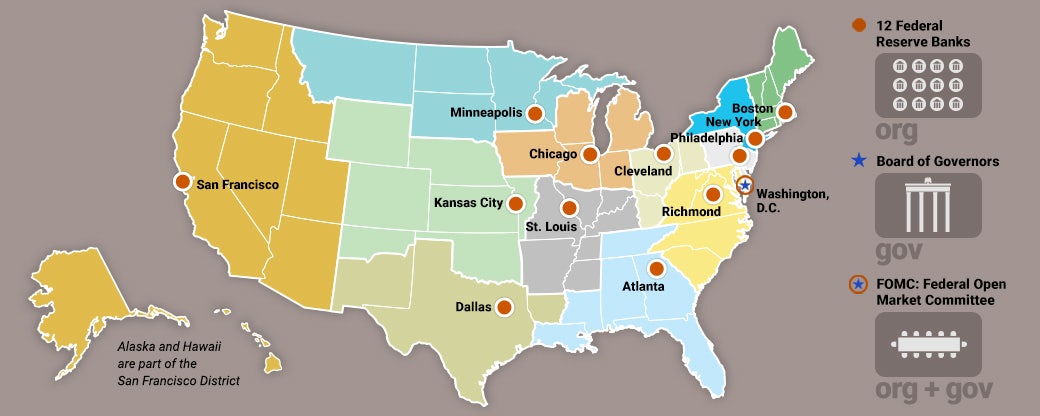

The US Federal Reserve System

Structure of the US Federal Reserve

The US Federal Reserve is made up of three main bodies:

- The Federal Open Market Committee (FOMC), responsible for making decisions on monetary policy

- The Board of Governors, whose members are appointed by the President and confirmed by the Senate, oversees the Federal Reserve banks.

- The Federal Reserve Banks, 12 regional Reserve Banks that act as a "bank for banks" and provide information to the rest of the Federal Reserve system.

The Federal Open Market Committee (FOMC)

The FOMC is responsible for making decisions on monetary policy for the US Federal Reserve. It is made up of 12 voting members: the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining 11 Reserve Bank presidents rotated on an annual basis. Traditionally, the chair of the Federal Reserve Board also acts as the chair of the FOMC and the president of the Federal Reserve Bank of New York acts as its vice-chair.

As part of its role in directing monetary policy, the FOMC is also in charge of executing monetary policy through "open market operations", foreign exchange interactions, and currency swap programs with foreign central banks.

The Board of Governors

The Board of Governors, or the Federal Reserve Board, oversees and governs the operations of the US Federal Reserve and its 12 Federal Reserve Banks. It is made up of seven members that are nominated by the President and confirmed by the Senate for 14-year terms. They cannot be re-appointed. The Chair and Vice Chair of the Board of Governors are also nominated by the President and confirmed by the Senate and serve for 4-year terms, and may be reappointed.

The 12 Federal Reserve Banks

The US Federal Reserve conducts its operations primarily through 12 Federal Reserve Banks. Each bank is responsible for a specific region of the United States and acts as a "bank of banks" to local financial institutions. They provide financial and lending/depository services, collect economic information, and help to regulate and supervise local financial institutions. The president of a Reserve Bank is responsible for the day-to-day operations of the Reserve Bank and also serve on rotated appointments on the FOMC.

A Federal Reserve Bank is a special combination of private and public interests. They are owned by commercial banks who elect six of the nine members of the board of directors. The other three members are appointed by the Board of Governors. While a Federal Reserve Bank can make money from its operations and the services it provides to local financial institutions, all its net profits are given to the US Treasury and are not distributed amongst its shareholders.

The 12 Federal Reserve Banks are:

- Federal Reserve Bank of Boston

- Federal Reserve Bank of New York

- Federal Reserve Bank of Philadelphia

- Federal Reserve Bank of Cleveland

- Federal Reserve Bank of Richmond

- Federal Reserve Bank of Atlanta

- Federal Reserve Bank of Chicago

- Federal Reserve Bank of St. Louis

- Federal Reserve Bank of Minneapolis

- Federal Reserve Bank of Kansas City

- Federal Reserve Bank of Dallas

- Federal Reserve Bank of San Francisco

The Objectives of the Federal Reserve

The Federal Reserve Act of 1913 gives the US Federal Reserve three main goals:

- Maximum sustainable employment

- Stable prices

- Moderate long-term interest rates

To understand these better, we can examine them one by one.

Maximum sustainable employment

The level of unemployment in an economy is an important factor in determining its productivity and the happiness of its citizens. Every economy has a natural rate of unemployment, which is defined by economists as the rate of unemployment that is compatible with a steady inflation rate or the rate of unemployment of an economy at full capacity. While a low unemployment rate is good, an unemployment rate below the natural rate of employment for an economy can lead to competition for workers and excess demand that can signify an overheated economy and bring inflation. An unemployment rate higher than the natural rate of unemployment means that the economy is not at full capacity and could be more productive. The Federal Reserve's job is to keep unemployment near its natural rate, estimated to be around 3.5% for the US economy at the beginning of 2020. Over the past 2.5 years, many disruptions have likely pushed the short-term noninflationary unemployment rate materially higher.

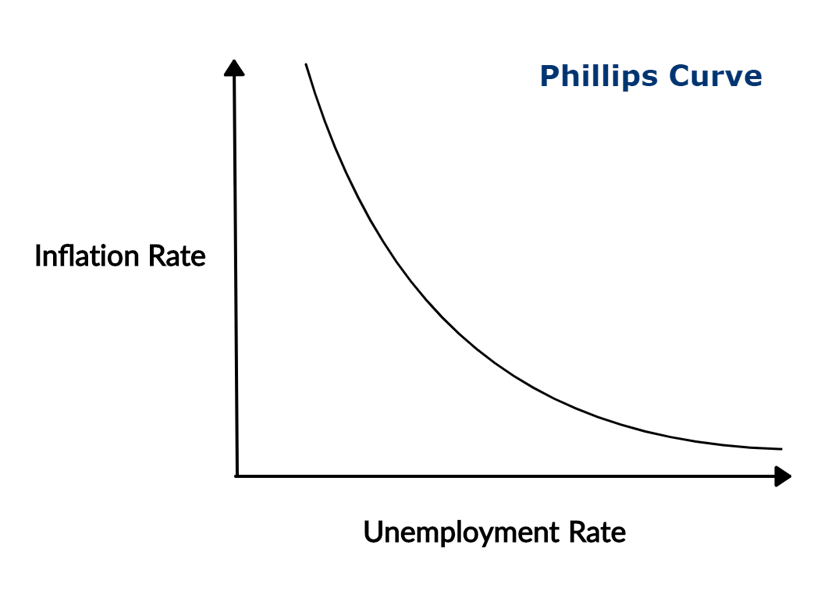

The Phillips Curve and The Relationship Between Employment and Inflation

The Phillips Curve is an economic model that describes the relationship between employment and inflation. The model suggests that there is an inverse relationship between the unemployment rate and inflation: if unemployment goes down, inflation goes up; if unemployment goes up, inflation goes down.

The slope of this inverse relationship changes based on where you are on the curve. If you already have a low unemployment rate and hot labour market, any further decreases in unemployment is likely to lead to a larger increase in inflation compared to if you started out with high unemployment. In addition, if you have high unemployment, going even higher will have less and less effect on inflation.

Stable prices

Stable prices, or stable inflation, is usually one of the most important goals of any country's central bank, including the US Federal Reserve. By keeping inflation, or the growth of prices over time, in check, the US Federal Reserve can maintain confidence in the US Dollar and minimize the costs associated with unstable inflation. For example, with stable inflation, a grocer can predict how expensive goods will be in the future and sign long-term contracts for workers and goods. However, if prices change dramatically from day to day, he cannot plan ahead and has to change prices day by day or risk losing money.

Although deflation, or decreasing prices, can seem like a positive for consumers, it can have a devastating impact on the economy. If you knew that prices were going to drop in the future, you wouldn't spend any money now. If everybody followed this principle, then consumption would stop and the economy would ground to a halt as nobody purchased any new goods or services. In addition, once you are used to deflation and flat or decreasing prices, it can be hard to get back to inflation or increasing prices. This is one of the reasons why central banks aim to keep inflation above zero rather than at zero.

The Federal Reserve aims to keep annual inflation around 2%, similar to the Bank of Canada and the central banks of other developed economies. The rate of inflation most commonly used by the Fed is the Personal Consumption Expenditures (PCE) price index, which takes into account a wide range of household spending but does not consider asset prices.

Average Inflation Targeting

Average inflation targeting is a new approach by the US Federal Reserve System that uses the 2% inflation target as an average rather than a target. This means that the Fed is willing to build inflation above 2% to make up for previous periods of lower inflation, and vice-versa. In contrast, their previous target approach used by most central banks would not take historical inflation into account and would always try to keep inflation as close to 2% as possible.

Given the previous decade of lower than 2% inflation and the deflationary impacts of COVID-19 on household spending, this gives the Fed more room to conduct quantitative easing and loose monetary policy without pressure from a possible rebound in inflation beyond 2%.

Moderate long-term interest rates

One of the less well-known mandates of the US Federal Reserve is its goal to maintain moderate long-term interest rates. This means to keep the interest rate of borrowings by businesses and governments (including cities and state governments) within a moderate range so that it remains affordable to borrow money and invest. While the definition of "moderate" is not clear, it can be taken to mean a rate at which enough investment is made to keep the economy running at its natural rate of unemployment and with stable prices.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.

- The names and logos of third-party products and companies displayed on this website are the property of their respective owners and may also be trademarks.