First Time Home Buyer Programs in Georgia

CASAPLORER®Trusted & Transparent

The Georgia Dream Homeownership Program offered by the Georgia Department of Community Affairs aims to help make homeownership possible for low- and middle-income earners in Georgia. In order to qualify for the program, applicants must meet a set of requirements mainly related to their income, creditworthiness, and their past homeownership experience. The Georgia Dream Homeownership Program offers affordable financing options, down payment assistance, and homeownership education to borrowers who qualify.

First-Time Home Buyer Eligibility Calculator

What You Should Know

- The Georgia Dream Homeownership Program offers affordable financing options, down payment assistance, and homeownership education to eligible borrowers

- The Standard Down Payment Assistance program offers up to $7,500 to qualified applicants

- Individuals working in certain professions can qualify for the Georgia PEN program and be eligible to receive up to $10,000 in assistance funds

- Georgia Choice offers up to $10,000 in funds to borrowers who have a family member living with a disability

Georgia State Programs | |||

|---|---|---|---|

| No | Program | Type | Jurisdiction |

| 1 | Georgia Standard Down Payment Assistance | Main Programs | Georgia State |

| 2 | Georgia PEN | ||

| 3 | Georgia Choice | ||

City-Specific Programs | |||

| 1 | HOME Atlanta 4.0 | Restricted eligibility to the city of Atlanta | City of Atlanta |

| 2 | VCRI | ||

| 3 | Atlanta Affordable Homeownership Program | ||

| 4 | Augusta Down Payment Assistance Program | Restricted eligibility to the city of Augusta | City of Augusta |

| 5 | Columbus Homebuyer Down Payment Assistance Program | Restricted eligibility to the city of Columbus | City of Columbus |

Federal Programs | |||

| No | Program | Type | Jurisdiction |

| I | Conventional Mortgage | Fannie Mae and Freddie Mac | Federal |

| II | FHA Loan | Federal Housing Administration | |

| III | VA Loan | US Department of Veterans Affairs | |

| IV | USDA Loan | U.S. Department of Agriculture | |

Georgia State Programs

Georgia Dream Homeownership Programs

The Georgia Dream Homeownership Programs include the Georgia Standard Down Payment Assistance program, Georgia Protectors, Educators & Nurses (PEN) program, and Georgia Choice. The programs differ from one another in terms of who they are targeted to and eligibility criteria.

How do the Georgia Dream programs work?

Lenders who are willing to offer affordable mortgages to low- and moderate-income families can do so through the Georgia Department of Community Affairs (DCA). The loans can be guaranteed by the FHA, VA, USDA or they can be conventional uninsured loans. Borrowers apply for the Georgia Dream loans through the participating lenders, who then process the application. The lender offers borrowers Georgia Dream mortgage rates. Once the lender gives credit approval, the information passes on to the DCA. The DCA does the compliance review and gives the final funding approval.

The whole process of applying and closing on a Georgia Dream loan typically lasts about 6 months. However, many lenders are able to process the application in a shorter time frame. If there is any delay from the borrower in providing the full documentation requested, then the process may take even longer than 6 months.

Who is eligible for Georgia Dream loans?

- First-time homebuyers

- Homebuyers who haven’t owned a home for the past 3 years

- Homebuyers who can prove that they haven’t used their home as their primary residence for the past 3 years, and who will sell the property or remove their name from the title before closing on a Georgia Dream loan. You are not allowed to own a real estate property when you close on a Georgia Dream loan.

- Borrowers looking to purchase in target areas - If you purchase in what the state considers a “target area”, then you do not have to be a first-time homebuyer. However, you are still required to not own any other real estate or have your name on the title of any real estate property at closing. Target areas are defined as those where at least 70% of the families have a Household Annual Income that is 80% or less of the statewide median family income. Target areas can also be those designated by the State as under continuous economic distress and approved by the Secretary of the U.S. Department of Housing and Urban Development and the Secretary of the U.S. Department of Treasury. To check if the area you are interested in is considered a target area, you can ask the participating lender you are working with for a list of targeted census tracts.

How do I apply for a Georgia Dream loan?

The process of applying for a Georgia Dream loan is similar to the process of applying for any other loan. You apply by submitting an application to one of the participating lenders for an FHA, VA, USDA or conventional uninsured loan. The lender then processes your application and the provided supporting documentation. Borrowers do not apply for the Georgia Dream loans through the DCA.

Before you start your home search, make sure you can first get pre-qualified by contacting the lender. You will also want to complete your homeownership education. You can complete an online class with one of the Housing Counseling agencies found on the DCA’s or HUD’s website. The cost of these classes ranges from $50 to $100.

The Requirements for Georgia Dream Loans

Income - The requirement of maximum income includes the income of all the members in the household, apart from that of students under the age of 18. The maximum household income required varies by county, therefore, you will need to discuss with your own lender what is the specific requirement for your area.

| County | Maximum Household Income | Maximum purchase price | |

|---|---|---|---|

| 1 or 2 persons | 3 or more persons | ||

| Barrow, Bartow, Carroll, Cherokee, Clayton, Cobb, Coweta, Dawson, DeKalb, Douglas, Fayette, Forsyth, Fulton, Gwinnett, Heard, Henry, Jasper, Morgan, Newton, Paulding, Pickens, Pike, Rockdale, Spalding or Walton | $84,000 | $96,000 | $325,000 |

| Any other county not listed above | $72,000 | $83,000 | $275,000 |

Credit Score - Applicants must have a minimum credit score of 640.

Liquid Assets - The maximum amount of liquid assets that the applicant is allowed to have is either $20,000 or 20% of the home purchase price, whichever amount is greater at the time of closing. Liquid assets are also considered things such as:

- Gifts of a substantial amount

- Stocks and other readily salable securities, unless they are restricted by IRA, 401(k) plans or other requirements

IRAs, 401(k) plans and other similar retirement accounts are not considered to be liquid assets.

Housing ratio and DTI ratio - The housing ratio shows in percentage form, the portion of your income that will go towards making the monthly mortgage payment, your monthly property tax and homeowners insurance. On the other hand, the DTI ratio, besides from the mortgage payment, also includes other debt obligations that the borrower may have. You will need to speak to the lender and see whether your ratios qualify you for a Georgia Dream loan depending on the type of mortgage you have applied for.

Minimum Down Payment - You will need to put at least $1,000 down in order to be eligible for the down payment assistance. This amount can also come in the form of a documented gift.

Georgia Standard Down Payment Assistance Program

Borrowers who apply for the Standard down payment assistance program are able to get up to $7,500 in down payment assistance. It is important to point out that if the borrower at any point sells the house, refinances the loan or transfers the ownership of the property to someone else, they are required to pay back the funds they received in the beginning as down payment assistance. Borrowers who can qualify for other programs, such as Georgia PEN or Georgia Choice, are eligible to receive up to $10,000 in assistance funds.

Georgia PEN

Individuals working in certain professions, such as public protectors, educators, nurses and active military service members and National Guard, may qualify for up to $10,000 in down payment assistance funds through the Georgia PEN program. These include:

- Protectors - Employees of the department of the police, sheriffs, highway patrol, probation, correctional or fire department, including EMS and volunteer firefighters

- Educators - Employees of state-recognized local, city or county school, including colleges and private schools

- Nurses - Employees of a state-licensed health facility, such as a hospital, health department, doctors’ office, dentists' office and nursing homes

Similar to the Standard program, the down payment assistance funds will come due if you decide to sell your home, refinance the loan or transfer ownership of property.

Georgia Choice

Applicants who qualify as disabled or who have a family member that is living with a disability are eligible for the Georgia Choice program. This program offers borrowers up to $10,000 in down payment assistance funds.

Participating Lenders

Click for List of Lenders

Counties in this region:

- Bartow

- Catoosa

- Chattooga

- Dade

- Fannin

- Floyd

- Gilmer

- Gordon

- Haralson

- Murray

- Paulding

- Pickens

- Polk

- Walker

- Whitfield

FAQ - Georgia Dream Homeownership Program

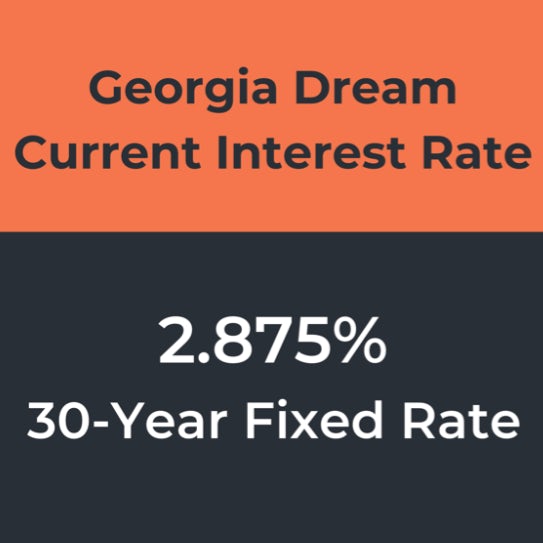

Who decides the mortgage rate for my Georgia Dream loan?

The mortgage rate offered by all the participating lenders in the Georgia Dream Homeownership Program is decided on by the DCA. Currently, the mortgage rate for a Georgia Dream loan is 2.875% for a 30-year fixed rate mortgage. Lenders are not allowed to charge additional fees besides those decided upon by the DCA. The mortgage rate is locked in for 75 days, however, the DCA typically changes the interest rate weekly or more often.

Who do I make the monthly mortgage payments to?

The mortgage payments will be made to the State Home Mortgage, that will be your servicer, at the first of each month. Once you make your first mortgage payment, you will receive a coupon at closing.

Do I have to pay back the down payment assistance loan?

Yes, the down payment assistance loan comes due when the borrower either sells the house, refinances the loan or transfers ownership of the property to another party. Until one of these scenarios takes place, the down payment assistance is a 0% interest loan where you don’t have to make any monthly payments. Similar to a second mortgage, a second lien is placed on your property.

Can I repay the mortgage early?

Yes. There are no prepayment penalties to paying off your Georgia Dream loan early.

City - Specific Programs

Besides the state-wide programs, it is also worth looking into whether there are any homeownership assistance programs offered only in the city you live in. Atlanta, Augusta and Columbus are three of the cities that offer their residents that extra incentive by offering city-specific assistance programs.

City of Atlanta

Atlanta has a range of assistance programs not only for those looking to purchase a home for the first time but also for those who are planning to renovate their homes.

HOME Atlanta 4.0

HOME Atlanta 4.0 offers 30-year fixed rate FHA or VA loans, where eligible borrowers may receive 3.5% of the loan’s amount in the form of a grant that they do not have to pay back. The funds can be used towards the down payment and closing costs. In order to qualify, applicants must meet the qualification requirements of an FHA or VA loan.

Requirements

| FHA Loan | VA Loan | |

|---|---|---|

| Minimum Credit Score | 660 | 680 |

| Maximum DTI Ratio | 45% | 45.01% - 50% |

| Maximum Purchase Price | $325,000 | |

| Eligible Properties | Single-family detached homes, 2-4 units, townhouses, condominiums, newly constructed or existing | |

| Household Size | Household Income Limit |

|---|---|

| 1 person | $68,350 |

| 2 people | $78,100 |

| 3 people | $87,850 |

| 4 people | $97,600 |

| 5 people | $105,450 |

VCRI

VCRI (Vine City Renaissance Initiative) provides borrowers with up to $10,000 in funds that they can use towards paying off their down payment and closing costs. The VCRI program may be right for you if you plan to stay in your home for more than 5 years since the funds become forgivable once the borrower lives in the home for 5 years.

Requirements

- Must qualify for a 30-year fixed-rate FHA, VA, or conventional loan

- The minimum credit score required will be determined by each participating lender of Invest Atlanta

- Liquid assets must not exceed $10,000

- Eligible properties include single-family detached homes, 2-4 unit townhouses and condominiums, newly constructed or existing

- Property must be within the boundaries of the incentive: Donald L. Hollowell Pkwy to the north; Northside Dr to the east, Martin Luther King Jr. Dr. to the south; Joseph E. Lowery to the west.

| Household Size | Household Income Limit |

|---|---|

| 1 person | $84,560 |

| 2 people | $96,600 |

| 3 people | $108,640 |

| 4 people | $120,680 |

| 5 people | $130,340 |

Atlanta Affordable Homeownership Program

The Atlanta Affordable Homeownership Program offers homebuyers a grant of up to $20,000 which becomes forgivable after 5 or 10 years of them living in the house, depending on the amount received. The funds can be put towards the down payment or closing costs.

Requirements

- Must qualify for a 30-year fixed-rate FHA, VA, or conventional loan with one of the participating lenders in Invest Atlanta

- A minimum credit score of 580

- Maximum debt-to-income ratio of 31%/ 43%

- Maximum liquid assets of $10,000

- Maximum purchase price in DeKalb and Fulton County

New Construction → $238,000

Existing Homes → $215,000 in DeKalb County and $223,000 in Fulton County - Eligible properties include single-family detached homes, 2-4 unit townhomes and condominiums, newly constructed or existing

- Property must pass the Home Quality Standards and Environmental Review inspections

| Household Size | Household Income Limit |

|---|---|

| 1 person | $48,300 |

| 2 people | $55,200 |

| 3 people | $62,100 |

| 4 people | $68,950 |

| 5 people | $74,500 |

City of Augusta

Augusta Down Payment Assistance Program

The Augusta Housing & Community Development Department (AHCDD) offers first time home buyers whose household income is classified as low or moderate, assistance with funds that can be used towards making the down payment and paying for the closing costs of a house. The department achieves this with the help of the U.S. Department of Housing and Urban Development’s HOME and American Dream Down-Payment Initiative programs. The maximum amount of assistance is $5,000 which is made fully forgivable after 5 years of the borrower living in the house.

Requirements

- Applicants must be first time homebuyers

- The applicant’s total income must not exceed 80% of the area’s median income depending on family size

- To qualify, a department-approved home buyer education program must be completed

- The home must serve as the borrower’s primary residence

- Property must be a one unit single family dwelling located within Augusta-Richmond County, with the city of Blythe excluded

- The purchase price of the property must not exceed 95% of the median purchase price of a single-family homes in the Augusta Metropolitan Statistical area, or FHA mortgage limits for the MSA

City of Columbus

Columbus Homebuyer Down Payment Assistance Program

The Columbus Homebuyer Down Payment Assistance Program by the Columbus Community Reinvestment department offers a 0% interest loan up to $10,000 to low-income earners. The exact amount offered cannot exceed 5% of the purchase price of the house. Different from other programs, these funds cannot be put towards covering the closing costs. To qualify for the program, the household gross income must not exceed 80% of the area’s median income.

Federal Programs

Conventional Loans

Conventional loans consist of conforming loans which follow the standards set by Freddie Mac and Fannie Mae, as well as jumbo loans. While a 20% down payment is the typical requirement for conventional loans, the two agencies offer programs with less strict criteria to make it more affordable for low income earning individuals to purchase a home. These programs include:

Freddie Mac - HomePossible Program

- Aimed at very low-to low-income earners

- Minimum down payment of 3%

- Minimum credit score of 660

- No upfront mortgage insurance

- Allows borrowers to use alternate sources of income

Fannie Mae - HomeReady Program

- Minimum down payment of 3%

- Minimum credit score of 620

- No upfront mortgage insurance

- Borrowers can include nontraditional sources of income

FHA Loans

FHA loans are a type of unconventional loans secured by the Federal Housing Administration. FHA-approved lenders offer these loans to borrowers who meet the qualification requirements and in the event that they default on the loan, the FHA pays back the lender. The loans come in 15- or 30-year terms and can be a fixed- or adjustable-rate mortgage.

FHA Loan Requirements

- Minimum credit score of 500 for a down payment of 10%

- Minimum credit score of 580 for a down payment of 3.5%

- DTI Ratio must not exceed 43%

- The home must be the borrower’s primary residence

- Borrowers are required to pay for upfront FHA MIP and annual variable MIP

VA Loans

VA loans are unconventional loans backed by the U.S. Department of Veterans Affairs. The only eligible applicants for these types of loans include military service members, veterans or their spouses. VA loans offer somewhat more lenient eligibility criteria than FHA loans, as long as you are a part of one of the groups mentioned above.

VA Loan Requirements

- No minimum down payment required

- No minimum credit score requirement

- DTI Ratio must not exceed 41%

- The home must be the borrower’s primary residence

- No insurance required

USDA Loans

USDA loans are aimed at low-income earning individuals living in rural areas. They are backed by the U.S. Department of Agriculture, which classifies rural areas as the ones that have a population fewer than 20,000 people.

USDA Loan Requirements

- No minimum down payment required

- No minimum credit score requirement

- DTI Ratio must not exceed 41%

- The home must be the borrower’s primary residence

- The household income must not exceed 115% of the area’s median income

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.