USDA Guarantee Fee

What You Should Know

- All USDA loans require mortgage insurance which is called USDA Guarantee Fee, and it consists of a one-time upfront fee and an annual fee that is charged throughout the loan term.

- USDA Guarantee Fee charges an upfront fee of 1% of the original principal and an annual fee of 0.35% of the outstanding principal.

- USDA loans are backed by the US Department of Agriculture, which allows borrowers to get a loan at a comparatively low interest rate.

- USDA Guarantee Fee is charged only for Guaranteed USDA Loans, and it is not charged for Direct USDA Loans.

USDA Loan Mortgage Insurance

USDA loans are unique because they do not require any down payment, they tend to have a lower interest rate than conventional loans, and they require a low credit score because the US Department of Agriculture insures all USDA loans. This combination of factors makes it a very attractive option for homebuyers, but it also comes with certain costs and restrictions that may not make it fit for everyone.

USDA loans have specific eligibility requirements that differ from other types of mortgage loans. More specifically, location-specific eligibility requirements for USDA loans allow a borrower to buy a house only in a rural area of the United States. It is important to note that even though USDA loans strictly require borrowers to get a property in a rural area, most of the US land is composed of rural areas, so a borrower can likely find an eligible property in every state and very close to large cities.

USDA Loan Requirements Chart

| Criteria | USDA Requirement |

|---|---|

| Status | US Citizen or Lawful Permanent Resident |

| Location | Area Population Less Than 20,000 |

| Type of Residence | Primary Residence |

| Household Income | No More Than 115% Of Area Median Income (AMI). |

| Debt-to-Income Ratio | Less than 41% Including Mortgage Payments |

USDA loans have a low interest rate compared to conventional loans because these loans are backed by the US Department of Agriculture, but USDA also requires borrowers to pay a mortgage insurance premium for all USDA loans to cover the risk of people defaulting on their loans. All government-backed loans, such as FHA loans, require some sort of mortgage insurance. In addition to that, some conventional loans require the borrowers to pay a private mortgage insurance premium if the loans are considered risky by the lenders. USDA loans require borrowers to pay a USDA Guarantee Fee that plays the role of mortgage insurance for USDA loans. Even though USDA borrowers have to pay mortgage insurance premiums, these premiums are among the lowest across all other types of mortgages.

Mortgage Insurance Rates

| Fee Type | Loan Type | |||

|---|---|---|---|---|

| Conventional Loan | FHA Loan | USDA Loan | VA Loan | |

| Upfront Fee | 0% | 1.75% | 1.00% | 0.50% - 3.60% |

| Annual Fee | 0.50% - 2.00% | 0.45% - 1.05% | 0.35% | 0% |

USDA Guarantee Fee

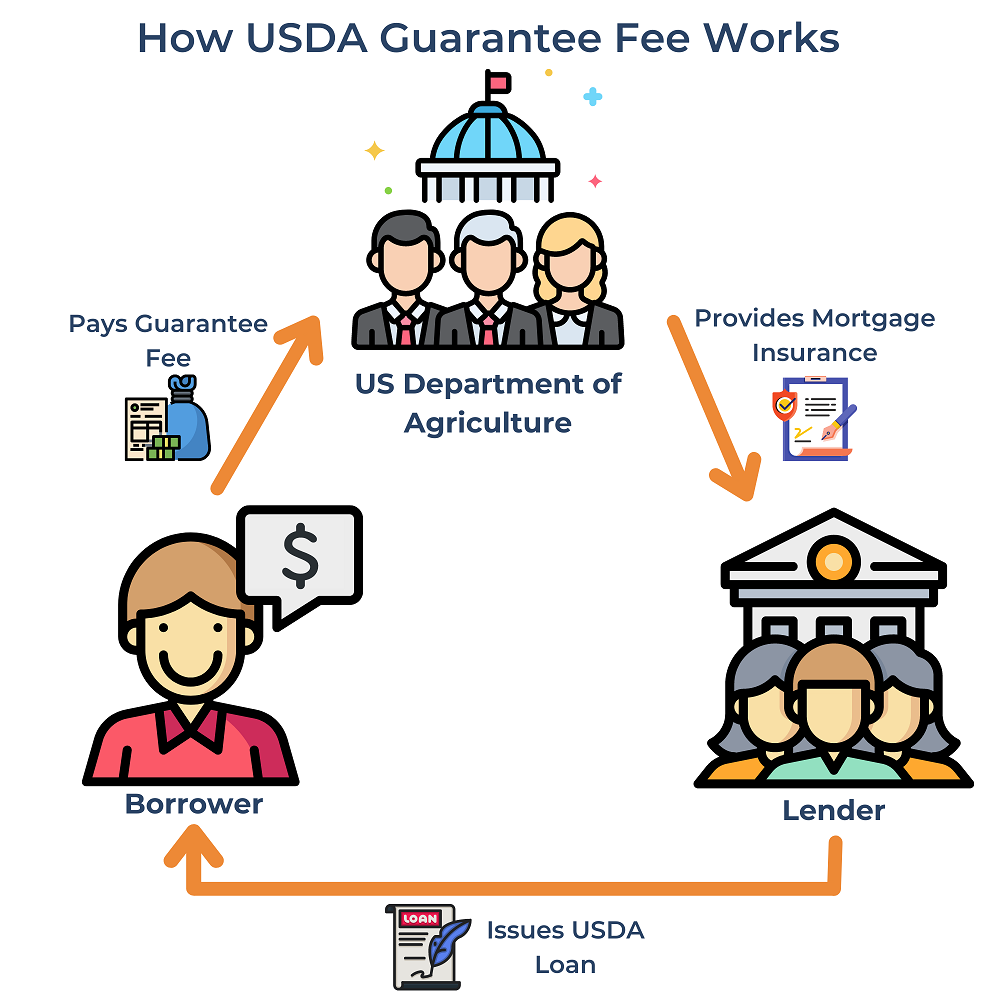

USDA Guarantee Fee is a special name for the mortgage insurance that is applied to USDA loans. Mortgage insurance is paid by a borrower, and it protects a lender in case the borrower defaults on their loan. Some people may call USDA Guarantee Fee a private mortgage insurance (USDA PMI), but the important distinction between the two is that PMI is required for conventional loans that have a loan-to-value (LTV) ratio above 80% and can be canceled once LTV drops below 80% while USDA Guarantee Fee does not depend on the LTV ratio, and it is paid throughout the USDA loan term. In addition to that, PMI is issued by private insurance companies while USDA Guarantee Fee is issued by the US government department.

How Does USDA Guarantee Fee Work?

The guarantee fee is required for all USDA loans regardless of the down payment and risk profile of the borrower. In addition to that, unlike mortgage insurance for other loan types, the guarantee fee is fixed for all loans and is not affected by different factors. The guarantee fee is paid by the borrower, and it protects the lender if the borrower defaults on their loan. The guarantee fee has two separate components that include an upfront fee and an annual fee. The upfront fee is 1% of the loan principal, and it must be paid upon loan origination. The annual fee charges 0.35% of the outstanding principal annually and is paid in monthly installments. Since the annual fee is charged based on the outstanding principal, the borrower pays less in annual fees every year because the outstanding principal decreases over time.

Example - USDA Loan Calculations

A borrower is planning to purchase a house with a 0% down payment using a USDA loan. The borrower made an offer to purchase the property for $300,000, and they are planning to pay for closing costs in full at the time of closing, so they expect to get the USDA loan for $300,000 with a 5% interest rate for 20 years. The borrower is interested to find out how much they would have to pay annually for the loan as well as the USDA Guarantee Fee. The USDA Guarantee Fee has an upfront fee of 1% of the original principal and an annual fee of 0.35% of the outstanding principal. The following table provides an estimated mortgage amortization schedule of the borrower’s loan:

USDA Guarantee Fee by Year Chart

USDA Loans Without a Guarantee Fee

There are two main types of USDA Loans: Direct and Guaranteed. The main difference between the two is that Direct USDA Loans are issued by the US Department of Agriculture while Guaranteed USDA Loans are issued by lenders. Lenders are required to pay a guarantee fee to the USDA, and the lenders can choose to pass the cost to the client. Most lenders require borrowers to pay the fee.

Direct USDA Loan: This loan is issued directly by the US Department of Agriculture, and they do not require a Guarantee Fee. Even though a borrower can save by choosing a Direct USDA Loan, only “Very-Low” to “Low” income households can be eligible.

Guaranteed USDA Loan: This loan is issued by private lenders and is insured by the US Department of Agriculture. Guaranteed USDA Loans require a Guarantee Fee. The fee must be paid by the lender, but most lenders choose to pass the cost to the borrowers.

Frequently Asked Questions

Do USDA Loans Have PMI?

USDA loans have mortgage insurance that is provided by the US Department of Agriculture, and it is called USDA. Even though it has mortgage insurance, it is not private mortgage insurance (PMI). Private mortgage insurance only applies to conventional loans and is issued by private insurance companies. USDA mortgage insurance is called USDA Guarantee Fee, and it is usually much cheaper than private mortgage insurance used for conventional loans.

How to Qualify for USDA Loan?

Not everyone can qualify for USDA loans. There are specific requirements that a borrower and the property purchased must meet to be eligible for the USDA loan. Typically, there are two ways to apply for a USDA loan, and the requirements may change depending on the way a borrower applies for the loan. The following list describes the two ways to apply for USDA loans.

- Guaranteed USDA Loan

This type of loan is issued by private lenders, and the loan is guaranteed by the US Department of Agriculture. This means that the lender understands that it is backed by the department as long as the borrower qualifies for the loan, which allows the lender to provide lower interest rates for the borrower. To be specific, the Rural Housing Service (RHS) guarantees to pay out the first 35 percent of the original loan in full and 85% of the other 65% of the loan in case the borrower defaults on their loan. Since USDA has to cover the lenders’ losses sometimes, it needs funding to do so. USDA funds this insurance solely with the fees they collect using USDA Guarantee Fee.

To qualify for a Guaranteed USDA Loan, the borrower must be US Citizen or Lawful Permanent Resident, choose a house in a rural area of the US that will be used as a primary residence, and have a household income of no more than 115% of AMI and have debt-to-income (DTI) ratio of no more than 41%. Usually, lenders also require a minimum credit score of 640, but the value may vary based on the lender.

- Direct USDA Loan

This type of loan is issued directly by the US Department of Agriculture, and it is intended for borrowers who cannot get approved for Guaranteed USDA Loan with private lenders. It is important to note that direct USDA loans do not require USDA Guarantee Fee because USDA does not insure direct loans.

To be eligible, the borrowers must still meet the USDA loan requirements, but they may have a very low income or a very bad credit score. In addition to that, the purchased property must be no more than 2000 square feet, must be priced within the applicable loan limits, and must not be used for income-producing activities.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.