What is Earnest Money?

CASAPLORER®Trusted & TransparentWhat You Should Know

- Earnest money is a deposit that the buyer makes to the seller of the house to prove that they are serious about the purchase.

- The exact amount of earnest money depends on the real estate market, but it typically ranges between 1% and 3% of the house sale price.

- When the purchase of the house is finalized, the earnest money deposit is returned to the buyer or is applied towards the mortgage’s down payment or closing costs.

- The buyer might lose their deposit if they change their mind about buying the house or if they don’t meet any of the responsibilities outlined in the contract.

- The deposit is refundable in the scenario that one of the contingencies in the contract is not satisfied with the most popular being financial, appraisal, and home inspection contingency.

What Is Earnest Money Deposit (EMD)?

Earnest money is a deposit that a buyer makes to a seller prior to closing to show that they are serious about the purchase. It is also known as a ‘good faith deposit’.

When you make an offer on a house and the seller accepts it, the seller has to remove the house listing from the market while the closing process takes place, which is usually several weeks. This means that during that time, the seller is not advertising the home and will be informing other potential buyers that the home is already sold. If the buyer of this home then changes his mind, decides not to buy the home, and doesn’t honor his agreement, the seller will have to put the listing back up and restart the process of finding a buyer. By that time, the seller will have already lost a lot of time and money.

Earnest money deposit assures the seller that the buyer is serious about the offer and will not walk away from the deal except in certain circumstances outlined in the agreement. The purpose of putting an earnest money deposit is to discourage buyers from placing multiple house offers.

How Does the Earnest Money Deposit Work?

The earnest money deposit is kept in an escrow account once the seller has accepted your offer. The funds act as a good faith purchase to assure the seller the buyer is going ahead with the transaction.

The purchase agreement will state how much earnest money is being deposited and where it will be held. When the transaction is complete and the sale is done, the funds can be returned or applied to the purchase price or closing costs.

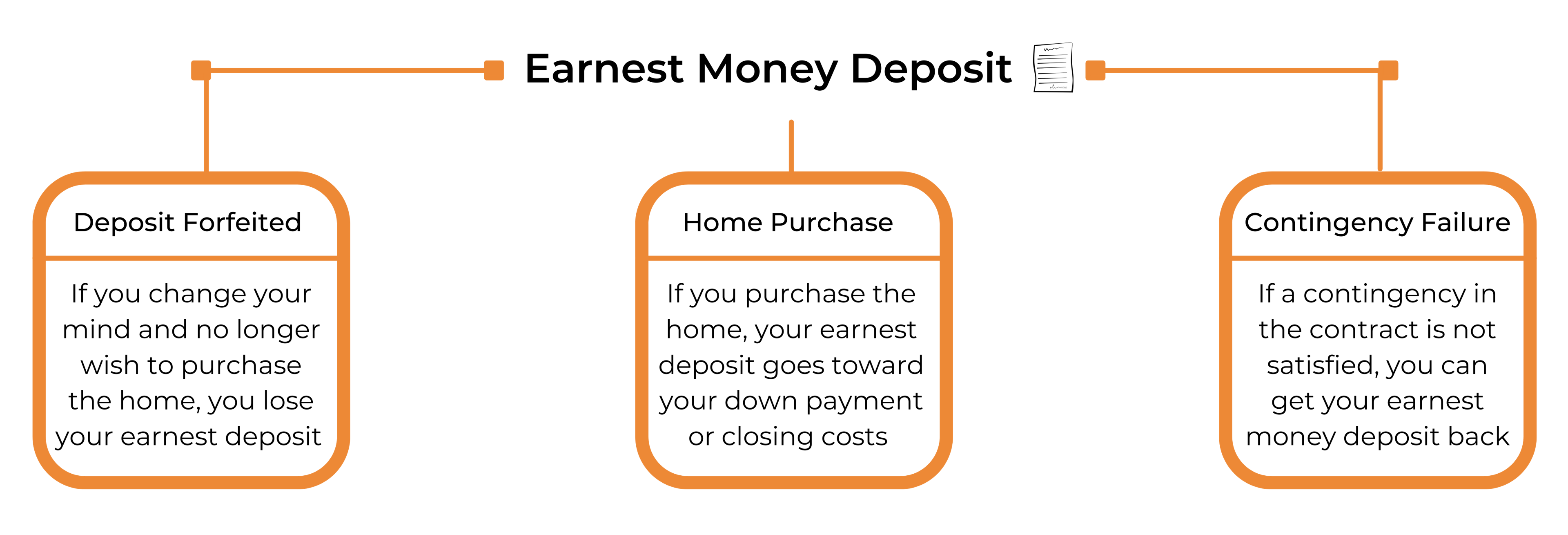

There are three scenarios as to the working of an earnest money deposit:

- Deposit Forfeited: In this scenario, the earnest deposit is not refunded. For example, let’s say you really like 3 houses and cannot choose between one. You decide to put in an earnest deposit for all 3 homes. As a result, the 3 sellers remove the homes from the markets for you. Finally, you pick one of the three houses. However, you lose your earnest money deposit for the other 2 homes in the process, because the other two sellers need to be compensated for their lost money and time.

- Home Purchase: In this scenario, the earnest money goes towards closing costs or the down payment. For example, imagine you really like one house and are certain that it will be your forever home. You decide to make an offer that includes an earnest deposit and the seller accepts it. After closing, your earnest money deposit goes toward your closing costs or down payment.

- Contingency Failure: In this scenario, the earnest deposit is refunded as a result of a breach in one of the contingencies. Continuing the last example, imagine that you really like a house and put an earnest money deposit with your offer to show that you are serious. The seller accepts your offer and takes the home off the market. However, during the home inspection, they find severe water damage and pipe failure. You have the option to cancel the transaction and get a full refund on your earnest money deposit or you can negotiate for a lower price.

Should You Pay Earnest Money?

It is important to understand that earnest money is not a requirement in the home buying process, it is more of a good-faith gesture. However, in competitive markets where sellers are getting multiple offers on their homes, it can be a key criterion to stand out. It assures the sellers that you will not drop out of the sale and cause hardship after the entire closing process is done.

If you are serious about the home, an earnest money deposit is a good decision as it is essentially prepaying some of the closing costs or down payment. If you are unsure about the home, or about the mortgage then you should consult a real estate agent whether it is the right decision to give a deposit or to make it a refundable deposit.

What Happens to Earnest Money at Closing?

A buyer does not lose the earnest money if the deal for buying a house is successful and no conditions of the contract have been breached. Depending on the contract and sometimes depending on the buyer’s preference, there are a few options of what may happen with the earnest money deposit.

- The Deposit Is Refunded to the Buyer - One of the most straightforward options of what happens with the earnest money deposit is the refund. The earnest money deposit is held in the escrow account before closing, and when a deal comes to a closing, the deposit is returned to the buyer unless otherwise agreed in the contract.

- The Deposit Is Applied to the Deal - If there is an agreement between the parties that the money will stay in the escrow account, then that money will be applied towards the payment for the house. It can be applied towards the down payment and closing costs. The earnest money deposit is usually 1% to 3% of the purchase price, which is not enough to cover both the down payment and closing costs, so it is unlikely that there will be a remaining balance. On the other hand, if there is a remaining balance after paying for all costs related to the deal, the buyer can withdraw that money.

Regardless of the situation and the conditions of the contract, if the buyer does not break any rules outlined in the contract, the money will be returned to the buyer in either cash or credits applied to the purchase of the house.

Is Earnest Money Deposit Refundable?

Yes, earnest money is refundable depending on which contingencies are included in the purchase agreement. The contingencies will include scenarios in which you can walk away from the deal with your earnest money deposit. The three most common contingencies:

- Financing Contingency: This contingency is there to protect buyers if they are rejected for a mortgage by their lender. If you were pre-approved for a mortgage, and then were rejected in the final approval process, this contingency allows you to get a full deposit refund. In extremely difficult markets, sellers will not like a financing contingency as it can prevent them from selling the house if you are not approved by your mortgage lender.

- Appraisal Contingency: Appraisal is the process of getting a home valued by an unbiased professional. Usually, the third-party appraiser is hired by the lender to assess the fair market value of the house. If the appraisal shows that the home is worth less than the sale price, you can choose not to proceed with the deal and get your earnest money deposit back. Or the alternative would be to negotiate a lower price with the lender.

- Inspection Contingency: A home inspection is essential in the home buying process. It can reveal problems with the house that you weren’t aware of. Depending on the results of your home inspection, you have the right to back out of the transaction if the home requires major repairs. In this case, you will get your earnest money deposit back. For example, if you were determined to buy a house before, but then the home inspection reveals there is a termite infestation, you are allowed to walk away from the deal. The alternative would be to negotiate with the seller a lower price or have them pay for the necessary repairs.

- Home Sale Contingency - This is a less used contingency where the buyer can back out of the purchase of a home because their existing home has not sold. This contingency is not used often as most sellers will not accept such a contingency as it reduces the chances of the sale proceeding. If you are considering this contingency look into bridge loan financing which can help overcome this.

There are some cases when the earnest money may not be refunded. EMD is not refunded if the buyer breaks any of the contingencies in the purchase agreement such as if they miss the deadlines to finance the transaction.

There are certain cases when the buyer can agree to a non-refundable earnest money deposit to stand out among buyers. In this case, if the deal does not go through for any reason, the deposit is not returned.

How to Protect Your EMD?

There are a number of things you can do to make sure that the money put towards your earnest deposit is handled appropriately and to lower the chances of losing your deposit.

- Know the terms and conditions of your contract

There are contingencies in the contract that protect the seller and if you break them, you risk losing your earnest money deposit. For example, the contract may state a deadline for completing a home inspection. If you fail to meet this deadline, you can lose your deposit. This is why it is important to read carefully and understand what your responsibilities are so you don’t miss anything.

- Check important contingencies

Before signing the agreement, make sure that all the necessary contingencies are included in the contract. Your financial, inspection, and appraisal contingencies are an important part of getting your earnest deposit back in the cases when you can either not get approved for a mortgage, the house is worth less than the price or it needs major repairs. Even if you still want to purchase the house when one of the issues mentioned above occurs, a contract that includes these contingencies can help you negotiate a lower price.

- Use a third party to handle the deposit

Never give your earnest money directly to the seller of the house. You should always use a reputable third party to handle the transaction such as an escrow company, title company, or legal firm. The money will remain there until closing. You can pay the earnest money through a certified check, a wire transfer, or a personal check. Don’t forget to get a copy of the check and a receipt.

- Include everything in the contract

To make sure that you don’t lose your earnest money deposit over a detail that was missed in the contract, you have to include everything before you sign. Important details include who gets to keep the earnest money in different scenarios. Even when you think something might be obvious, it still helps to put it in writing and avoid any confusion down the road. Make sure that any changes to the contract are documented as well.

FAQ About Earnest Money Deposit

How Much Earnest Money Should Be Offered?

Typically, earnest money deposits are 1% - 3% of the sale price. For example, on a $400,000 final home price, the earnest money deposit could be between $4,000 and $12,000.

However, you might have to put more or less depending on the real estate market your property is in. In a slow real estate market where there are a few buyers and a lot of sellers, a small earnest money deposit might work well. On the other hand, in a hot market where there are a lot of buyers and a few sellers, you will probably need to pay more to secure the house. The market with many buyers means that more people are willing to offer earnest money deposits, so sellers might go with the one that puts the highest deposit to be well compensated if the buyer walks out of the deal.

A real estate agent can advise you on exactly how much to put in your deposit depending on the market. Some sellers require a fixed amount, such as $5000, no matter the purchase price of the house. In this case, the buyer has to decide whether they would like to deposit the specified amount or walk away from the deal.

Should I Waive Earnest Money Contingencies?

Contingencies in an earnest money contract allow the buyer to walk away from the deal and get back their EMD if one of the contingencies is not met. This protects the buyer from losing money in case there is something wrong with the house. It is possible to waive the contingencies, which increases the risk for the buyer either getting locked in a bad deal or losing their EMD.

While there are higher chances of the seller accepting your offer if it contains fewer contingencies, it is important to understand that they protect you from losing your EMD in some cases. You can remove the financial contingency if you get approved for a mortgage before making the offer. However, the appraisal and inspection contingencies should be non-negotiable. Additionally, making a backup offer may result in the requirement for an EMD.

What Is the Difference Between an Earnest Deposit and a Down Payment?

An earnest deposit is a good faith payment to improve your chances of purchasing a home. The seller removed the listing preventing other buyers from purchasing the home. It is not required by the buyer.

The down payment, on the other hand, is an upfront amount that is paid to purchase the home. It is a requirement in most mortgage programs so be sure to check the minimum down payment requirements for different loan programs and lenders.

What Are Earnest Money Requirements for the Good Neighbor Next Door Program?

The Good Neighbor Next Door program allows qualifying individuals who work as teachers, law enforcement officers, firefighters, or emergency medical technicians, to receive a 50% discount on the price of a house if the individual commits to keep it as a primary residence for at least 36 months. This program provides a very financially attractive opportunity for qualifying individuals, but it has certain caveats to it. One of the caveats is that the participants must provide an earnest money deposit of 1% of the purchase price. More specifically, the EMD must be at least $500 and may not exceed $2,000.

Can Earnest Money Be Paid With a Personal Check?

Earnest money can be paid with a personal check, but you have to make sure to put the conditions of the EMD in writing before issuing the check. Generally, EMD can be paid with a wire transfer, personal check, or certified check.

When Is the Earnest Money Due?

Usually, the earnest money is due within 3 days after the earnest money offer is signed. The earnest money can be wired directly to the seller's agent or be passed in the form of a personal or a certified check.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.