Bridging Loans

What You Should Know

- A bridging loan is a short-term loan that provides liquidity to a buyer who needs to close on a new house before they are able to sell their old house.

- Bridging loans usually have a term length of 12 months, and they have a high interest rate, so it might be beneficial to pay them off as soon as the buyer has the money to do so.

- Even though it is better to avoid bridging loans, they can be very helpful during a seller’s market because buyers might have to close quickly to complete the deal.

- There are alternatives such as HELOCs and Home Equity Loans that may be cheaper options than bridging loans.

What Is a Bridge Loan?

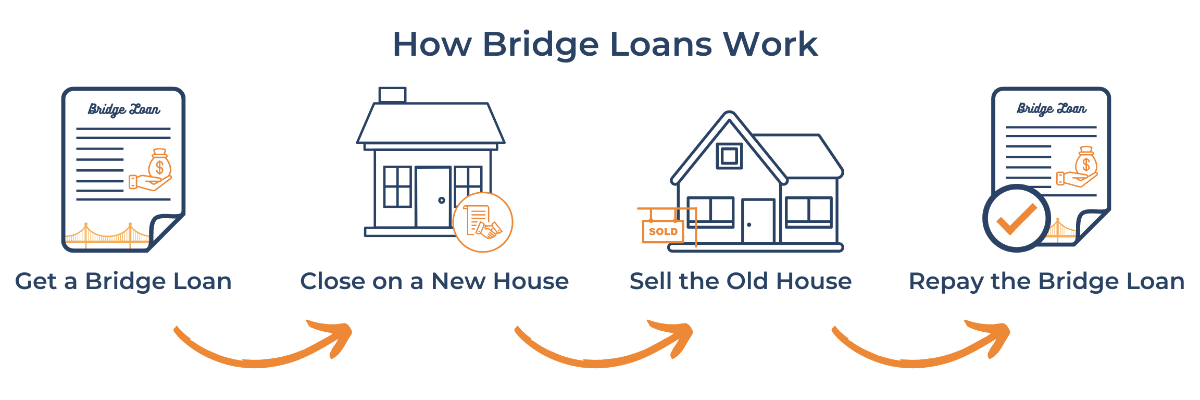

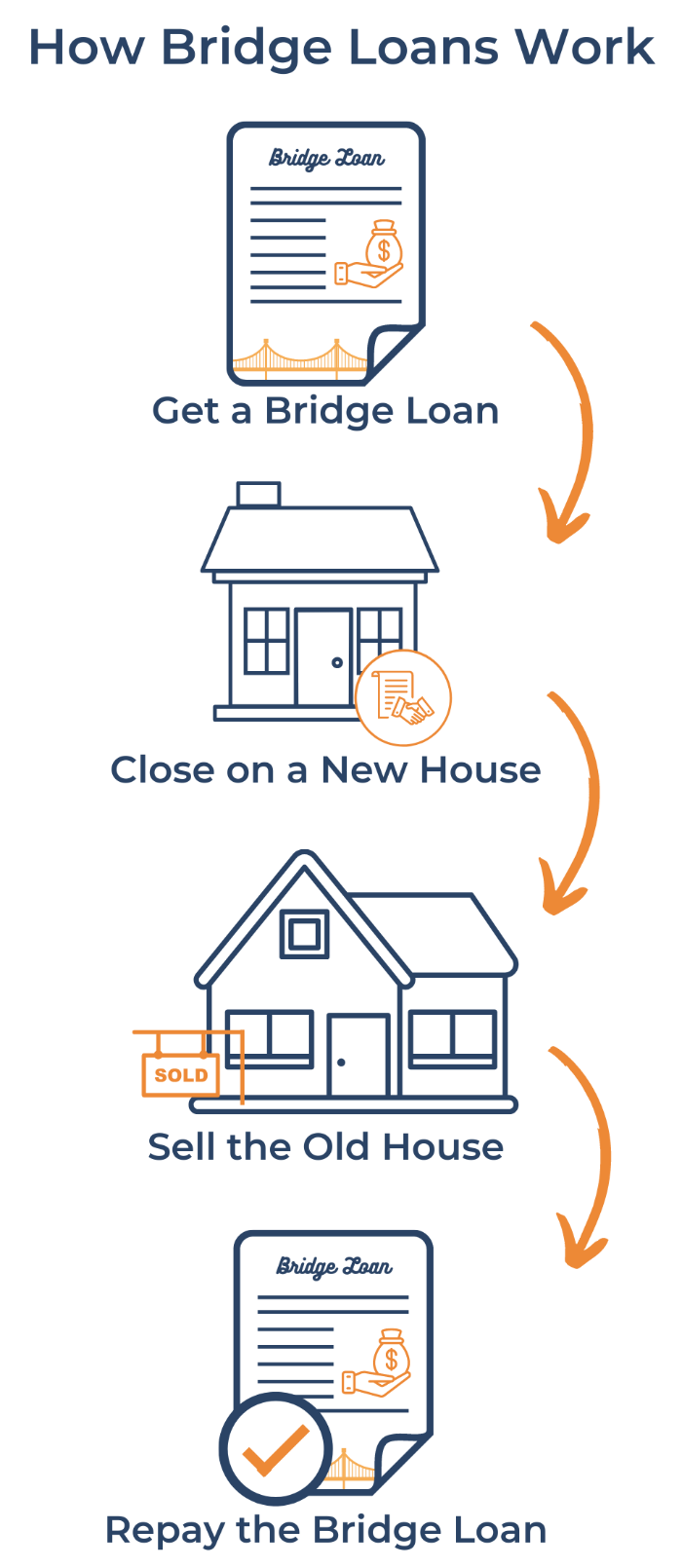

A bridge loan, which is also known as a bridging loan and a swing loan, is a short-term loan that usually lasts from 6 to 12 months. They provide liquidity when a homeowner has to close on a new property before selling their old property. Since a buyer has to pay a considerable amount of money at the time of closing, they may not be able to do so without selling their old property beforehand. A bridging loan allows the buyers to ‘bridge’ the gap between the two transactions of selling an existing home and using those funds to buy a new home.

In most cases, it is difficult for a homeowner to time the selling of their current home and purchase of a new home. Bridge loans help homeowners to ensure that they can buy their new home without the need to have funds immediately available from the sale of their current home. Bridging loans are short-term loans that are usually paid back within 12 months. They have relatively higher interest rates compared to mortgage loans while are still secured by the existing home as collateral. You can use this bridge loan calculator to estimate the cost of a bridge loan for your project.

How Do Bridge Loans Work?

Bridging loans allow the buyers to close on the property they want to buy before selling the property they currently own. The loan structure depends on the lender, the property owned by the borrower, and the borrower's financial situation. In addition to that, the payment structure, interest rates, and conditions of the loan may vary greatly from lender to lender. Some lenders may even require to pay off the previous mortgage on the property while others may provide the loan on top of the existing mortgage. It is important to shop around to get the best bridging loan available for the specific situation of the borrower.

| Criteria | Description |

|---|---|

| LTV Ratio < 80% | Bridge loan lenders require a borrower to have at least 20% in home equity before they may be eligible to get the loan. |

| Credit score > 620 | The lenders only issue bridge loans to people who have a history of being good with debt. A few lenders may issue a loan with a credit score as low as 600, but it is rare. |

| DTI Ratio > 50% | A lender is not legally required to make sure that the borrower can pay off the loan. On the other hand, most lenders will not issue a loan if Debt-to-Income (DTI) ratio is more than 50%. |

| Market Conditions | Another important factor that lenders look at is the real estate market where a property is being sold. If there is a risk that the property may not be sold, the lenders may decline the loan. |

Bridge loans are used for residential and commercial real estate transactions. They allow the borrowers to take advantage of the extra time bridging loans provide to sell their property at a better price and conditions. On the other hand, this benefit comes at a hefty cost of a high interest rate on the bridging loan. This may be a helpful financing tool for many investors and homeowners, but it may not be helpful in situations when the homeowner does not face timing problems with their property transactions.

| Loan Type | Interest Rate* |

|---|---|

| Conventional Mortgage | 5.50% |

| HELOC | Prime Rate + 1.50% |

| Home Equity Loan | Prime Rate + 0.75% |

| Bridge Loan | Prime Rate + 2.00% |

| Piggyback Second Loan | 10.00% |

| Personal Loan | 12.00% |

| Credit Card | 20.00% |

The interest rates offered on bridge loans are much higher than the interest rates for mortgage loans. Even though these loans are paid out in under 12 months, the interest payments may add up if the bridge loan has a large principal. Historically, the interest rate charged on bridge loans has varied on average from 6% to 10%, although the rates usually change with the prime rates.

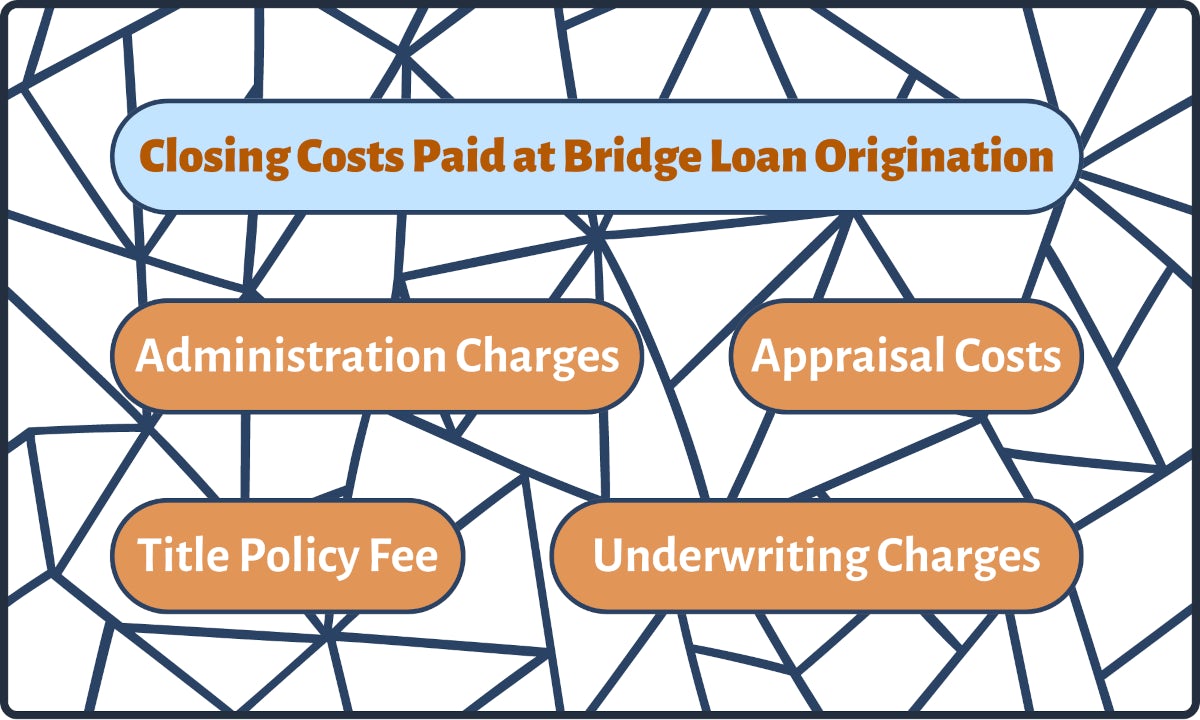

Bridging loans have an interest rate of around 2% above the prime rate, but the actual figure may deviate largely depending on the lender and the borrower. This means that when prime rates increase, the average interest rate for bridging loans increases too. In addition to that, there are closing costs that a borrower has to pay at the time of loan origination. They usually account for up to 2% of the loan amount.

Bridging loans may not be the best solution for every single person. For the most part, they are used by investors looking to swap properties that may cost millions of dollars. When it comes to residential real estate transactions, there are cheaper alternatives that may help homebuyers achieve their financial objectives:

1. Home Equity Line of Credit (HELOC): A HELOC allows homeowners to borrow funds by using the equity they own in their home as collateral. Most lenders allow up to 80% of the home value to be borrowed. HELOC functions like a credit card where funds can be borrowed and paid back, giving a lot of flexibility to the borrower. HELOCs charge a lower interest rate than bridge loans. However, they cannot be used if the home is up for sale. Therefore, if a HELOC is being used for the purpose of providing liquidity then it should be used to buy the new home first and then sell the existing home. HELOC payment calculator allows borrowers to check their monthly payments and compare them with bridge loan payments.

2. Home Equity Loan: A home equity loan is similar to a HELOC where a borrower can access funds based on the equity they own in their home. The difference between a home equity loan and a HELOC is that the funds are provided as a lump sum instead of a line of credit. Home equity loans are cheaper than bridge loans with lower interest rates and usually lower principal.

3. Piggyback Loan: Using a piggyback loan, which is also known as an 80-10-10 loan, the borrower first takes a mortgage on the new home for 80% of the home value, then they take a second short-term loan for 10% and pay the remaining 10% out of pocket. Once the borrower sells their existing home, the borrower can use those funds to pay off the second mortgage. This strategy allows borrowers to put little upfront and avoid private mortgage insurance (PMI), as the overall down payment is more than 20%.

Bridge Loan Lenders

Residential Bridge Loans

Residential bridge loans are used much less often as mortgage loans or even home equity loans. They are also considered riskier than the other loans used in real estate transactions. Because of that, large institutional lenders tend to avoid offering bridge loans to save costs and minimize their risks. Since large lenders do not offer these services, it might be difficult to find lenders who would be willing to provide this type of loan.

On the other hand, there are some small lenders, credit unions, and private lenders that would be happy to issue a bridge loan. The following list provides the names of lenders who issue bridge loans as well as the terms and conditions of their loans and the qualifications required.

- North Coast Financial

- Midland States Bank

- Banner Bank

Commercial Bridge Loans

Bridge loans are much more popular when it comes to commercial real estate and investment properties. Generally, it might not be a problem for households to save up money for a down payment on a house, but when down payments surpass hundreds of thousands of dollars, it might be difficult to raise that much cash at once even for an investment company.

This is why there is a larger demand for bridge loans in the investment sector. Since there is a greater demand, there is also a larger pool of financial solutions that might not only be beneficial for businesses but also interesting in their nature. Different lenders create unique financial solutions that may help specific businesses when needed.

- Avana Capital

- Stratton Equities

- Arbor

Bridge Loan Regulations

Even though bridge loans are mainly used for real estate transactions, they are not regulated the same way other mortgage loans are. There are usually two regulation levels that apply to bridge loans: federal and state. When it comes to federal-level regulations, bridge loans are often exempted from most of the sections that regulate other primary and higher-cost mortgage loans.

These exceptions provide a lot of freedom for the lenders to choose the interest rate, structure, and conditions of the loan. Some states also have state-level provisions regarding bridge loans that usually restrict the lenders from taking advantage of the clients who require bridge loans.

Federal Regulations

Most real estate transactions are regulated by the Real Estate Settlement Procedures Act (RESPA). RESPA outlines the basic rules for loans originated including how the disclosure of transactions, fees, and any business affiliations related to the translation is done. This act covers most of the mortgages that are being secured or bought by the government and quasi-government agencies like Fannie Mae and Freddie Mac. This means that most conventional and conforming loans are being regulated by RESPA.

Unlike conventional and conforming loans, bridge loans are not regulated by the RESPA. On the other hand, it is regulated by the Truth in Lending Act (TILA). This act provides an overview of the limitations and permissions of higher-priced loan types that are usually supplementary to a primary mortgage loan on a house. When it comes to bridging loans, this act regulates the following topics related to bridge loans:

- Section 1026.32(d) of TILA

- Section 1026.35(b) of TILA

- Section 1026.35(c) of TILA

- Sections 1026.43(a), (g), (h) of TILA

State-Specific Regulations

Some states have provisions that apply to bridge loans. Most of the time, these provisions target lenders rather than borrowers. This means that the borrowers are not required to comply with the state-specific regulations unless otherwise specified. If there are any provisions that a borrower must be aware of, they will be notified at the time of bridge loan inquiry. The states that have certain regulations applicable to bridge loans include the following:

This state has additional restrictions and requirements that are passed by the government on the state level. These restrictions are set to protect consumers from predatory lending practices as well as limit the risks taken by certain lenders. More specifically, there are 4 distinct terms and conditions for issuing a bridge loan applicable to New York:

1. The loan must be paid out upon the closing of the borrower’s sale of the property used to secure the bridge loan.

2. The borrower can repay the loan at any time without any prepayment penalty.

3. Regardless of the number of terms the loan is offered for, the fees and points may be taken only at the origination of the loan, and the borrower may not be charged more than 3 points at a time.

4. The loan must have a fixed interest rate within each term of the loan.

This state also has its own set of rules that describe prohibitions of certain lending practices, disclosure requirements of certain home loan information, prescribes certain duties and obligations to lenders in home loan transactions, and penalties for misconduct.

One specific provision that this act states is that mortgage loans with a term length of under 5 years must not have a payment schedule that does not fully amortize the outstanding principal balance except bridge loans. This means that in Michigan, a borrower may end up still owing money at the time the bridge loan expires, so they would have to make a balloon payment at the expiry date.

Texas has its own laws on home equity. The bridge loans taken out in Texas must comply with the Texas Home Equity Provisions (A6). The A6 provisions apply to any cash-out home equity loan on a primary residence in Texas.

Since it is regulated the same way as other ways to receive money using equity, such as HELOC or cash-out refinance, bridge loans are not an attractive option to use in Texas. The homeowners usually look for other options to secure a loan that has more beneficial terms, conditions, and qualification requirements.

In 2012, the senate of Florida issued updated statutes that cover numerous topics, including bridge loans. Balloon payments are prohibited for high-cost loans in Florida. On the other hand, the prohibition does not apply to loans that account for seasonal and justified irregular incomes. Even though bridge loans do apply to this type of definition, it also clearly states that bridge loans also do not apply to this prohibition.

Unlike the other states described above that have specific rules regulating bridge loans, California has rules that regulate other loan types. On the other hand, bridge loans are exempt from all regulations applied to other loan types in California.

This means that California restricts certain activities for most loans to protect the borrowers and limit the liabilities of the lenders. On the other hand, there are no additional regulations that apply to bridge loans making them riskier for borrowers.

Frequently Asked Questions

What Are Pros and Cons of Bridge Loans?

Bridge loans, just as any other loan, have their advantages and disadvantages. It is important to weigh them before choosing to proceed with getting a bridge loan. It is also important to make sure that a borrower can sustain the monthly payments that come with the loan in case the borrower is not able to sell their house as quickly as they expect.

| Advantages | Disadvantages |

|---|---|

| Lack of Sale-Contingent Offers | High Interest Rate |

| Fast Access to Cash | Appraisal Requirement |

| Interest-Only or Deferred Payments | LTV Requirements |

| Quick Processing Time | Collateral Required |

| Balloon Payment Required |

1. No Need for Sale-Contingent Offers: When a homebuyer purchases a home, there is a clause that allows them to back out of a purchase deal if their current home is not sold on time. In a seller’s market where several buyers compete for a single home, a sale contingent offer may decrease the chances of getting a property. Sellers may accept another offer that does not have this contingency to make sure that the deal will go through. In this case, bridge loans allow the buyer to place an offer without the sale contingency offer, making their offer much more attractive.

2. Fast Access to Cash: A borrower can get immediate access to cash, which can then be used for the minimum down payment instantly.

3. Interest-Only or Deferred Payments: The payments required for the bridge loan may be interest-only or deferred until the borrower sells their existing home. This can give the borrower flexibility as the payments can be made once the term of the bridge loan is over, which should be after the existing home is sold.

4. Quick Processing Time: In general, bridge loans require less time to be processed as the underwriting and funding process is faster than traditional loans.

1. High Interest Rate: As these are short-term loans that can involve risks for the lender, they charge a higher interest rate on the loan. Some lenders also give a variable rate that is usually above the Prime rate by around 2%, which is expensive relative to other loans available.

2. Appraisal Requirement: Apart from fees and other costs, a lender might also require an appraisal, which adds to the cost of getting a bridge loan.

3. A 20% Home Equity Required: A borrower is required to have at least 20% equity in their existing home or an LTV ratio of 80% to be eligible for bridging loan.

4. Home as Collateral: Since the home is the collateral, a default on the loan may result in foreclosure.

5. Debt Repayments: After a certain period of time, a borrower could be paying a mortgage on their existing home and making repayments on the bridge loan. Too many payments may result in financial stress and subsequent default.

When Should I Use a Bridge Loan?

There are certain cases where the use of a bridge loan can be extremely helpful.

1. Market Condition: If a buyer is looking for a house in a seller’s market and the seller does not accept sale contingent offers, the buyer might have to get a bridge loan to close the deal.

2. Down Payment: If a homebuyer cannot make the minimum down payment on a new home while making debt payments on their existing home, then a bridge loan could help make up the difference.

3. Timing: A borrower has found the new home they want to buy but has not been able to receive the funds from the sale of their existing home. Rather than losing the buying opportunity, the buyer can use a bridging loan to provide liquidity during the transitionary period.

4. Preference: A borrower would rather close on their new home before selling their existing home.

How Are Bridging Loans Structured?

Bridging loans can be structured in various ways. The two main methods offered to the borrowers are as follows:

1. Second Mortgage: Pays Down Payment on the New Home

This method works like a second mortgage. A homeowner borrows funds based on the equity they own in their existing home, which is then used to pay for the down payment on the new home. The borrower can increase their loan-to-value (LTV) ratio up to 85% which would be calculated based on the first mortgage and the bridging loan. This loan works similarly to a home equity loan, where the existing home is used as collateral. In this case, the borrower has to make sure that they can keep paying off their first mortgage, bridging loan, and potentially another mortgage if they close the deal on the property they want to buy.

For example, if a borrower’s existing home is valued at $400,000 and has an outstanding balance of $250,000, this means that a homeowner has $150,000 in home equity. If the homeowner borrows up to 85% of the home value, which is $340,000 ($400,000 * 85%), they will get a total bridge loan of $90,000 ($340,000 - $250,000). If closing costs and fees for the bridge loan are around $15,000, the borrower will have $75,000 available. This $75,000 can be used to cover the down payment for the new home, while the current home is in the process of being sold.

2. Lump-Sum Loan: Existing Mortgage Payoff and Down Payment on the New Home

In this case, a homeowner can borrow funds based on the value of their existing home to pay off the remaining mortgage and use additional funds for the down payment on the new home. The borrower can get up to 80% of the home value using this method.

For example, if a house is valued at $400,000 and the homeowner has an outstanding balance of $250,000, they can borrow a lump sum of $320,000 ($400,000 x 80%). Out of the $320,000 that they borrow, the outstanding balance to be paid is $250,000, leaving an additional $70,000 ($320,000 - $250,000) to be used for the down payment for the new home.

Both methods assume that the loan uses the existing home as collateral and that the home will sell fairly soon. Once the home is sold, the funds from the sale are used to pay off the bridge loan and accrued interest. In the event the home does not sell, the entire bridge loan will be due along with the new monthly mortgage payments.

This can result in severe financial strain and may eventually result in the borrower defaulting on one or both of the debt payments. Therefore, although bridge loans provide an elegant solution to lack of liquidity, they can also result in foreclosure that comes from mortgage default.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.