A Complete Guide to Owner Financing

What You Should Know

- Owner financing implies that the seller will provide the mortgage on the property to the buyer.

- Usually, the buyers who cannot qualify for a mortgage are looking for owner financing.

- Owner-financed loans have higher interest rates than conforming loans.

- Owner financing is usually done for a short term of five to ten years, which allows the buyer to build a credit score to qualify for a mortgage.

What Is Owner Financing?

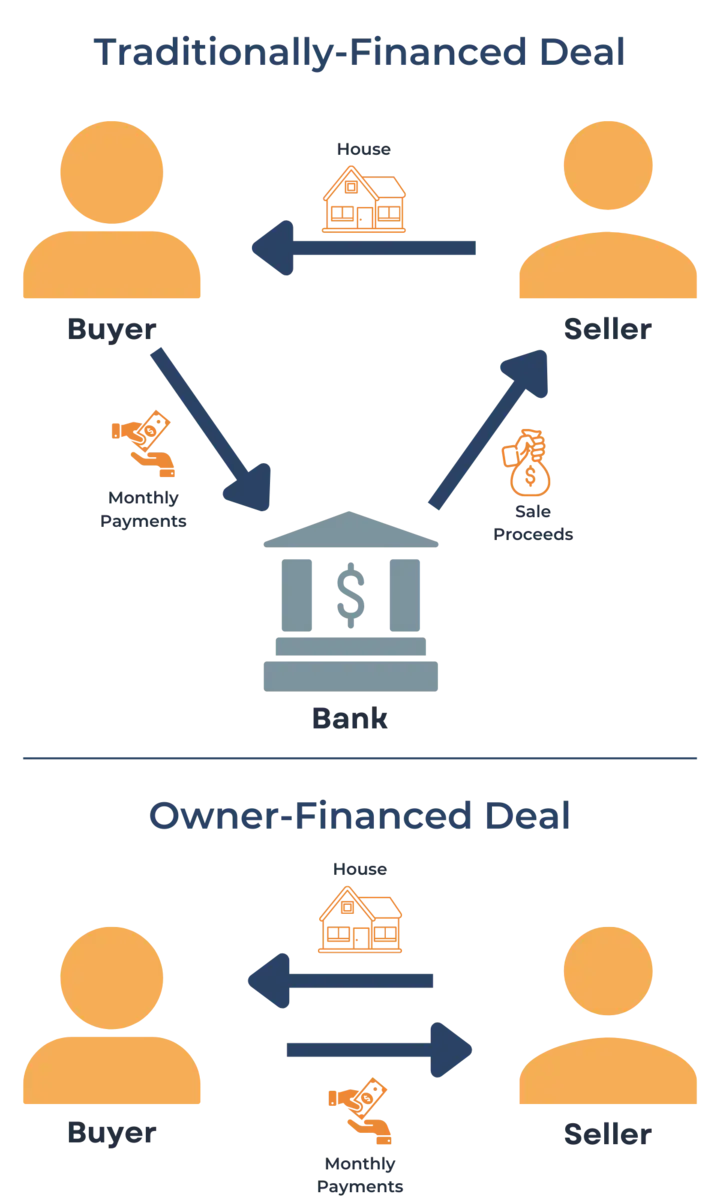

Owner financing, which is also referred to as seller financing, is a way for a buyer to finance a house by taking a loan from the seller instead of the bank. When a person decides to purchase a house, the most common way to pay for the house is to finance it with a mortgage that is extended by a third-party lender. In the case of owner financing, the buyer does not have to go to the bank because the owner is willing to extend the credit. There are different benefits that a buyer and a seller may receive using owner financing, but it is important to understand how it works to make sure that none of the parties take the risk they are not willing to take.

| Pros and Cons for Owner Financing for a Buyer and a Seller | |||

|---|---|---|---|

| Buyer | Seller | ||

| Pros | Cons | Pros | Cons |

| Few Requirements | Higher Interest Rate | Higher Demand for the Property | Risk of Default |

| Short Closing Period | High Balloon Payments | Potentially Higher Sale Price | Risk of Unexpected Repair Costs |

| No Minimum Downpayment | Seller Approval Is Needed | Can Sell As-Is | Due-on-Sale Clause Restriction May Apply |

| Low Closing Costs | High Return on the Mortgage | Dodd-Frank Act Restrictions Apply | |

| Ability to Negotiate Terms | Promissory Notes May Be Sold | ||

Depending on whether you are buying or selling a property, owner financing may provide you with an opportunity to make the transaction more flexible in its terms or provide an additional return down the road. It is also important to consider the downsides of this type of financing as it adds an extra degree of risk for a seller and a buyer. Every transaction is unique because every buyer and every seller has their specific financial situation. Depending on the situation, owner financing may provide a benefit to a buyer and a seller or create a possibility of bankruptcy for both buyer and seller. Since not all financial situations may benefit from owner financing, it is important to understand how owner financing works and what consequences to expect when choosing an owner financing in your specific situation. Owner financing implies that the seller cover the full amount of the sale price minus the down payment. There are other arrangements where the seller provides partial financing, which may be more fit for some people. For example, a seller carry back mortgage allows a seller to lend out some money to help the buyer cover the price of the house.

How Does Owner Financing Work?

An owner-financed home is a home for sale where the seller is willing to directly provide a mortgage to a buyer. This means that the buyer does not have to look for a mortgage when buying an owner-financed property because the seller will provide the mortgage to cover the cost of purchasing a house. Even though the seller plays the role of a lender in an owner-financed home sale, the whole transaction process differs from a traditional property sale.

When the seller plays the role of a lender, the seller does not give cash to the buyer to complete the transaction. Instead, the seller provides enough credit to the buyer to cover the purchase of the property minus the down payment. Since there is no money changing hands, besides the down payment, the seller and the buyer may be able to avoid paying hefty loan origination fees and other fees related to banking and financing expenses. Once the buyer and the seller agree on the terms of the loan, the buyer will have to sign a promissory note that outlines the terms and conditions of the loan including

- Principal Amount

- Interest Rate

- Loan Term Length

- Repayment Schedule

- Collateral Information

- Consequences of Default

The promissory note may contain the list of collaterals that are used to back the loan. Most of the time for promissory notes that are used in owner-financed real estate deals, the property sold is being used as collateral. Because of that, the buyer should make sure to cover payments due on time to avoid defaulting on their property. Often enough, a seller keeps the title to the property until the loan is paid off by the buyer. The seller also has to make sure that they can pay off the rest of their mortgage before getting into this deal. Most mortgages have the Due-on-Sale clause that requires the homeowners to pay off the rest of the mortgage once the house is sold. If the seller does not have enough funds to cover the outstanding mortgage, the house may risk becoming foreclosed, which may lead to large losses for the buyer and the seller.

Usually, owner-financed real estate deals are intended as short-term financing instruments. The promissory note usually states that the loan has a certain small monthly payment for 5 to 10 years followed by a balloon payment. The balloon payment in this promissory note reflects the belief of the buyer and the seller that the buyer would be able to qualify for the mortgage due to the equity built by the time the balloon payment must be made. Once the promissory note is close to its expiration day, the buyer should get approved for a mortgage and pay off the balloon payment. If the buyer cannot receive a mortgage at that time, the buyer may be at risk of losing the house as well as the equity they have built. After the housing crash in 2008, the US government passed the Dodd-Frank Act that prohibited mortgages with balloon payments in some owner-financed property sales, which made owner financing more difficult. Balloon payments are allowed for owner financing if the home seller doesn't complete more than 1 owner finance transaction in a 12-month period.

Types of Owner-Financed Deals

There are 4 main ways how a buyer and a seller can set up an owner-financed deal. All of them imply that the buyer has to make mortgage payments to the seller. The main difference between the 4 types of owner financing is who holds the title to the property while the mortgage is being paid off. The following list provides a description of four main owner financing options:

- Promissory Note

The most common type of an owner-financed home is a promissory note because it has the same function as a conventional loan. It clearly states the terms and conditions as well as collateral and outcomes of default. Some promissory notes can be sold to other investors since it has all necessary terms and conditions outlined. - Rent-to-Own Agreement

Even though rent-to-own agreements may not be an obvious option for owner financing, it is a good option for a seller to avoid taking high risks and a buyer to avoid paying large amounts of money for high interest. The idea of a rent-to-own model is that the buyer rents the house they want to buy for a specified period of time. This time is intended for the buyer to build their credit score and save money for the down payment. Once the time expires, the buyer will have the option to purchase the property. - Trust Deed

Trust deed works similarly to a promissory note, but this deed implies that the title on the property is held with a third party trustee until the mortgage is paid off in full. In this case, the buyer and the seller cannot access the title until the conditions of the note are either satisfied or broken. - Deed Retention

One last option available to the seller is to keep the title for the property on their name until the loan is paid in full. In this case, the seller is considered to be the owner until the conditions of the loan are satisfied and the title is transferred to the buyer.

Advantages and Disadvantages of Owner Financing

There are two parties that are involved in the transaction when the owner finances the deal, the buyer and the seller who is also the owner. Both parties have their own interests in the transaction, and both will have different pros and cons that they should consider before choosing to proceed with owner financing. This section will cover the most common advantages and disadvantages of owner financing for a buyer and a seller relative to traditional financing that involves a third-party lender.

Advantages for Buyers

- Few Requirements

Owner financing implies that the lender is a private lender who does not need to conform to certain standards or regulations when originating a loan to sell it later on. Since individuals may be less strict with their approval process, a buyer of an owner-financed house may have a better chance to be approved for the loan. The buyer may even be able to buy a house with bad credit simply because the seller is willing to provide financing. - Short Closing Period

Since there are fewer requirements to originate a loan, there are fewer documents to process, which may save a large amount of time. Owner financing is also known for having a short closing period since the owner will not go through the whole due diligence process that a bank would. - No Minimum Downpayment

Since there are no set requirements for a down payment for owner financing, the buyer may negotiate their down payment. Usually, lenders require a down payment of at least 20%. If the down payment is less than 20%, the lenders may require mortgage insurance , which may be costly. Owner financing provides an opportunity for the buyer to put a low down payment and avoid paying mortgage insurance premiums. - Low Origination Costs

Loan origination costs may be a significant expense when buying a house, and can be avoided by using owner financing. Mortgage origination cost in the USA is around 0.5% to 1% of the principal amount. This may not seem like a significant amount, but it may be considered a small bonus that comes when using owner financing. - Ability to Negotiate Terms

Third-party lenders usually follow the same origination process for most of their clients to make sure that their loans conform to certain standards. This means that buyers may have a hard time negotiating the terms of the loan with the lenders since there are more requirements that have to be met. On the other hand, home sellers may be more flexible and willing to negotiate the terms of the loan, so a buyer may have a better chance to negotiate more favorable terms with owner financing.

Disadvantages for Buyers

- Higher Interest Rate

Since it is a private loan, it is likely that it will have an interest rate that is much higher than conventional mortgage rates. Sellers also want to get a gain from providing owner financing, so they usually account their desired profits into the interest rate provided. It is possible to negotiate the interest rate, but the final interest rate will depend on the negotiation power a buyer has over a seller. - High Balloon Payments

Some owner-financed deals may contain a large balloon payment at the maturity of the promissory note. Balloon payments are used to keep monthly payments low and the loan's lifetime reasonably short. It is assumed that the buyer will be able to get approved for a mortgage before the balloon payment. If the buyer is not able to get approved for a loan, they may lose their property as well as all the equity they have built over the years. - Seller Approval Is Needed

Seller financing is not very common. One of the reasons it is not common is that the sellers usually need the funds from the house to purchase another property or cover the outstanding mortgage balance. If a buyer likes a house but cannot get a mortgage, they have to persuade the seller to provide owner financing, which may be impossible if the seller needs the proceeds from the deal to pay off debts.

Advantages for Sellers

- Higher Demand for a Property

Owner financing provides a unique opportunity for buyers who cannot get a mortgage, to finance a property directly with an owner. This will definitely increase the demand for the house, which will increase the number of offers a seller can get on a single property. - Potentially Higher Sale Price

A higher demand for the property may lead to offers that are over the asking price, especially if the buyers have the option to finance it with a lower down payment or lower monthly payment. Sellers should beware of picking the highest offer because not every buyer can reasonably estimate how much they can pay for the property. If they pay too much, they may default, which will lead to a lot of problems for the buyer and the seller. - Can Sell As-Is

Once the property is sold directly to the buyer, and there is no third party that may have a stake in the property, the seller may list a property As Is. When a property is listed As-Is, it implies that the property is sold without making any repairs, so it may require repairs or be inhabitable. Usually, a lender requires an appraisal and inspection to be done before a loan is originated. Since there is no third-party lender in an owner-financed deal, the house can be sold as-is without any additional repairs. - High Return on the Mortgage

Since the seller is issuing a mortgage privately to a person who needs that mortgage, the seller may require a high interest rate, which would be acceptable for the buyer. This allows the seller to benefit from a high interest rate, which is the return on the investment. In some cases, the sellers may prefer owner financing to cash because owner financing may have the highest risk-adjusted return among all other financial assets available. - Promissory Notes May Be Sold

Depending on the risk profile of a buyer and the quality of a promissory note, it could be valued and sold to another investor. In that case, the seller may get a lump sum payment even if the property was sold with seller financing. The ability to sell a promissory note to another investor provides a great deal of flexibility to the seller because they can choose the best timing to withdraw their cash and earn a high return on investment until that point.

Disadvantages for Sellers

- Risk of Default

One of the largest risks the seller faces is the default risk by the buyer. Since there is no financial intermediary who takes the financial risks, the seller assumes the risk. If a buyer does not have money to pay off their mortgage, they may default on the loan, which will directly affect the seller. On the other hand, the seller may take the collateral, which is usually the mentioned property, so the seller may get back the property in their possession. - Risk of Unexpected Repair Costs

If the buyer defaults on their debt and the seller takes back the property, they will be responsible to conduct all necessary repairs. The buyer may cause considerable damage to the property, which may lead to large losses in equity for the seller. - Due-on-Sale Clause Restriction May Apply

If the seller has an outstanding mortgage balance on the property at the time of the sale, the seller should ensure that they have enough money to cover the mortgage principal. Most of the time, mortgages have a restrictive covenant called the Due-on-Sale clause, which requires the outstanding debt to be paid off in full if the property is sold. If the seller has enough money to cover the outstanding debt, then the seller can sell the property and offer owner financing. - Dodd-Frank Act Restrictions Apply

Dodd-Frank Act was passed in response to the housing crash that happened in 2008. This act defines and regulates owner financing including some restrictions that make owner financing very unattractive to the sellers. The following rules apply to owner financing according to Dodd-Frank Act:- The seller did not build the property.

- The loan is fully amortizing (no balloon payments) with exceptions.

- The seller determines in good faith and documents that the buyer has a reasonable ability to repay the loan.

- The loan has a fixed or adjustable rate with a reasonable lifetime limit.

- The loan meets other criteria set by the Federal Reserve Board.

How to Find Owner-Financed Homes

The process of finding an owner-financed home is a little bit different than the process of finding a home with a pre-approved mortgage. The difference is mainly due to the fact that the seller has to agree to provide the mortgage, which may require some search and persuasion from the buyer. If you are looking to buy an owner-financed home, you will have to find a real estate agent who is knowledgeable about the topic and current market conditions. Once you find an experienced real estate agent, you can start looking for properties that may fit the buyer. It is important to note that most sellers will likely decline an owner-financed deal, so it is better to look for specific people who may be interested in such an arrangement. Some of the most popular places to look for owner-financed homes are as follows:

- Real Estate Agents

One of the most straightforward ways to find owner-financed deals is to find an experienced agent who works with owner-financed deals. They may know where to look for such deals or even have a network of clients who specifically look for this type of deal. A real estate agent is especially important if there are off-market owner-financed deals available that cannot be accessed by the public. - Real Estate Websites

Real estate aggregators may be a useful resource for research and shopping around. It allows you to easily see what is available around and compare different properties. Many websites also allow you to specifically search for owner-financed properties, which makes the process much easier. - FSBO Listings

Many For Sale by Owner (FSBO) listings come with flexible terms that may not come in regular listings. Owners who sell their property on their own tend to be savvy and knowledgeable of the market instruments available to them. They may be willing to extend a loan if it provides appropriate income. - Rental Listings

Some homeowners use their properties as rental properties. They do it because they can make rental income on rental properties. If you find a property that is listed for rent, you can contact the owners to discuss the possibility of leasing it or getting into a rent-to-own program that allows the buyer to rent their property before buying it. You can also directly ask them whether they would like to sell their property with owner financing. - Friends and Family

It is also worth it to let your friends and family know of your intentions. They may have a property that they are willing to sell on the mentioned conditions. They may also have friends or other acquaintances that may have a property that they are willing to sell. Given that it does not cost anything to talk to your friends and family, it may be a worthwhile attempt to find a property with owner financing.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.