Seller Closing Cost Calculator 2026

This Page Was Last Updated: October 15, 2024

| Modify entries below to get a more accurate result | ||

Real Estate Agent Commission | $ | |

Title, Escrow, Notary, & Transfer Tax | $ | |

Remaining Mortgage/Equity Loans | $ | |

Seller Concession | $ | |

Required Repairs | $ | |

| Modify entries below to get a more accurate result | ||

Real Estate Agent Commission | $ | |

Title, Escrow, Notary, & Transfer Tax | $ | |

Remaining Mortgage/Equity Loans | $ | |

Seller Concession | $ | |

Required Repairs | $ | |

What You Should Know

- Closing costs are fees required to be paid for to close the deal on a home. Both, buyers and sellers face closing costs.

- Seller closing costs usually range between 6% and 8% of the home selling price.

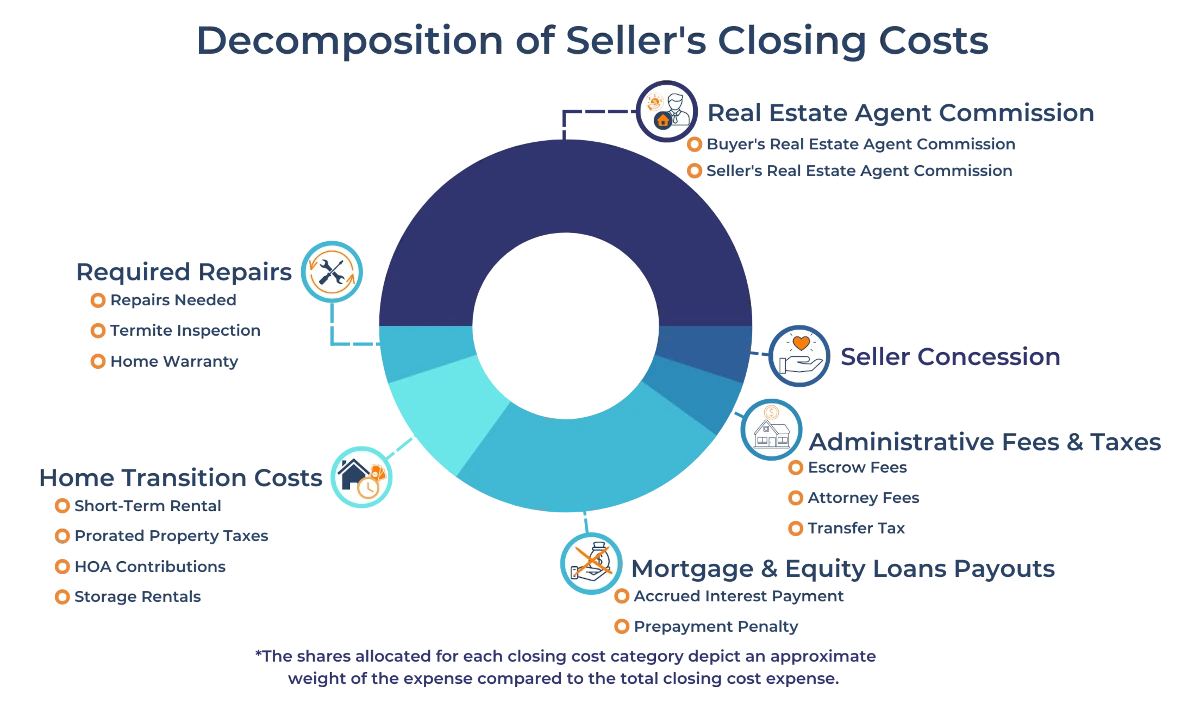

- Seller closing costs pay for the commission of real estate agents, title, escrow, attorney, transfer tax, the remaining mortgage, the seller concession, home transition costs, and required repairs.

- To minimize closing costs, a seller can look for cheaper service providers, check if they are eligible for a reduced rate on the owner’s insurance policy, and even ask the buyer to pay some of the closing costs.

Our seller closing cost calculator provides the total amount that you will receive from selling your home once all closing and miscellaneous costs have been deducted. Our calculator uses the estimated home selling price, and various costs such as the real estate agent commission, closing expenses, remaining mortgage balance, and seller discounts.

What Are Closing Costs?

Every home seller is familiar with the sellers closing costs because they have to be paid at the time of closing the deal on a home. Closing costs are the fees that a buyer and a property seller pay once the transaction closes. These fees are used to pay for legal and administrative expenses such as real estate agent commission, loan origination, etc. Usually, a seller pays closing costs, but some deals also lead to the buyer’s closing costs. A seller usually pays 6% to 8% of the sale price towards closing costs, but in some cases, the closing costs may reach up to 12% of the sale price excluding closing outstanding loans.

Seller Closing Costs by State

*The Median Seller’s Closing Costs are approximate and are based on the median home price in each state. Closing costs may deviate from the figures shown on the map above.

Different states have different closing costs because of differences in service prices, local taxes and regulations. This seller closing cost calculator helps you estimate your closing costs using your state and your county. For more precise results, you can adjust existing or add new expenses to the closing costs in the results section.

How to Calculate Seller Closing Costs

Suppose a homeowner is closing the deal on their property for $600,000. Three days prior to closing, the seller receives a closing disclosure where the seller can see all the details about the deal including expenses. The commission to the real estate agent is 4%, transfer tax fee of 1%, payment of remaining mortgage of $60,000, and payment towards repairs of $1,000. The following table provides a closing costs calculator.

The Closing Cost Details for a $600,000 Property

| Closing Cost Item | Price |

|---|---|

| Real Estate Agent Commission | $24,000 (4%) |

| Title, Escrow, Attorney, and Transfer Tax | $6,000 (1%) |

| Remaining Mortgage/Equity Loans | $60,000 |

| Seller Concession | $4,000 |

| Home Transition Costs | $0 |

| Required Repairs | $1,000 |

| Total Closing Costs | $95,000 |

| Net Proceeds Received: $505,000 ($600,000 - $95,000) | |

What Are Seller Closing Costs?

There are different sets of fees included in the seller’s closing costs. Closing costs for the seller can end up costing tens of thousands of dollars, but there are certain items that can be negotiated down in price. It may also be the case that some items are overpriced or are not required so the seller has the ability to negotiate those as well. It is important to understand what is included in the closing costs to know what exactly you are paying for each service. The following list provides the breakdown of closing costs into distinct categories.

- Real Estate Agent Commission

This is by far the largest expense required at closing. The standard real estate commission is 6% in most states, however, how much the agents charge you will depend on where you are located and the real estate market’s condition in that place. For example, in New York, the real estate agent’s commission is 6%. This means that you would have to pay $30,000 in commission if you sell a home for $500,000.

Seller/Buyer Agent Commission - The total commission explained above is typically split evenly between the seller agent and the buyer agent. However, this depends on the deal they have with the seller. If you already know the commission your agent will charge you, you can input it into the calculator to get a more accurate result.

- Title, Escrow, Notary, and Transfer Tax

These are known as closing costs and include the cost of paying for title insurance, escrow, notary fee, etc. Transfer taxes are imposed by the local government to transfer ownership to the buyer. On average, these expenses are usually 1% of the home sale price.

Title Insurance - The seller is required to pay for the owner's title insurance. This is a one-time fee that protects the future owner of the house from parties that may claim ownership of the house’s title. Another type of title insurance is the lender’s title insurance, which protects the lender and is paid by the borrower.

Escrow Fees - These fees are typically split evenly between the seller and buyer. Escrow fees are usually about 1% of the home’s sale price or a flat fee is charged for the whole service. Escrow providers help the parties in their closing process during the signing and recording of the documents and by holding the funds until closing.

Attorney Fees - Some states require a real estate attorney to be present during the closing process. Especially in complex transactions, an attorney can ensure that the seller is clear on the terms of the contract and ask for clarification when things seem vague. The real estate attorney is typically paid at closing from the sale’s proceeds.

- Attorney Required by Law- Attorney Is Not Required by LawTransfer tax - Transfer taxes are imposed by the local government to transfer ownership to the buyer. How much you pay in transfer taxes will largely depend on the state you live in. For example, for a median-valued home, the transfer taxes in San Jose, CA would come up to $1,085, while in Denver, CO, you would only pay $36 in transfer taxes.

- Remaining Mortgage / Equity Loans

- Seller Concession

In certain cases, the seller may offer discounts or seller credit to the buyer in order for the deal to go through. This could be in the form of reduced price or partial payment of buyer closing costs.

- Home Transition Costs

The seller may have to pay for some homeownership costs twice if they are in the process of switching houses and there is an overlap. Other times, they may have to pay for the costs involved in selling their house before moving into their new place.

Short-term rental - Sometimes, the seller sells their current house before the sale of their new house is closed. For that period, they might have to either rent a place temporarily or ask the buyer if they could lease the house back until the sale of their new house closes.

Prorated property taxes - Most states require property taxes to be paid twice a year. Depending on the day the house sale is closed, as a seller, you will have to pay property taxes on the house for the period of time the house was yours. For example, if property taxes were last paid on June 1st, and the house is sold on September 1st, you will have to pay for the 3 months of June, July, and August. If there is an overlap, and the seller owns two houses at the same time, they will also have to pay the property taxes for their new place.

HOA Fees - Similar to property taxes, you will have to pay for any accrued HOA fees for the time you were the owner of the house up to the sale’s close date. Moreover, HOA fees will have to be paid in the new place as well, when there is an overlap.

Furniture Storage - In the case when the seller sells their current house but the sale of their new house has not closed yet, they may not be able to move in. This means that they will have to pay for furniture storage until the sale closes and they can officially move in.

- Required Repairs

The seller may be required to pay for some home inspections and repairs that the inspections may reveal, depending on the agreement they have with the buyer.

Repairs Needed - If the home inspection uncovers problems with the house that will cost the buyer a substantial amount of money, the buyer may refuse to purchase the house if the owner does not pay for the repairs. In other cases, the seller may make these repairs prior to listing the house.

Termite Inspection - If a termite inspection is needed, typically the seller is required to pay for it.

Home Warranty - A seller may sometimes pay for a home warranty for the buyer to make the offer more attractive. The buyer can use a home warranty to get discounted repairs and replacement services.

If you have any outstanding mortgage balance, or if you took a home equity line of credit or loan, all these dues will have to be paid back prior to closing.

Accrued Interest - If you decide to pay off the balance in your mortgage early, you may owe some accrued interest to the lender. This interest is charged for the days between your monthly mortgage payment date and the day you pay off the mortgage completely. You would normally pay this interest in the upcoming mortgage payment, however, there won’t be any upcoming payments if you choose to pay off all your mortgage.

Prepayment Penalty - These are fees that a lender may charge you if you decide to pay off your mortgage early. When borrowers choose to prepay their mortgages, lenders lose the anticipated interest that they would get throughout the years. Therefore, prepayment penalties are in place to offset their loss of interest.

Frequently Asked Questions

What Closing Costs Do Sellers and Buyers Pay?

For every real estate transaction, both a buyer and a seller, have to split the closing costs. On average, a seller should expect to pay up to 12% of the home sale price in closing costs while a buyer should expect to pay 3% to 6% of the home sale price in closing costs. The difference in the closing costs between the buyer and the seller is due to the fact that they pay for different items that apply to their situation. Depending on the state, some items may need to be paid for by the buyer while others may be paid for by the seller.

Seller and Buyer Closing Cost Breakdown

| For Sellers | For Buyers |

|---|---|

| Agent Commission | Application Fee |

| Attorney's Fees | Appraisal Fee |

| Credits Toward Closing Costs | Bank Processing Fee |

| Escrow And Closing Fees | Credit Report Fee |

| HOA Fees | Homeowner’s Insurance |

| Prorated Property Taxes | Inspection Fee |

| Title Insurance | Loan Discount Points |

| Transfer Tax | Origination Fee |

| Prepaid Interest | |

| Prorated Property Taxes | |

| Title Insurance Policy For The Lender |

How to Reduce Seller Closing Costs?

Closing costs are not the same for everyone and can change based on your situation. There are certain ways that can be used to reduce the closing costs:

- Shopping Around For Several Service Providers: Most states allow title and escrow companies to set their own price points and payments, therefore, you can negotiate and try to get a much better price than the stated price. You can reach out to multiple companies and choose the best one based on price and service.

- Title Insurance Reissue Rate: If you have lived in the home for a few years and are selling, you can get a reduced rate for the owner’s title insurance policy.

- For Sale By Owner (FSBO): Instead of hiring a seller real estate agent and paying them 3% of the sale price, you can choose to sell the home yourself online or through personal means. This type of transaction where the seller sells the house on their own is called “For Sale by Owner.” It allows the seller to save on hiring a real estate agent, but it comes with a lot of work from properly pricing the property to filing all documents correctly and providing all information in a proper form.

How Much Are Seller Closing Costs?

Seller closing costs can range from 8% to 10% of the home selling price. On a $500,000 home, this can be between $40,000 and $50,000 in closing costs. Although this is a lot, there are several categories of expenses that can change based on location, negotiation, and specific situations. Using our calculator you can get an accurate value based on your circumstances. It is important to note that closing costs are only the only costs associated with selling a house. If your property has risen in value, you may have to pay capital gains tax.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.