Budget Calculator - Personal Budget Template

Your Monthly Budget Breakdown

Income & Expenses Analysis

What You Should Know

- This budget calculator allows you to estimate your monthly budget depending on your incomes and expenses as well as the area you live in.

- This budget calculator is based on income, and it may help you understand whether you have a deficit or surplus in your budget.

- There are various budgeting strategies that may help you to make sure that you allocate enough money towards your expenses and savings.

About This Budget Calculator

This budgeting calculator allows you to estimate your annual and monthly budget based on your income, current expenses, and planned savings. It can also estimate your income tax depending on your state. The results section provides a simple breakdown of your budget including your total incomes and expenses, and how much surplus or deficit you should expect. This monthly budget calculator allows you to input monthly as well as annual incomes and expenses.

This budget calculator follows a simple budget template that breaks down the spending into three categories: Essential Expenses, Non-Essential Expenses, and Savings. The essential expenses focus on the expenses that must happen, and they include housing expenses, grocery expenses, transportation expenses, and others. Non-Essential expenses include spending that is not necessary for day-to-day life. It focuses on entertainment expenses and other spending on luxuries.

It can also be used as a financial budget planner because it allows you to see how much you spend over how much you earn. If you earn more than you spend, the calculator will let you know how much funds you have that have not been allocated. It allows you to budget based on income and how much taxes you have to pay on your income.

Budgeting Strategies

There are various budgeting strategies available that may help you to comfortably reach your financial goals. Allocating your money with a strategy in mind may help you in different ways. It may help you stay on top of meeting your monthly car payments and having enough to spend on rent. It may also allow you to see how much you can contribute to your emergency fund and how much money you should have free to budget after.

Building a realistic budgeting strategy may be very beneficial. A person with a budget may be able to build significant savings and control their spending. A healthy budgeting strategy may also allow a person to increase their credit score and receive loans at a lower interest rate with a larger loan amount. Lower interest rates may help an individual to budget in large purchases by lowering their interest expense.

The following strategies may be useful to get an idea what budgeting strategy may work for you.

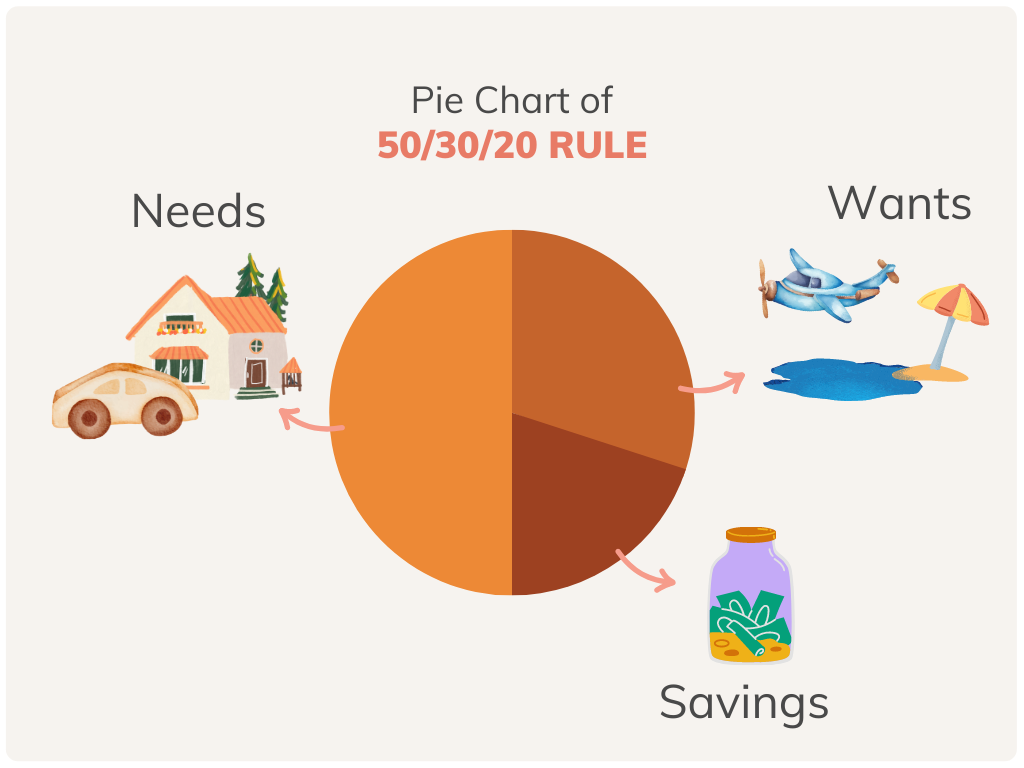

50/30/20 Rule

This rule is a simple budgeting strategy that classifies all expenses into three categories: necessities, wants and savings. A 50/30/20 rule states that a person should distribute their after-tax income as follows: 50% towards necessities, 30% towards wants and 20% towards savings. Even though this rule seems simple, it is important to understand what to consider a necessity and what should be considered a want.

Needs - 50%

Necessities include things like rent or mortgage payments, transportation costs, groceries, education and other. On the other hand, some high-end accommodation and transportation options may not be considered a luxury by many. For example, you may buy an affordable apartment that would fit your budget, or you could get an expensive mansion that may be over your budget. If your necessities are over 50%, you should consider downsizing your housing or transportation means.

Wants - 30%

The wants category focuses on the items a person buys that are not essential. This section may include items like entertainment expenses, going out, Uber rides and many others. It is always ideal to try to lower your budget for wants although you should stay realistic. Allocating some money towards entertainment may help you stay well rested over long periods of time.

Savings - 20%

It is important to consistently save money for many reasons. The savings can go towards an emergency fund, retirement, or a vacation. Having a cash buffer may help during hard times when a large amount of money is needed or when a person gets laid off work. Saving at least 20% of your after-tax income may help you avoid going into debt if a surprise expense arises.

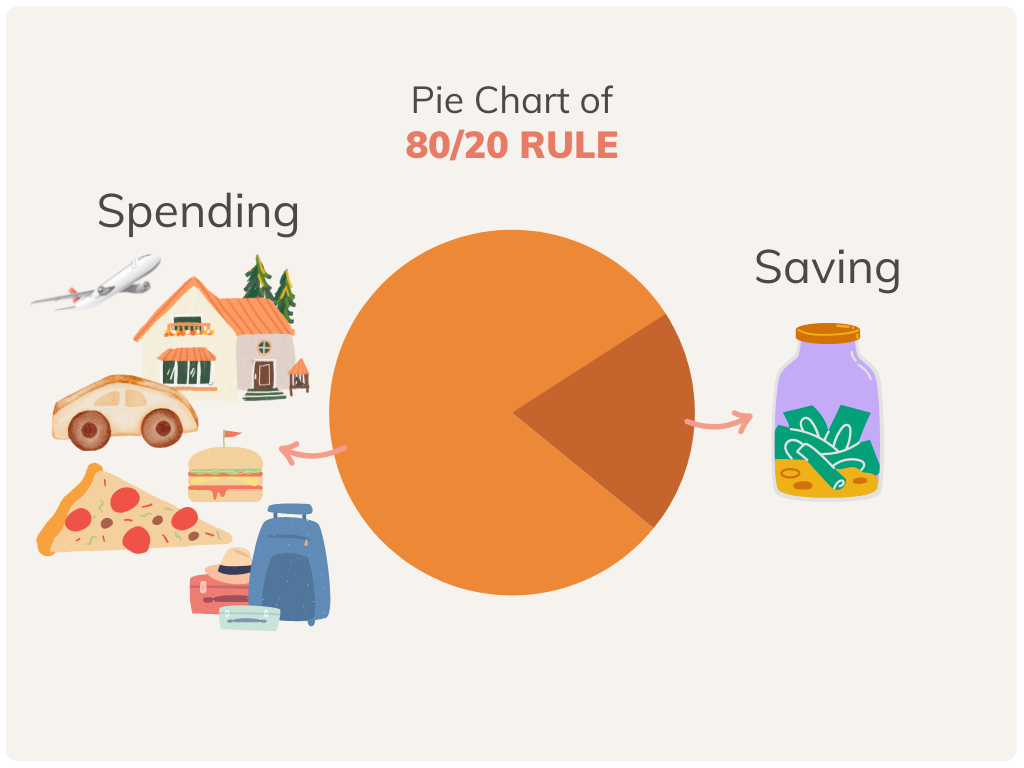

80/20 Budget Rule

This rule is a simplified version of the 50/30/20 rule. The 80/20 budgeting rule combines needs and wants together. It simply splits the after-tax income into two categories: expenditures and savings. The rule suggests that a person should spend 80% of their income and save the other 20%.

Saving is a crucial component of the mentioned rules. If a person does not have any savings, they may go into debt regardless of their net income. It is always important to have an emergency fund and retirement savings to protect your future.

Envelope Budget

This type of budgeting strategy allows you to visualize how much money you are spending on a certain category. Envelope budgeting is flexible in a way that a person can create their own spending categories. Once the spending categories are created, you can use envelopes to visualize them and allocate money towards each category. This way, you will have a visual understanding how much money you dedicate to each category.

This strategy may be useful to combine with another strategy that allocates your budget in different categories. It is easy to make budgeting mistakes allocating money towards different categories because envelope budgeting does not limit spending towards categories. A 80/20 budget rule may be a useful framework to work with envelope budgeting.

Living Cost in the United States

Living Wages By State Map

People living in the USA may require different budgeting strategies because the cost of living in the US varies a lot depending on the region. People living in California may have to allocate more money towards housing than people living in Ohio. Some people may have to contribute a larger share of their income towards their needs because of lower wages. This means that people should be flexible in choosing a budgeting strategy because no single strategy works for everyone.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.