FHA Streamline Refinance

What You Should Know

- FHA Streamline Refinance is a fast and cheap refinance process available to FHA loan holders.

- It allows the borrowers to avoid home appraisal, credit check, and income verification upon applying for the refinancing.

- The application process can be credit qualifying or non-credit qualifying where credit qualifying requires a borrower to update their credit history to receive a rate discount.

- FHA Streamline Refinance does not allow cash-out refinance, so it may not be the best product to withdraw cash against the equity in the house.

What Is a Streamline FHA Refinance?

The FHA Streamline Refinance is an FHA loan refinance program offered by the Federal Housing Administration. It allows FHA borrowers to refinance their mortgages faster and cheaper than other refinance options. The FHA Streamline Refinance often allows FHA borrowers to avoid a lot of paperwork such as a credit check and a home appraisal, which may save time and money for the borrower. FHA Streamline Refinance can benefit an FHA borrower with a cheap and quick refinance. On the other hand, some restrictions and requirements apply that the borrower should be aware of before proceeding with this refinancing option. A borrower who wants to benefit from a Streamline FHA Refinance should meet the basic requirements discussed below.

This refinance is offered by FHA-approved lenders, and the lenders may have additional requirements to get the loan without looking into the borrower’s creditworthiness. One of the most common requirements FHA Streamline Refinance lenders ask for is that the borrower should be current on their FHA loan for at least 12 consecutive months. If the FHA borrower has missed at least one payment during the 12 months, the lender would have to check their credit history and estimate whether the borrower is eligible for FHA Streamline Refinance. Some lenders may also offer no-closing-cost refinance, which means that the borrower does not have to pay for the closing costs upfront. Instead, the lender will charge a higher interest rate on the loan to cover the closing costs. Borrowers should be aware that a no-closing-cost mortgage does not spare them from closing costs, but simply makes them pay the closing costs with the mortgage principal.

FHA Streamline Refinance Pros and Cons

The FHA Streamline Refinance is a unique product available to borrowers with FHA-insured loans. It may be useful for the borrowers because it can be taken by a borrower only when there is a tangible benefit to the borrower, and it has lower closing costs than a regular FHA refinance. On the other hand, restrictions of FHA Streamline Refinance may make it incompatible with the objectives of some borrowers. The following table and list provide an overview of the most significant FHA Streamline Refinance pros and cons.

| Pros | Cons |

|---|---|

| Net Tangible Benefit | No Cash-Out Refinance |

| Quick and Cheap Refinancing Process | Some Closing Costs Are Charged |

| Possible Refinance of Underwater Mortgage | Mortgage Insurance Premium Is Required |

| May Not Require a Home Appraisal | |

| No-Closing Cost Refinance Available |

FHA Streamline Refinance Pros

Net Tangible Benefit

FHA Streamline Refinance can only be taken if it results in a net tangible benefit for the borrower. This means that the borrower will benefit from the refinance financially. If the borrower is approved for FHA Streamline Refinance, then there is a benefit for them. If the borrower is not approved for this refinance, then there is likely no benefit for the borrower to refinance at that moment.

Quick and Cheap Refinancing Process

One of the main differences between FHA Streamline Refinance and regular refinance is that an FHA Streamline Refinance is cheaper because the borrower does not have to pay certain refinance closing costs such as an appraisal fee and a credit history check fee. Since an FHA Streamline Refinance does not require an appraisal, the whole process is much faster than regular refinancing.

Possible Refinance of Underwater Mortgage

Most refinance programs look at the loan-to-value (LTV) ratio before approving a borrower for the refinance. FHA Streamline Refinance lenders do not look at the value of the house. Instead, the lenders look at the outstanding principal on the FHA loan. This means that if the value of the property has gone down, an FHA-insured loan borrower may be able to be approved for FHA Streamline Refinance.

May Not Require a Home Appraisal

Since FHA Streamline Refinance lenders are not concerned about the LTV ratio of a borrower’s loan, they do not require a home appraisal. The lack of requirement for home appraisal saves time and money for the borrower, which makes the FHA Streamline Refinance unique from other refinance programs available.

No-Closing Cost Refinance Available

Some lenders may offer a no-closing cost refinance when a borrower chooses to take on FHA Streamline Refinance. A no-closing cost refinance allows a borrower to avoid paying for closing costs at the time of closing. Instead, the closing costs are rolled into a mortgage principal and are amortized with the mortgage. The borrower should be aware that they will pay more over time with a no-closing costs mortgage compared to paying for closing costs upfront.

FHA Streamline Refinance Cons

No Cash-Out Refinance

It is only possible to get a $500 cash out of the FHA Streamline Refinance. Many homeowners use refinance as a way to get some cash against the equity that they have built. Even though FHA Streamline Refinance allows the borrower to withdraw up to $500, it is a very small amount to consider as a cash-out refinance. Since the FHA Streamline Refinance does not provide an adequate cash-out option, borrowers who are looking to get some cash should also consider a HELOC to get a loan against the equity they have built.

Some Closing Costs Are Charged

One of the largest benefits of an FHA Streamline Refinance is that it is considerably cheaper than other refinance options when it comes to closing costs. Even though it is cheaper, the borrower is still likely to pay a considerable amount of money toward closing costs. A borrower who is considering getting FHA Streamline Refinance should account for the closing costs before deciding to refinance.

Mortgage Insurance Premium Is Required

Paying an FHA Mortgage Insurance Premium is required for all FHA loans. The FHA Streamline Refinance also requires FHA MIP, which may lower the financial benefit of refinancing the loan in the first place. A borrower should always compare the upfront cost and the total benefit a refinance will bring before proceeding with it.

FHA Streamline Refinance Guidelines

The FHA Streamline Refinance process can either be credit qualifying or non-credit qualifying. A non-credit qualifying FHA Streamline loan does not require borrowers to submit a new application and does not require income, employment, and credit verification. FHA-approved lenders can use paperwork from the borrower’s existing mortgage to process the FHA Streamline Refinance request. This is a typical streamlining process, and it is available only when the borrower meets the following requirements:

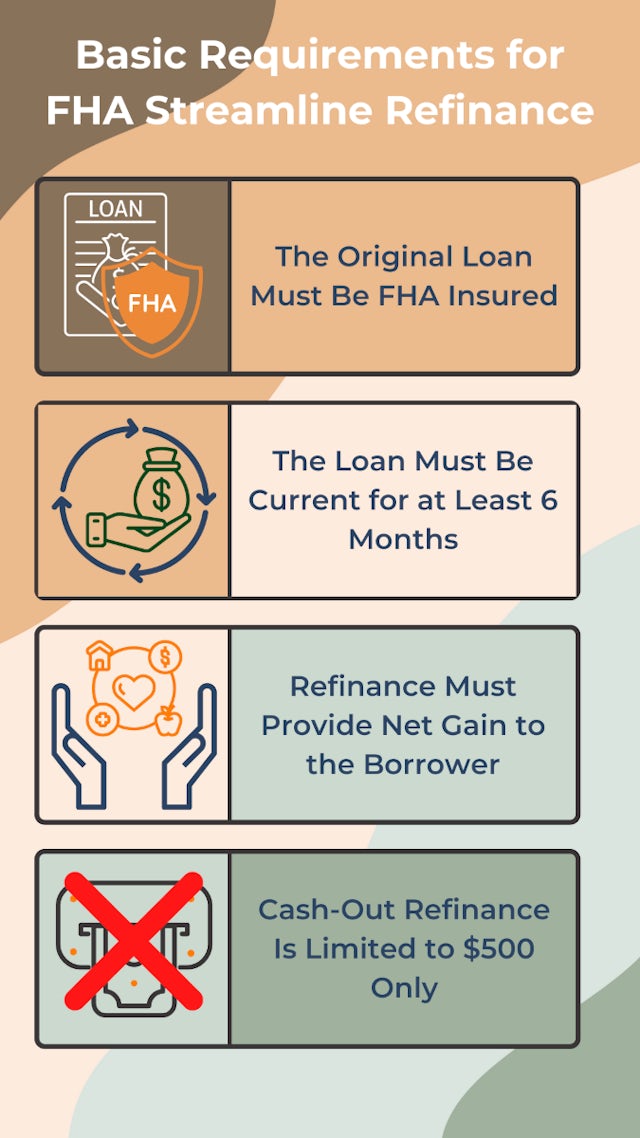

- The refinanced loan must be FHA insured.

- The FHA mortgage refinanced must be current (not delinquent).

- FHA Streamline Refinance must result in a net tangible benefit for a borrower.

- Cash-out refinancing is not allowed under FHA Streamline Refinance. A maximum of $500 can be taken out with FHA Streamline Refinance.

- The borrower’s monthly payments are lower as a result of FHA Streamline Refinance, or the decrease in mortgage term increases the mortgage payment by no more than 20%.

If a borrower is not eligible for a non-credit qualifying to streamline refinance, the borrower will have to complete a credit-qualifying FHA Streamline Refinance. This process requires the borrower’s credit report and income statements to re-assess their ability to make monthly mortgage payments. A borrower may also choose to proceed with a credit-qualifying FHA Streamline Refinance if their financial circumstances or credit history have improved. If a borrower has improved their creditworthiness, the borrower may be eligible for lower mortgage rates.

Frequently Asked Questions

Is the FHA Streamline Refinance a Good Idea?

An FHA Streamline Refinance may be a good idea if a borrower is eligible for it and the borrower is not looking to get a cash-out refinance. The FHA Streamline Refinance process has multiple benefits over the regular refinance process. In particular, FHA Streamline Refinancing allows a borrower to save time by avoiding a home appraisal and save their money by excluding some closing costs. On the other hand, an FHA Streamline Refinance may not be fit for everyone because it has certain eligibility requirements as well as restrictions on cash-out refinance.

Does FHA Streamline Refinance Have Closing Costs?

An FHA Streamline Refinance has closing costs that need to be paid. On the other hand, the closing costs for FHA Streamline Refinances are less than the closing costs for a regular refinance. Usually, refinance closing costs range between 2% and 5% of the refinanced mortgage principal. Performing an FHA Streamline Refinance does not require a home appraisal and a credit check since lenders can use the home appraisal from the original mortgage. This can save a borrower between $300 and $600 in refinancing closing costs.

Can Closing Costs Be Included in an FHA Streamline Refinance?

Some lenders offer a no-closing cost FHA Streamline Refinance. This offer allows closing costs to be rolled into the refinance principal. It is important to note that no-closing costs refinance allows the borrower to postpone the payment of closing costs, but the borrower will still have to pay for closing costs. No-closing costs refinance are often more expensive in total than a refinance where closing costs are paid upfront.

Do You Need an Appraisal for an FHA Streamline Refinance?

No, you do not need to conduct an appraisal for an FHA Streamline Refinance. This type of refinancing does not look at the loan-to-value ratio, which means that the lenders will not look at whether the value of the property has changed. Instead, the lenders will use the property appraisal from the original FHA loan. This allows borrowers to refinance the properties even if they have lost value significantly.

Does FHA Streamline Refinance Have PMI?

FHA Streamline Refinancing has an FHA mortgage insurance premium. FHA MIP is similar to PMI , but it applies only to FHA loans. In addition to that, FHA MIP has a fixed upfront fee and a fixed annual premium that must be paid by all FHA loan borrowers.

What Documents Do I Need for an FHA Streamline Refinance?

There are only a few documents needed for the FHA Streamline Refinance process because most of the documents will be used from the original loan application. The lender issuing FHA Streamline Refinance will require the following documents:

- A completed loan application.

- A mortgage statement with at least a six-month payment history.

- Employer information (to verify employment status).

- Bank statements if closing costs are paid upfront.

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.