Compound Interest Calculator

CASAPLORER®Trusted & Transparent| Year | Period Interest | Total Interest | Total Principal |

|---|---|---|---|

| Year 1 | $100.00 | $100.00 | $1,500.00 |

| Year 2 | $160.00 | $260.00 | $2,000.00 |

| Year 3 | $226.00 | $486.00 | $2,500.00 |

| Year 4 | $298.60 | $784.60 | $3,000.00 |

| Year 5 | $378.46 | $1,163.06 | $3,500.00 |

| Year 6 | $466.31 | $1,629.37 | $4,000.00 |

| Year 7 | $562.94 | $2,192.30 | $4,500.00 |

| Year 8 | $669.23 | $2,861.53 | $5,000.00 |

| Year 9 | $786.15 | $3,647.69 | $5,500.00 |

| Year 10 | $914.77 | $4,562.45 | $6,000.00 |

| Year 11 | $1,056.25 | $5,618.70 | $6,500.00 |

| Year 12 | $1,211.87 | $6,830.57 | $7,000.00 |

| Year 13 | $1,383.06 | $8,213.63 | $7,500.00 |

| Year 14 | $1,571.36 | $9,784.99 | $8,000.00 |

| Year 15 | $1,778.50 | $11,563.49 | $8,500.00 |

| Year 16 | $2,006.35 | $13,569.84 | $9,000.00 |

| Year 17 | $2,256.98 | $15,826.82 | $9,500.00 |

| Year 18 | $2,532.68 | $18,359.50 | $10,000.00 |

| Year 19 | $2,835.95 | $21,195.45 | $10,500.00 |

| Year 20 | $3,169.55 | $24,365.00 | $11,000.00 |

What You Should Know

- Compound interest earns interest on interest, which allows an investment to grow exponentially.

- Compounding period determines how often interest is compounded, and it also affects the total return on investment.

- Financial products that consumers use usually have a shorter than annual compounding period.

How to Calculate Compound Interest

Compound interest is an important financial concept that needs to be understood by every person who invests or takes on debt because it may help achieve investment goals as well as avoid taking on excessive and expensive debt. Before understanding how compound interest works, it is essential to understand the concept of simple interest.

Simple interest is interest that is calculated only on the original principal of an investment or a loan throughout the lifetime of the investment or the loan. Simple interest does not have increasing returns as the value of investment increases because the return on investment is paid based on the original value of the investment. For example, suppose your investment of $1000 increases in value by 10% of the initial principal for 10 years. Since it increases in value by 10% of the initial principal, the investment increases in value by $100 every year for 10 years. This means that the investment will be worth $2,000 in 10 years.

Simple Interest Formula

- FV - Future Value of the Investment.

- PV - Present Value of the Investment.

- r - Average Rate of Return.

- t - Number of Times Interest Is Accrued.

Compound interest is not only calculated on the original principal but also on the interest the investment accumulated over the life of the investment. As investment grows in value, the return on the investment also increases when it comes to compound interest. The fact that compound interest grows as the value of the investment grows, is the largest difference from simple interest, which does not grow as the value of the investment grows. For example, suppose your investment of $1000 increases in value by 10% each year for 10 years. Since it increases in value by 10% every year, the value of the investment increases at an increasing rate since the interest is being paid on the previous interest as well. In this case, the investment will be worth $2143. Generally, compound interest yields a higher return than simple interest.

| How Value of Investment Grows With Different Interest Types at 10% Interest Rate | ||

|---|---|---|

| Years | Simple Interest Investment | Compount Interest Investment |

| Initial Investment | $1,000.00 | $1,000.00 |

| Year 1 | $1,100.00 | $1,100.00 |

| Year 2 | $1,200.00 | $1,210.00 |

| Year 3 | $1,300.00 | $1,331.00 |

| Year 4 | $1,400.00 | $1,464.00 |

| Year 5 | $1,500.00 | $1,610.00 |

| Year 6 | $1,600.00 | $1,771.00 |

| Year 7 | $1,700.00 | $1,948.00 |

| Year 8 | $1,800.00 | $2,143.00 |

| Year 9 | $1,900.00 | $2,357.00 |

| Year 10 | $2,000.00 | $2,593.00 |

| Year 11 | $2,100.00 | $2,852.00 |

| Year 12 | $2,200.00 | $3,137.00 |

| Year 13 | $2,300.00 | $3,451.00 |

| Year 14 | $2,400.00 | $3,796.00 |

| Year 15 | $2,500.00 | $4,176.00 |

Compound interest formula also accounts for the number of times compounding happens in a given period. One of the most common examples of multiple compounding is monthly compounding. A 10% annual rate of return may yield more than 10% in a year if it is compounded monthly because the interest in that case is paid out every month. Since the interest is paid out every month, each consecutive month will pay out more because it will account for payments made in the previous months.

Compound Interest Formula

- FV - Future Value of the Investment.

- PV - Present Value of the Investment.

- r - Average Rate of Return.

- t - Number of Times Interest Is Accrued.

- n - Number of Times the Investment Compounds in a Year.

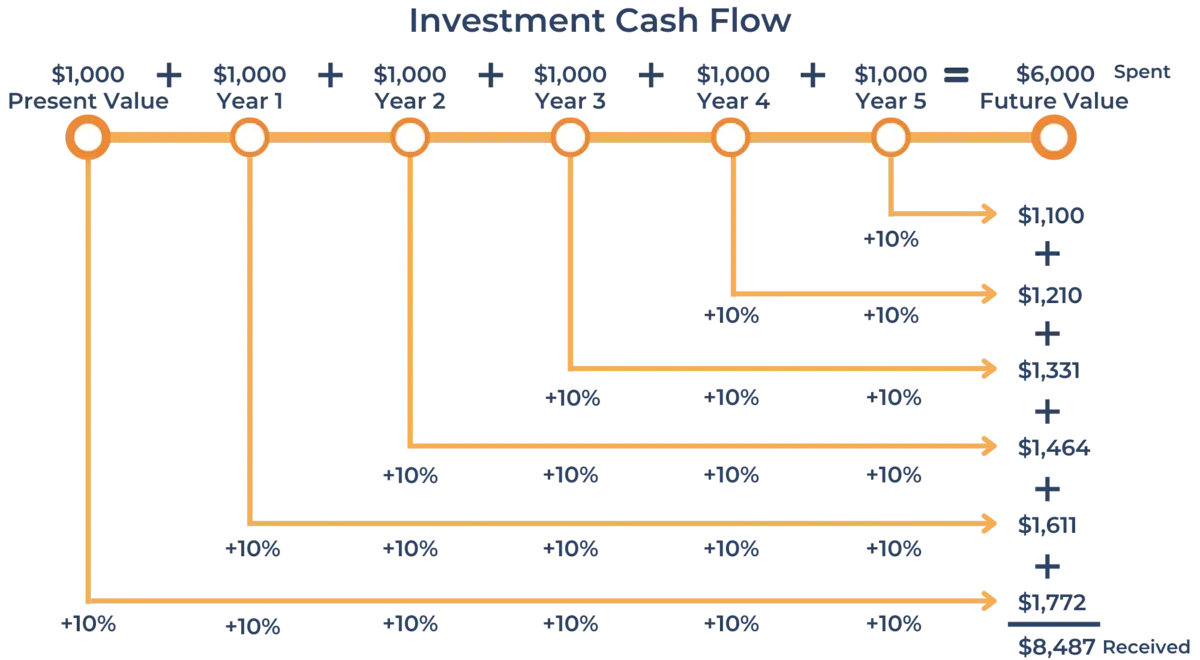

It is also important to consider how compound interest affects an investment when an investor periodically buys more of it. For example, an investor may be buying a diversified index fund that is increasing in value over time, and meanwhile, the investor periodically invests more into that fund. There is a formula to calculate the future value of the total investment for this case, but it is important to understand how this formula is derived to see how simple it is.

Every time an investor contributes additional funds to the index fund, it can be considered a separate investment. This means that it is possible to find the future value of each individual investment and sum it up to calculate the future value of the total investment. Suppose you have $1,000 invested and you want to keep investing $1,000 per year for five years, and your investment has a rate of return of 10% compounded annually. This means that the initial investment of $1,000 will be compounded 6 times, and the second investment will be compounded five times all the way until the last investment which will be compounded only once.

In other words, the formula to calculate the future value of periodic investments can be written using a summation formula. Using this general formula, an investor can estimate the future value of periodic investments even if the investments are irregular. On the other hand, it might be difficult to use it for indefinitely recurring investments because it implies summing up an indefinitely large amount of numbers.

Periodic Investment Compound Interest Formula

- FV - Future Value of the Investment.

- Pi - Payment Towards Investment at Time i.

- r - Average Rate of Return.

- n - Number of Times Investment Grows.

If the periodic payments are consistent and are the same over time, it is possible to derive a formula for finding the future value without recursively calculating the future value of every investment made. The following steps can be applied to the formula mentioned above to find a simplified formula for calculating the future value of consistent contributions.

The final formula for calculating the future value of a recurring investment is very similar to the formula for calculating the future value of an annuity. This is because both formulas have the same ideas and relate to the same process in a different context.

Annuity Formula*

- FV - Future Value of the Investment.

- P - Periodic Investment Contribution.

- r - Average Rate of Return.

- n - Number of Compounding Periods.

*This formula assumes the same number of compounding and contribution periods.

Other Compound Interest Formulas

There are other formulas used to calculate present value, rate of return, and even the number of periods of a given investment. All of them are derived from the formula that describes the relationship between an investment's present and future value. This section uses letters and a combination of letters to abbreviate certain metrics required for compound interest formulas. These metrics include the following and are used throughout this section:

- PV - Present Value

- FV - Future Value

- r - Interest Rate (Compounded Annually)

- n - Number of Years Compounding Occurs

- t - Number of Compounding Periods in a Year

| Compound Interest Formulas | |

|---|---|

| To Calculate | Formula |

| Present Value | |

| Future Value | |

| Rate of Return | |

There are two cases that have slightly different formulas, so they must be discussed separately. The first case is when n=1, which means that the compounding happens only once per period. Another important case is when n, which means that the compounding happens continuously throughout the lifetime of the investment. The following tables provide the formulas for both of the cases.

| Single Compounding Interest Formulas (n = 1) | |

|---|---|

| To Calculate | Formula |

| Present Value | |

| Future Value | |

| Rate of Return | |

| Continuous Compounding Interest Formulas (n → ∞) | |

|---|---|

| To Calculate | Formula |

| Present Value | |

| Future Value | |

| Rate of Return | |

What is a Compounding Period?

The compounding period determines how often the interest is compounded on your total investment. For example, the most common compounding period is annual compounding where a year needs to pass for the interest to compound again. This is included when calculating APY. Once the compounding period is over, interest is added to the capital. In the next compounding period, more interest will be earned on the larger capital. Our calculator has the ability to do daily, quarterly, semi-annual and annual compounding.

Depending on the compounding period, the return on it may be larger or smaller. For example, an annual return of 10% compounded annually yields less than the annual return of 10% compounded monthly because interest in the monthly compounding adds up every month while interest in annual compounding adds up once a year. The following graph shows how $1000 grows over 10 years at a 10% annual return with different compounding periods.

| Growth of $1000 at 10% Interest Rate over 10 Years With Different Compounding Periods | |||||

|---|---|---|---|---|---|

| Years | Compounding Periods | ||||

| Annum | Quarter | Month | Day | Continuous | |

| Initial Investment | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 |

| Year 1 | $1,100.00 | $1,104.00 | $1,105.00 | $1,105.00 | $1,105.00 |

| Year 2 | $1,210.00 | $1,218.00 | $1,220.00 | $1,221.00 | $1,221.00 |

| Year 3 | $1,331.00 | $1,345.00 | $1,348.00 | $1,350.00 | $1,350.00 |

| Year 4 | $1,464.00 | $1,485.00 | $1,489.00 | $1,492.00 | $1,492.00 |

| Year 5 | $1,611.00 | $1,639.00 | $1,645.00 | $1,649.00 | $1,649.00 |

| Year 6 | $1,772.00 | $1,809.00 | $1,818.00 | $1,822.00 | $1,822.00 |

| Year 7 | $1,949.00 | $1,996.00 | $2,008.00 | $2,014.00 | $2,014.00 |

| Year 8 | $2,144.00 | $2,204.00 | $2,218.00 | $2,225.00 | $2,226.00 |

| Year 9 | $2,358.00 | $2,433.00 | $2,450.00 | $2,459.00 | $2,460.00 |

| Year 10 | $2,594.00 | $2,685.00 | $2,707.00 | $2,718.00 | $2,718.00 |

The difference between compounding periods is not large, but it is clear that the shorter the compounding period, the larger the return. Different financial products such as credit card debt and mortgages may have different compounding periods. It is important to know the compounding period to precisely understand how much you will have to pay for a loan or how much your investment will return in the future.

Rule of 72

The rule of 72 is used to find an approximate amount of time it takes to double the investment amount at a certain rate of return. To calculate how much time it will take to double an investment, you need to divide 72 by the periodic rate of return to find the number of periods needed to double the value of the investment. For example, suppose you have invested $1,000 at a 10% rate of return compounded annually. Then the following calculations can estimate the number of years required for the investment to double in value.

This rule suggests that it takes 7.2 years for a $1,000 investment to double in value at 10% rate of return, which is approximately the right amount of time. It is important to remember about a few caveats before using this formula:

- Rate of Return should be expressed as a percentage rather than a decimal. For example, a 10% rate of return should be written as 10 rather than 0.1.

- Rate of Return used in the formula is periodic, which means that you can use the rate of return with a different compounding period. This will yield a result in the respective periodic length. For example, if the rate of return is annual, then the formula will yield the number of years needed for the investment to double. If the rate of return is monthly, then the formula will yield the number of months needed for the investment to double.

- The Rule of 72 is an approximation, which means that it may not always be accurate. It is the most accurate for the rate of return range between 5% and 12%. The higher the rate of return, the less accurate the prediction will be.

Rule 72 is a relatively simple instrument to estimate how long it will take for the investment to double in value. Even though it is simple, it is often used in investment and budget planning by families and households. Using the formula and estimating the timeframe of investment, it is possible to estimate the number of times the investment will go through a doubling cycle.

Riskier investments tend to have a higher rate of return, which means that they double in value within a shorter period of time than safer investments with a lower rate of return. Many investors with a longer investment time horizon prefer moderately risky investments because they will double multiple times over the investment lifetime, which will lead to large returns. People who have a short investment time horizon, usually purchase safer investments because they will not be able to enjoy the power of compounding interest regardless of the interest rate as well as not have as much time to recover their principal should there be losses.

Compounding Frequency of Financial Products

There are various financial products from mortgages to certificates of deposit that have some form of compounding. Depending on the type of the instrument, the compounding schedule may look different and compounding frequencies may range. Compounding frequency also depends on the financial institution providing the product because they usually have the power to choose what compounding frequency to use. The following table provides the most common compounding frequencies to some of the most popular financial products.

| Financial Product | Compounding Frequency |

|---|---|

| Consumer Loans | Monthly |

| Savings Accounts | Daily/Monthly |

| Certificates of Deposit | Daily/Monthly/Semi-annually |

| Money Market | Daily |

- Any analysis or commentary reflects the opinions of Casaplorer.com (a part of Wowa Leads Inc.) analysts and should not be considered financial advice. Please consult a licensed professional before making any decisions.

- The calculators and content on this page are for general information only. Casaplorer does not guarantee the accuracy and is not responsible for any consequences of using the calculator.

- Interest rates are sourced from financial institutions' websites.